Fixed Income/Bonds

Fixed Income/Bonds play a crucial role in financial markets, offering stability and diversification within investment portfolios. This topic explores the structure and characteristics of fixed-income securities, including government, corporate, and municipal bonds, as well as the interest rate mechanisms that influence their value. Key concepts include yield, duration, convexity, and the impact of economic factors on bond pricing. Mastery of these elements is essential for evaluating bond market trends and understanding fixed-income instruments, allowing technical analysts to make informed investment decisions and manage interest rate risk effectively.

Learning Objectives

In studying “Fixed Income/Bonds” for the CMT, you should learn to understand the fundamentals of fixed-income securities, including their structure, types, and valuation. Develop a strong grasp of bond pricing, yield calculations, and how interest rate fluctuations impact bond prices and yields. Analyze yield curve dynamics and interpret different shapes of yield curves to assess economic conditions. Study various types of bonds, such as government, corporate, and municipal bonds, and evaluate their risk profiles. Additionally, explore concepts such as duration, convexity, and credit risk as they relate to bond portfolios, focusing on how these measures inform investment strategies and risk management in the context of technical analysis.

Understanding Fixed-Income Securities

Fixed-income securities are investment instruments that provide regular, predictable income through interest payments. They are typically issued by governments, corporations, and other entities seeking to raise capital. These securities are an essential component of many investment portfolios, valued for their ability to provide steady income and relative stability compared to equities.

What Are Fixed-Income Securities?

Fixed-income securities, commonly known as bonds, are debt instruments issued by entities such as governments, corporations, or municipalities. When you purchase a fixed-income security, you’re essentially lending money to the issuer in exchange for periodic interest payments and the return of the principal at maturity.

Types of Fixed-Income Securities

There are various types of fixed-income securities, each with unique characteristics and purposes:

- Government Bonds: Issued by national governments, such as U.S. Treasury bonds. They are generally considered low-risk and include Treasury bills (short-term), notes (medium-term), and bonds (long-term).

- Corporate Bonds: Issued by companies to raise capital. These carry higher risks than government bonds but typically offer higher returns.

- Municipal Bonds: Issued by local governments and municipalities. They often come with tax advantages, making them attractive to certain investors.

- Mortgage-Backed Securities (MBS): Bonds backed by mortgage loans. Investors receive payments based on mortgage repayments, providing exposure to the housing market.

How Fixed-Income Securities Work

Fixed-income securities provide income to investors through regular interest payments, often referred to as “coupons.” The frequency of these payments depends on the bond structure—most commonly semi-annually, quarterly, or annually. At the end of the bond’s term, or maturity date, the issuer repays the principal amount to the bondholder.

Example: A $1,000 bond with a 5% annual coupon rate would pay $50 per year (or $25 semi-annually) to the investor until maturity.

Impact of Interest Rate Fluctuations on Bond Prices and Yields

Interest rate fluctuations have a significant impact on bond prices and yields. When interest rates change, bond values adjust accordingly, affecting both new bonds issued at current rates and existing bonds trading in the secondary market. Here’s how these fluctuations work and their effects on bond investors.

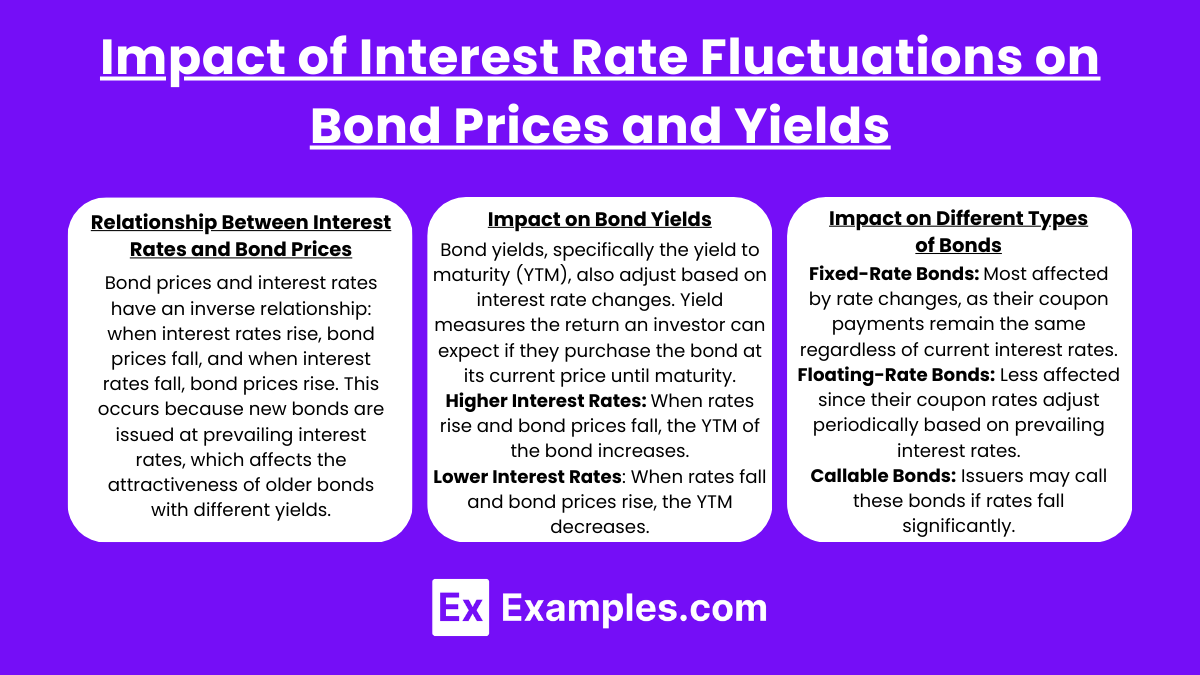

1. Relationship Between Interest Rates and Bond Prices

Bond prices and interest rates have an inverse relationship: when interest rates rise, bond prices fall, and when interest rates fall, bond prices rise. This occurs because new bonds are issued at prevailing interest rates, which affects the attractiveness of older bonds with different yields.

- Interest Rate Increase: When rates rise, new bonds offer higher yields, making existing bonds with lower rates less attractive. Consequently, the price of existing bonds falls to align their yields with the new, higher interest rates.

- Interest Rate Decrease: When rates fall, new bonds offer lower yields. Existing bonds with higher rates become more valuable, increasing their prices.

Example: If interest rates rise from 3% to 5%, a bond paying a 3% coupon will be less attractive, causing its market price to drop so that its effective yield aligns closer to the new market rate.

2. Impact on Bond Yields

Bond yields, specifically the yield to maturity (YTM), also adjust based on interest rate changes. Yield measures the return an investor can expect if they purchase the bond at its current price and hold it until maturity.

- Higher Interest Rates: When rates rise and bond prices fall, the YTM of the bond increases because investors can buy the bond at a lower price and still receive the fixed coupon payments, enhancing the return.

- Lower Interest Rates: When rates fall and bond prices rise, the YTM decreases as investors pay a premium for the bond’s fixed interest payments, resulting in a lower effective yield.

Example: A bond with a face value of $1,000 and a 5% coupon bought at a discount due to rising interest rates (e.g., purchased for $950) will have a higher YTM than if it were bought at its original face value.

3. Impact on Different Types of Bonds

The impact of interest rate changes can vary depending on bond type:

- Fixed-Rate Bonds: Most affected by rate changes, as their coupon payments remain the same regardless of current interest rates.

- Floating-Rate Bonds: Less affected since their coupon rates adjust periodically based on prevailing interest rates.

- Callable Bonds: Issuers may call these bonds if rates fall significantly, allowing them to refinance debt at lower rates, which limits the bondholder’s potential for gains.

Example: If interest rates drop significantly, an issuer of a callable bond might choose to redeem it early, affecting the bondholder’s expected income stream.

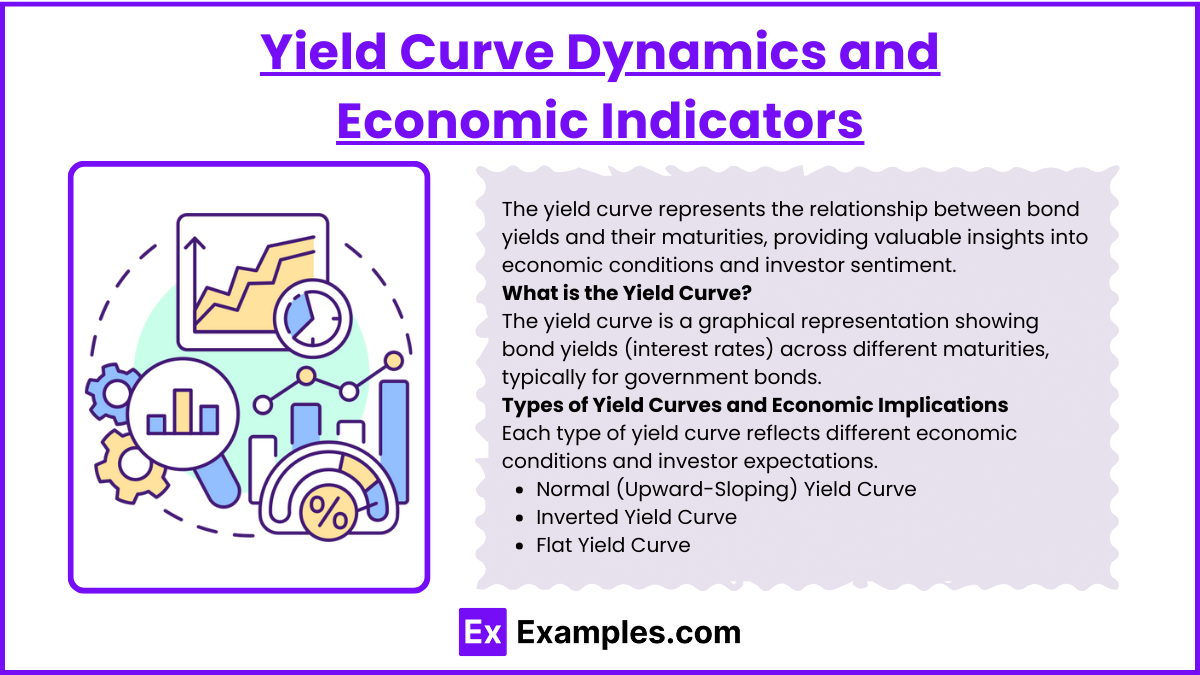

Yield Curve Dynamics and Economic Indicators

The yield curve represents the relationship between bond yields and their maturities, providing valuable insights into economic conditions and investor sentiment. Changes in the yield curve shape and slope are closely watched as indicators of economic growth, inflation expectations, and potential recessions. Here’s an overview of yield curve dynamics and how they relate to key economic indicators.

What is the Yield Curve?

The yield curve is a graphical representation showing bond yields (interest rates) across different maturities, typically for government bonds. It reflects the cost of borrowing over various time frames, from short-term to long-term, and is a critical tool for assessing market expectations.

- Normal Yield Curve: Typically upward-sloping, indicating that long-term yields are higher than short-term yields, reflecting expectations of stable economic growth and inflation over time.

- Inverted Yield Curve: Occurs when short-term yields are higher than long-term yields, often seen as a signal of economic downturn or recession.

- Flat Yield Curve: A flat or nearly flat curve occurs when yields across maturities are similar, indicating uncertainty about future economic conditions.

Example: A steep yield curve suggests confidence in economic growth, as investors expect higher inflation and interest rates in the future.

Types of Yield Curves and Economic Implications

Each type of yield curve reflects different economic conditions and investor expectations.

- Normal (Upward-Sloping) Yield Curve: This shape is typical in a healthy, expanding economy where investors demand higher yields for longer maturities to compensate for inflation and other risks.

- Implication: Generally signals positive economic growth, moderate inflation expectations, and a stable interest rate environment.

- Inverted Yield Curve: An inverted yield curve is rare and often seen as a precursor to an economic recession, as investors seek safety in long-term bonds, driving yields lower than short-term rates.

- Implication: Historically associated with upcoming economic slowdowns or recessions, as it indicates lower expectations for future interest rates.

- Flat Yield Curve: A flat yield curve suggests that investors are uncertain about future economic conditions and expect little difference in short- and long-term rates.

- Implication: Often signals economic transition, with potential stagnation or moderate growth expectations. It may indicate that the economy is nearing a turning point.

Example: An inverted yield curve occurred in the U.S. before the 2008 financial crisis, accurately predicting the economic downturn.

Yield Curve and Key Economic Indicators

The yield curve’s shape is influenced by several economic factors, such as:

- Inflation Expectations: If investors expect inflation to rise, long-term yields tend to increase, steepening the yield curve. Conversely, lower inflation expectations can flatten or invert the curve.

- Economic Growth: Strong economic growth expectations typically steepen the yield curve, as higher demand for credit leads to rising long-term rates.

- Interest Rate Policies: Central banks, such as the Federal Reserve, influence short-term rates through monetary policy. Rate hikes often lead to a flattening yield curve, while rate cuts can steepen it.

Example: The Federal Reserve’s decision to lower interest rates in response to economic weakness can lead to a steeper yield curve if investors anticipate stronger growth and inflation in the long term.

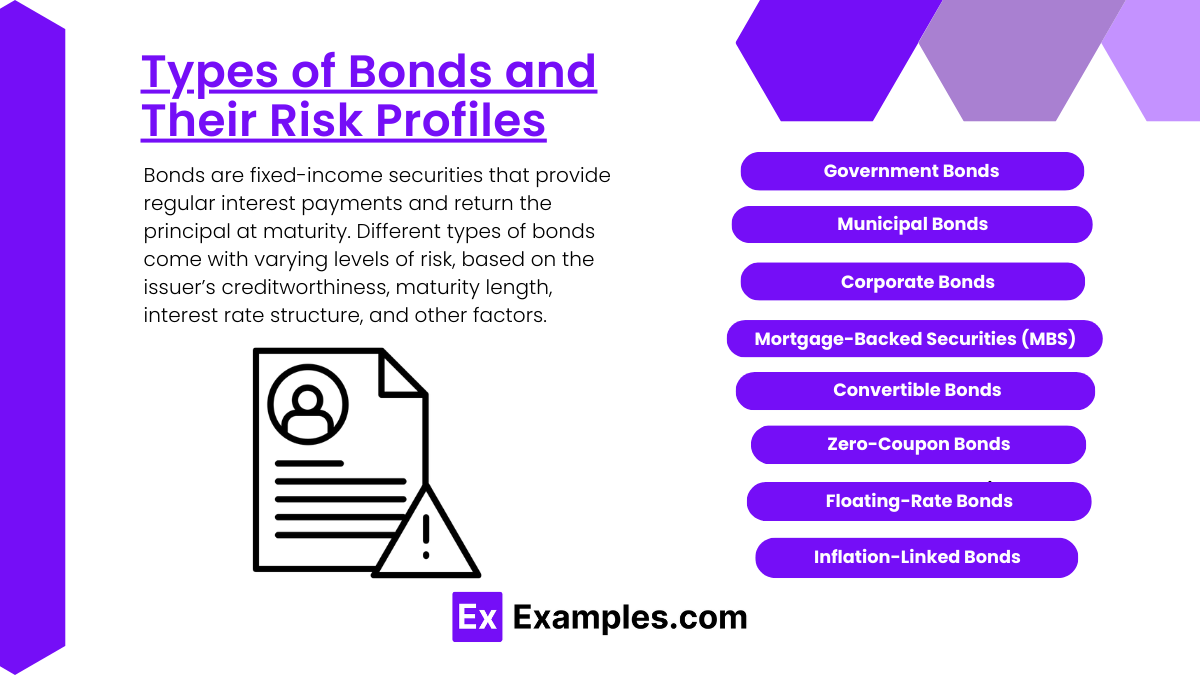

Types of Bonds and Their Risk Profiles

Bonds are fixed-income securities that provide regular interest payments and return the principal at maturity. Different types of bonds come with varying levels of risk, based on the issuer’s creditworthiness, maturity length, interest rate structure, and other factors. Here’s a look at the main types of bonds and their associated risk profiles.

1. Government Bonds

Government bonds are issued by national governments to finance operations or specific projects. They are typically considered low-risk investments, especially in economically stable countries.

- Risk Profile: Low risk, as governments have a high capacity to repay their debt. However, inflation risk and interest rate risk can affect returns.

2. Municipal Bonds

Municipal bonds, or “munis,” are issued by state or local governments to fund public projects such as schools, highways, and infrastructure.

- Risk Profile: Generally low to moderate risk, depending on the financial stability of the issuing municipality. They are also subject to interest rate and, in some cases, credit risk.

3. Corporate Bonds

Corporate bonds are issued by companies to raise capital for expansion, acquisitions, or other expenses. They carry higher risk than government and municipal bonds due to the potential for default.

- Risk Profile: Varies based on the issuing company’s financial health. Investment-grade corporate bonds have lower credit risk, while high-yield or “junk” bonds carry higher credit and default risk.

4. Mortgage-Backed Securities (MBS)

Mortgage-backed securities are bonds secured by a pool of mortgage loans, often issued by financial institutions. Payments to investors are derived from homeowners’ mortgage payments.

- Risk Profile: Moderate to high risk, with exposure to prepayment risk (early mortgage repayments reduce the bond’s income) and interest rate risk.

5. Convertible Bonds

Convertible bonds are corporate bonds that can be converted into a predetermined number of the issuer’s equity shares. They offer fixed income and potential equity appreciation.

- Risk Profile: Moderate risk, as they carry the credit risk of the issuing company and interest rate risk, but also offer equity-related upside if the company’s stock performs well.

6. Zero-Coupon Bonds

Zero-coupon bonds do not make periodic interest payments. Instead, they are issued at a discount and mature at face value, with the interest effectively built into the purchase price.

- Risk Profile: Moderate to high risk, as they are highly sensitive to interest rate changes (higher duration risk). Investors are exposed to greater price volatility.

7. Floating-Rate Bonds

Floating-rate bonds have variable interest rates that adjust periodically based on a reference rate, such as the LIBOR or federal funds rate. This feature makes them less sensitive to interest rate changes.

- Risk Profile: Low to moderate interest rate risk, as the coupon adjusts with market rates. Credit risk varies based on the issuer.

8. Inflation-Linked Bonds

Inflation-linked bonds, like Treasury Inflation-Protected Securities (TIPS), adjust their principal based on inflation rates, providing protection against inflation risk.

- Risk Profile: Low credit risk (if issued by stable governments) and low inflation risk. However, they carry interest rate risk.

Examples

Example 1: Government Bonds

Government bonds, such as U.S. Treasury bonds, are issued by national governments to finance public projects and manage national debt. These bonds are considered low-risk investments because they are backed by the full faith and credit of the government. Investors receive regular interest payments, known as coupon payments, and the principal amount is returned at maturity. Government bonds are widely used by investors seeking stability and predictable income.

Example 2: Corporate Bonds

Corporations issue bonds to raise capital for various purposes, such as expanding operations or funding new projects. Corporate bonds typically offer higher yields than government bonds due to the increased risk associated with investing in a corporation. Investors assess the creditworthiness of the issuing company to determine the risk of default. For example, a well-established company may issue bonds with a lower interest rate than a startup with less financial stability, reflecting the risk profile of each issuer.

Example 3: Municipal Bonds

Municipal bonds are issued by states, cities, or other local government entities to fund public projects, such as schools, highways, or hospitals. One key feature of municipal bonds is that interest income is often exempt from federal income tax, and sometimes state and local taxes as well, making them attractive to investors in higher tax brackets. For instance, a city might issue bonds to finance the construction of a new bridge, appealing to investors looking for tax-advantaged income.

Example 4: Convertible Bonds

Convertible bonds are a hybrid type of fixed-income security that gives investors the option to convert their bonds into a predetermined number of the company’s shares at specific times during the bond’s life. This feature allows investors to benefit from potential stock price appreciation while still receiving fixed interest payments. For example, a technology company may issue convertible bonds to raise capital while providing investors with the option to participate in the company’s growth through equity conversion.

Example 5: Zero-Coupon Bonds

Zero-coupon bonds are fixed-income securities that do not pay periodic interest. Instead, they are issued at a discount to their face value and mature at par value. The difference between the purchase price and the face value represents the investor’s return. For example, a zero-coupon bond with a face value of $1,000 might be purchased for $700, providing a $300 return at maturity. These bonds are attractive to investors who do not need immediate income but want to lock in a guaranteed amount to be received in the future.

Practice Questions

Question 1

What is the primary purpose of issuing bonds by corporations?

A) To pay dividends to shareholders

B) To raise capital for operational needs or expansion

C) To reduce the company’s tax burden

D) To purchase equity in other companies

Correct Answer: B) To raise capital for operational needs or expansion.

Explanation: Corporations issue bonds primarily to raise capital for various purposes, such as funding expansion projects, improving infrastructure, or refinancing existing debt. By issuing bonds, a company can secure the necessary funds without diluting ownership through equity issuance. While paying dividends (Option A) and acquiring other companies (Option D) may be reasons for using the funds raised, they are not the primary purpose of bond issuance. Reducing tax burdens (Option C) is not a direct objective of issuing bonds.

Question 2

Which of the following types of bonds is considered the safest investment?

A) Corporate bonds

B) Municipal bonds

C) U.S. Treasury bonds

D) Convertible bonds

Correct Answer: C) U.S. Treasury bonds.

Explanation: U.S. Treasury bonds are considered the safest type of investment because they are backed by the full faith and credit of the U.S. government. This backing minimizes the risk of default, making them highly attractive to risk-averse investors. While municipal bonds (Option B) are also relatively safe, they carry some credit risk depending on the issuing municipality. Corporate bonds (Option A) can vary significantly in risk depending on the issuer’s financial stability, and convertible bonds (Option D) introduce additional complexities related to both equity and fixed-income markets.

Question 3

What is a key feature of zero-coupon bonds?

A) They pay regular interest payments.

B) They are sold at par value.

C) They are issued at a discount to their face value.

D) They have a fixed maturity date.

Correct Answer: C) They are issued at a discount to their face value.

Explanation: Zero-coupon bonds are a type of bond that does not pay periodic interest payments (Option A). Instead, they are sold at a discount to their face value, meaning that an investor purchases the bond for less than its maturity value. At maturity, the investor receives the full face value of the bond, with the difference representing the interest earned. This feature distinguishes zero-coupon bonds from other bond types, which typically provide regular interest payments. While zero-coupon bonds do have a fixed maturity date (Option D), the key defining characteristic is their issuance at a discount. They are not sold at par value (Option B), which further reinforces the correct answer.