Fixed-Income Active Management: Credit Strategies

Preparing for the CFA Exam involves a solid understanding of Fixed-Income Active Management, with a focus on Credit Strategies. Mastery of credit risk assessment, bond selection, and sector rotation is essential. This knowledge aids in identifying high-yield opportunities, managing credit risk, and enhancing portfolio performance, which is crucial for a high CFA score.

Learning Objective

In studying “Fixed-Income Active Management: Credit Strategies” for the CFA Exam, you should learn to evaluate the strategies that enhance returns through active credit risk management. Understand methods such as sector rotation, credit quality analysis, and issuer selection to optimize portfolio performance. Analyze credit spreads, relative value assessments, and default risks within various fixed-income sectors. Evaluate the role of ratings, yield curves, and economic conditions in shaping credit strategy decisions. Additionally, explore how these strategies adjust to market cycles, manage exposure to credit events, and contribute to risk-adjusted returns, applying these insights to CFA-level practice scenarios.

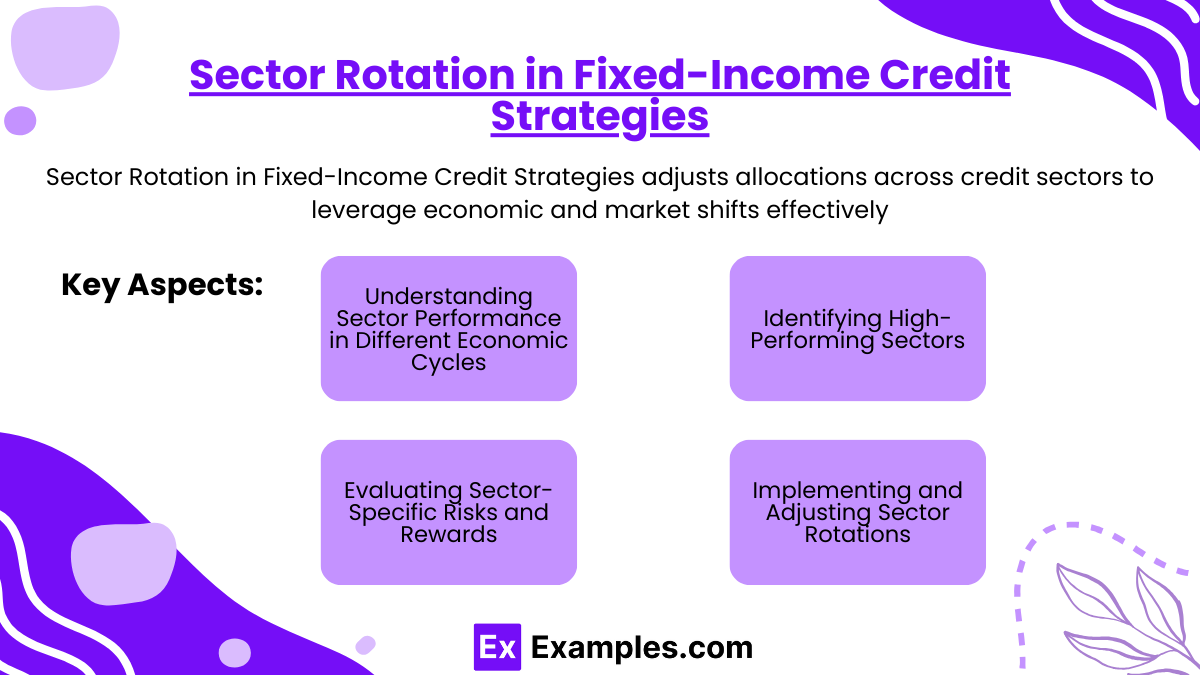

Sector Rotation in Fixed-Income Credit Strategies

Sector Rotation in Fixed-Income Credit Strategies involves actively adjusting portfolio allocations among different sectors within the credit market to capitalize on economic and market cycle shifts. Unlike passive strategies, sector rotation requires a deep understanding of how various credit sectors—such as corporate bonds, municipal bonds, high-yield bonds, and mortgage-backed securities—respond to economic changes. Here’s a breakdown of the key aspects:

- Understanding Sector Performance in Different Economic Cycles

Each sector within fixed-income markets has unique sensitivities to economic conditions. For example, high-yield bonds tend to perform well during economic expansion when default risk is low, while government bonds may be preferred during recessions for their stability. Successful sector rotation involves predicting these cycles to optimize returns. - Identifying High-Performing Sectors

Sector rotation strategies aim to identify sectors expected to outperform based on credit spreads, interest rates, and macroeconomic trends. By increasing exposure to sectors likely to experience spread tightening or price appreciation, portfolio managers can enhance returns. - Evaluating Sector-Specific Risks and Rewards

Each credit sector comes with distinct risk factors, such as credit risk, interest rate sensitivity, and liquidity. Sector rotation strategies assess these risks and balance them against potential returns, allowing investors to take advantage of market opportunities while managing exposure. - Implementing and Adjusting Sector Rotations

Sector rotation in fixed-income credit strategies is a dynamic process, with managers continuously monitoring economic indicators and market signals to make adjustments. Effective sector rotation requires frequent re-evaluation of allocations to remain aligned with economic forecasts and market conditions.

Sector rotation strategies help fixed-income managers capitalize on market inefficiencies, adjust to changes in economic conditions, and maximize risk-adjusted returns within credit portfolios

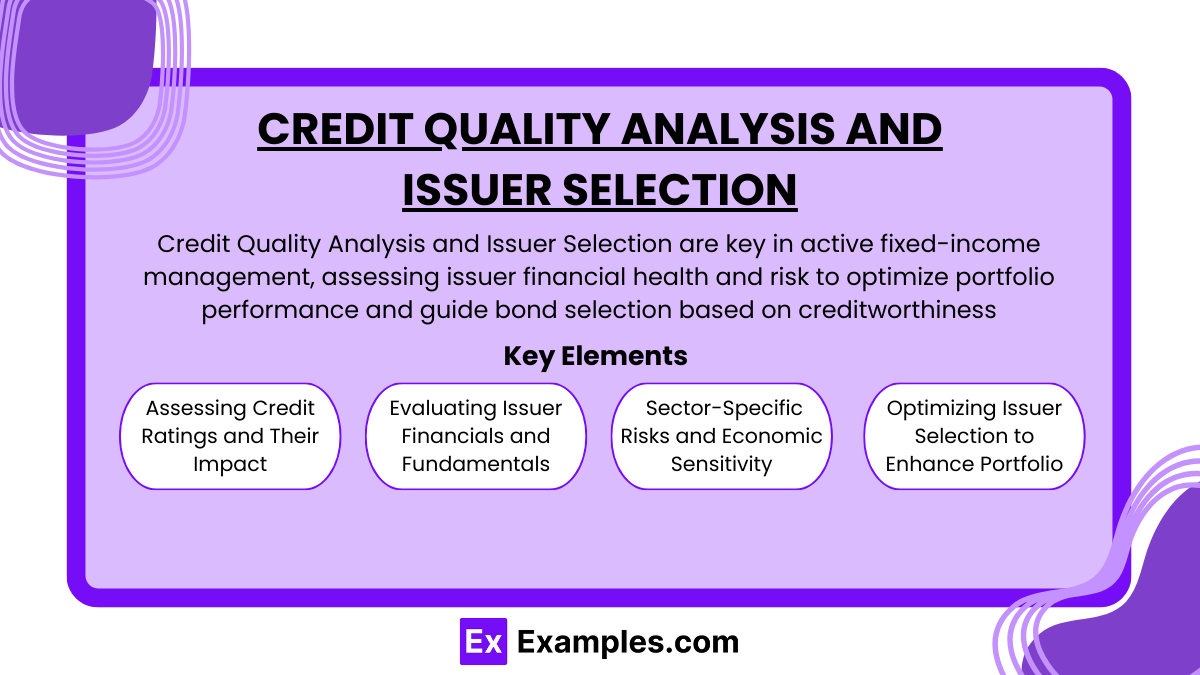

Credit Quality Analysis and Issuer Selection

Credit Quality Analysis and Issuer Selection are crucial components in active fixed-income management, focusing on evaluating the financial health and risk profile of bond issuers to optimize portfolio performance. This process allows investors to make informed decisions on which bonds to hold, based on the creditworthiness of the entities issuing the bonds.

Key Elements of Credit Quality Analysis and Issuer Selection:

- Assessing Credit Ratings and Their Impact

Credit ratings, provided by agencies like Moody’s, S&P, and Fitch, serve as a quick indicator of an issuer’s creditworthiness. Higher-rated bonds (e.g., AAA) are generally seen as lower risk but offer lower yields, while lower-rated bonds (e.g., BB or below, commonly referred to as “junk bonds”) carry higher yields but come with greater risk. Analyzing credit ratings helps investors gauge the level of risk associated with different issuers, informing decisions on bond selection based on risk tolerance and return objectives. - Evaluating Issuer Financials and Fundamentals

Beyond credit ratings, investors conduct in-depth financial analyses of issuers to assess their ability to meet debt obligations. This includes reviewing financial statements to evaluate revenue, profit margins, cash flow stability, and debt levels. Key ratios, such as the debt-to-equity ratio and interest coverage ratio, help investors determine the issuer’s financial stability and resilience to economic downturns. - Understanding Sector-Specific Risks and Economic Sensitivity

Credit quality can also be influenced by the issuer’s sector and the broader economic environment. For example, issuers in sectors like utilities or healthcare may be more stable in downturns, while those in cyclical industries like manufacturing or retail may be more vulnerable. Sector-specific factors such as regulation, competition, and economic sensitivity must be considered when selecting issuers, as these factors influence the likelihood of default and overall investment risk. - Optimizing Issuer Selection to Enhance Portfolio Performance

With a clear understanding of each issuer’s credit quality and risk profile, managers can strategically select bonds that align with the portfolio’s return and risk objectives. This selection process may involve balancing high-quality, stable issuers with higher-yielding, riskier issuers to create a diversified portfolio that achieves optimal risk-adjusted returns. By focusing on issuers with strong fundamentals and favorable credit outlooks, managers can reduce the likelihood of defaults and improve overall portfolio resilience.

Through thorough credit quality analysis and strategic issuer selection, active managers can build a portfolio that not only maximizes returns but also mitigates risk, providing stability and performance across various market conditions

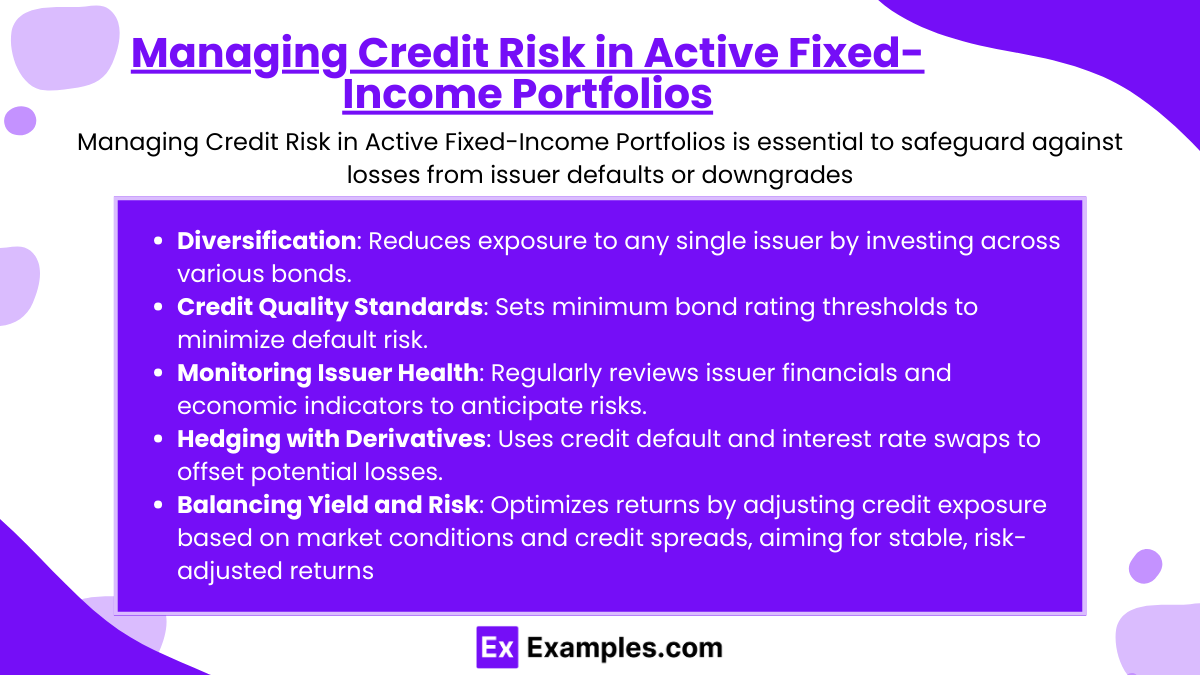

Managing Credit Risk in Active Fixed-Income Portfolios

Managing Credit Risk in Active Fixed-Income Portfolios is a critical process aimed at protecting investments from losses due to issuer defaults or credit downgrades. By actively managing credit risk, portfolio managers can mitigate the impact of unfavorable credit events and enhance the portfolio’s stability and risk-adjusted returns.

Techniques for Reducing Credit Risk Exposure

- Diversification: One of the primary ways to reduce credit risk is by diversifying across issuers, industries, and geographic regions. By spreading investments across various bonds, managers can reduce the portfolio’s exposure to any single issuer’s credit risk.

- Credit Quality Requirements: Many portfolios set minimum credit quality standards, investing only in bonds with ratings above a specific threshold. This approach minimizes exposure to lower-quality issuers and reduces the likelihood of holding bonds that may default.

Monitoring Default Risks and Credit Events

- Continuous Monitoring of Issuer Health: Active management requires regular review of each issuer’s financial and operational health, which includes tracking their earnings reports, debt levels, and other financial metrics. Early identification of negative trends can help managers make timely decisions.

- Sector and Economic Analysis: Beyond individual issuers, managers must monitor broader economic indicators and sector performance. A sector downturn can impact all issuers within it, even those with strong individual fundamentals.

Hedging Credit Risk with Derivatives

- Credit Default Swaps (CDS): CDS contracts allow managers to hedge against the risk of default by essentially buying insurance on a bond. If the bond issuer defaults, the CDS provider compensates for the losses, offsetting the impact on the portfolio.

- Interest Rate Swaps: Changes in interest rates can influence the credit risk environment. Managers may use interest rate swaps to protect against interest rate movements that could negatively impact credit-sensitive bonds.

Balancing Risk-Adjusted Returns in Credit Strategies

- Optimizing Yield vs. Risk: Active managers assess the trade-off between pursuing higher yields and controlling credit risk. Higher yields may come with greater risk, so the challenge lies in finding bonds that offer attractive returns while aligning with the portfolio’s risk tolerance.

- Dynamic Adjustments: Managers adjust credit exposure based on market conditions, issuer fundamentals, and credit spread movements. This flexibility allows for timely shifts in portfolio composition, aiming to avoid credit risk spikes while maintaining performance

Examples

Example 1

A portfolio manager identifies that the technology sector is experiencing strong earnings growth and tightening credit spreads. They increase exposure to investment-grade technology bonds, expecting continued spread compression as investor demand increases. This sector rotation strategy aims to capture price appreciation from improving credit quality in this sector.

Example 2

During an economic slowdown, the manager shifts from lower-rated corporate bonds to higher-quality government bonds to mitigate default risk. This strategy reduces exposure to credit risk by avoiding sectors likely to under perform in a downturn, focusing on assets with lower credit risk and greater stability.

Example 3

A manager uses credit spread analysis to identify bonds with unusually wide spreads relative to peers in the same credit rating. They purchase these bonds, expecting the spreads to narrow as the market reassesses the issuer’s risk, which would increase the bond’s price. This relative value strategy helps capture gains from market inefficiencies.

Example 4

The portfolio manager implements a hedging strategy using credit default swaps (CDS) to protect against potential defaults in the energy sector, which is facing declining oil prices. By purchasing CDS contracts, the manager reduces the portfolio’s exposure to credit events in this sector, preserving returns while managing risk.

Example 5

As the yield curve steepens, indicating expectations of economic growth, the manager increases allocation to long-duration corporate bonds in sectors likely to benefit from expansion. The strategy aims to capture higher yields while capitalizing on improved credit conditions, balancing duration risk with credit quality considerations to enhance portfolio yield.

Practice Questions

Question 1

Which of the following is a primary objective of credit spread analysis in fixed-income active management?

A) To identify bonds with the highest possible yield regardless of risk

B) To assess the risk premium investors demand over risk-free bonds

C) To calculate the impact of interest rate changes on bond prices

D) To determine the liquidity of corporate bonds

Answer: B) To assess the risk premium investors demand over risk-free bonds

Explanation: Credit spread analysis focuses on understanding the additional yield investors require for taking on credit risk beyond a risk-free asset, such as a government bond. This spread reflects the credit risk associated with a particular bond and allows managers to assess if the yield offered justifies the associated risk.

Question 2

A fixed-income portfolio manager anticipates an economic downturn and decides to reduce exposure to high-yield bonds. This is an example of:

A) Sector rotation strategy

B) Credit spread compression

C) Credit quality shift

D) Duration adjustment

Answer: C) Credit quality shift

Explanation: In anticipation of a downturn, the manager is moving away from high-yield (riskier) bonds to safer bonds, which is a credit quality shift. This strategy helps reduce credit risk exposure, as high-yield bonds are generally more vulnerable to economic downturns.

Question 3

Which tool would a portfolio manager use to hedge against the default risk of a particular bond issuer in a credit strategy?

A) Yield curve analysis

B) Interest rate swaps

C) Credit default swaps

D) Sector rotation

Answer: C) Credit default swaps

Explanation: Credit default swaps (CDS) are financial instruments specifically designed to provide protection against credit events, such as defaults. By purchasing a CDS, the manager can hedge against the risk that a particular issuer will default, making it an effective tool for managing credit risk in a fixed-income portfolio.