A Simple Model For Bonds

Preparing for the CMT Exam requires a strong grasp of “A Simple Model for Bonds,” a key aspect of fixed-income analysis. Mastery of bond pricing, yield curves, and interest rate risk is crucial. This knowledge enables effective evaluation of bond market behavior, risk management, and investment strategies, essential for achieving success in technical analysis.

Learning Objective

In studying “A Simple Model for Bonds” for the CMT Level 2 Exam, you should learn to understand key aspects of fixed-income securities, including bond pricing models, yield curves, and duration analysis. Evaluate how these tools assess interest rate risk, bond valuation, and market dynamics. Analyze the relationship between interest rates and bond prices, including convexity and sensitivity. Additionally, explore how bond market models inform investment decisions, risk management strategies, and market timing. Apply your knowledge by interpreting yield spreads, bond market cycles, and real-world scenarios in CMT practice exams and market selection strategies in Section V.

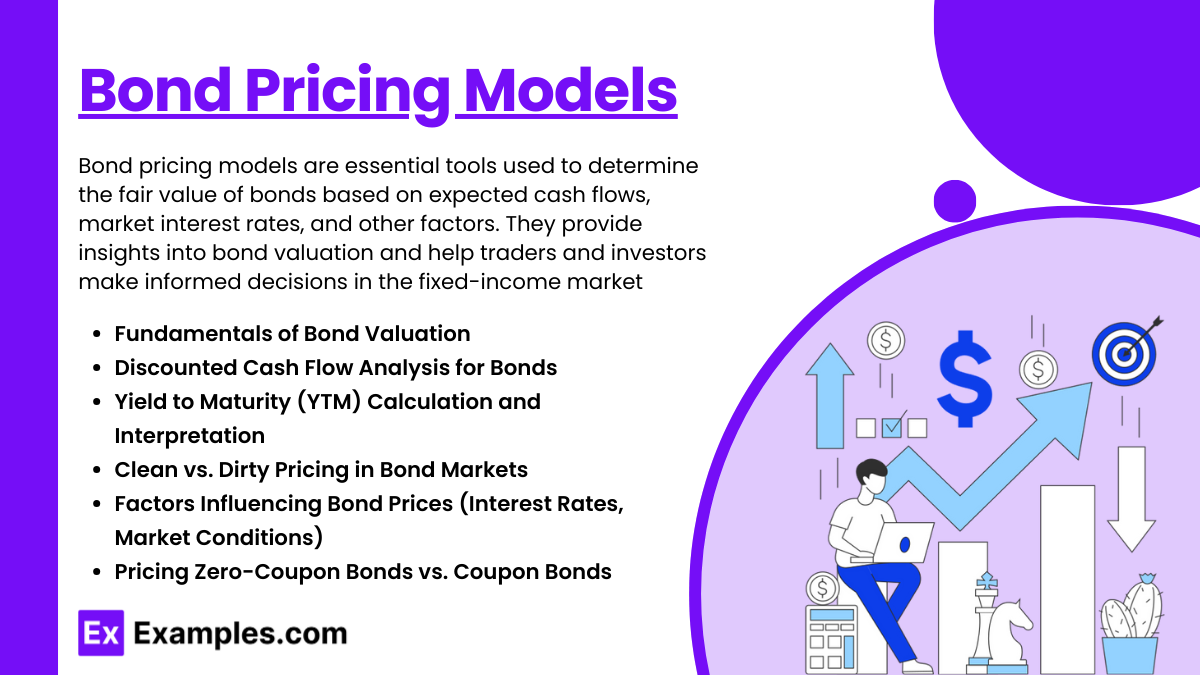

Bond Pricing Models

Bond pricing models are essential tools used to determine the fair value of bonds based on expected cash flows, market interest rates, and other factors. They provide insights into bond valuation and help traders and investors make informed decisions in the fixed-income market. Here’s a detailed explanation of key concepts:

- Fundamentals of Bond Valuation: The price of a bond is typically the present value of its future cash flows, including periodic coupon payments and the principal (face value) upon maturity. These cash flows are discounted at an appropriate interest rate (or discount rate) to reflect their present value.

- Discounted Cash Flow Analysis for Bonds: This technique involves calculating the present value of all future cash flows generated by a bond. For a bond with fixed coupon payments, the discounted cash flow model sums the present value of each payment using a discount rate that reflects the bond’s risk and prevailing market interest rates.

- Yield to Maturity (YTM) Calculation and Interpretation: Yield to maturity represents the internal rate of return (IRR) earned by an investor who purchases a bond at its current price and holds it until maturity. YTM considers all coupon payments and the difference between the bond’s purchase price and its face value. It helps compare different bonds with varying characteristics.

- Clean vs. Dirty Pricing in Bond Markets: Bond prices are often quoted as either “clean” or “dirty.” The clean price excludes accrued interest since the last coupon payment, while the dirty price (also known as the full price) includes accrued interest. The dirty price is the actual amount paid for the bond when purchased between coupon payments.

- Factors Influencing Bond Prices (Interest Rates, Market Conditions): Bond prices are inversely related to market interest rates. When interest rates rise, existing bond prices generally fall because their fixed coupon payments become less attractive compared to newer bonds with higher yields. Other factors, such as credit risk and market conditions, also affect bond prices.

- Pricing Zero-Coupon Bonds vs. Coupon Bonds: Zero-coupon bonds are sold at a discount to their face value and do not make periodic interest payments. Instead, the investor receives a lump sum at maturity. Coupon bonds, on the other hand, make periodic interest payments based on a specified coupon rate. The pricing models for these bond types differ based on their cash flow structure.

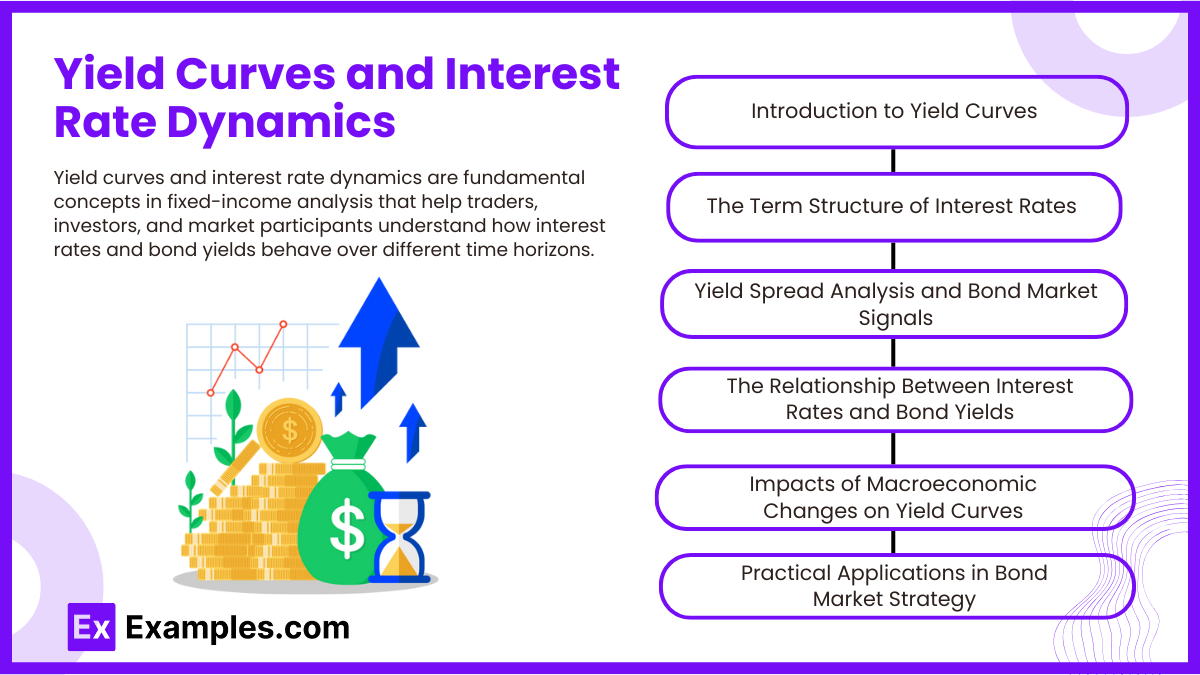

Yield Curves and Interest Rate Dynamics

Yield curves and interest rate dynamics are fundamental concepts in fixed-income analysis that help traders, investors, and market participants understand how interest rates and bond yields behave over different time horizons. These concepts provide critical insights into market sentiment, economic conditions, and potential investment opportunities. Here’s an in-depth explanation:

- Introduction to Yield Curves (Normal, Inverted, and Flat Curves): A yield curve is a graphical representation that shows the relationship between bond yields (interest rates) and maturities. A normal yield curve slopes upward, indicating that longer-term bonds offer higher yields due to increased risk over time. An inverted yield curve slopes downward, often signaling potential economic slowdowns or recessions. A flat curve suggests minimal differences in yields across various maturities and can indicate market uncertainty.

- The Term Structure of Interest Rates and Its Significance: The term structure of interest rates explains how bond yields vary with different maturities. It reflects market expectations for future interest rates, economic growth, and inflation. This concept is essential for investors as it influences borrowing costs, the valuation of financial instruments, and overall investment strategy.

- Yield Spread Analysis and Bond Market Signals: Yield spreads refer to the difference in yields between different bonds, such as corporate bonds and government bonds or bonds of varying maturities. Changes in yield spreads provide signals about market sentiment, risk appetite, and economic expectations. For instance, a widening spread between corporate and government bonds may indicate increased risk aversion among investors.

- The Relationship Between Interest Rates and Bond Yields: Bond prices and yields have an inverse relationship. When interest rates rise, bond prices generally fall, causing yields to increase. Conversely, when interest rates decrease, bond prices rise, and yields fall. This dynamic is crucial for bond valuation and portfolio management as changes in interest rates can significantly impact bond returns.

- Impacts of Macroeconomic Changes on Yield Curves: Macroeconomic factors such as inflation, economic growth, central bank policies, and geopolitical events can influence the shape and movement of the yield curve. For example, central bank rate hikes often lead to upward shifts in short-term rates, affecting the overall shape of the yield curve.

- Practical Applications in Bond Market Strategy: Yield curves are used by investors to make strategic decisions, such as bond laddering, maturity selection, and interest rate risk management. Understanding yield curves helps traders identify opportunities to invest in bonds with favorable yield spreads and manage exposure to interest rate fluctuations.

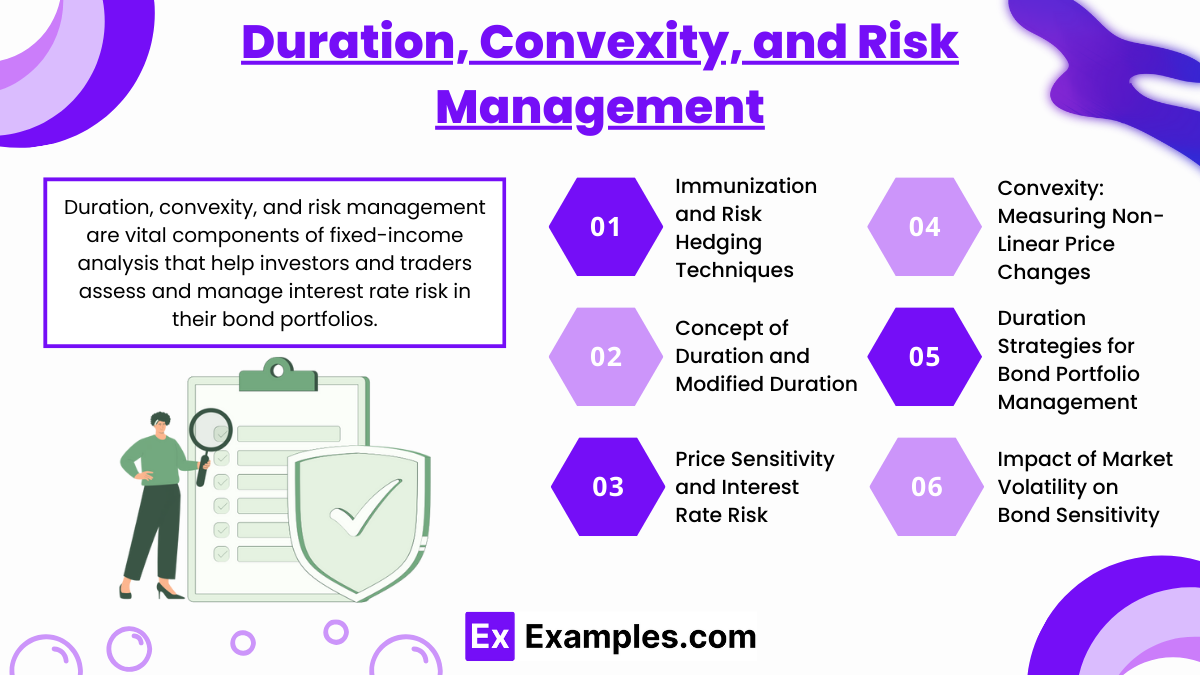

Duration, Convexity, and Risk Management

Duration, convexity, and risk management are vital components of fixed-income analysis that help investors and traders assess and manage interest rate risk in their bond portfolios. These concepts enable a deeper understanding of how bond prices react to changes in interest rates and provide strategies to mitigate risks. Here’s an in-depth explanation:

- Concept of Duration and Modified Duration: Duration measures the sensitivity of a bond’s price to changes in interest rates. It represents the weighted average time it takes to receive a bond’s cash flows (both interest payments and principal repayment). Modified duration quantifies the percentage change in a bond’s price for a 1% change in yield. It provides an estimate of interest rate risk—bonds with higher durations are more sensitive to rate changes.

- Price Sensitivity and Interest Rate Risk: Duration is a key indicator of price sensitivity. When interest rates rise, bond prices fall, and vice versa. The extent of this price change depends on the bond’s duration. Investors use duration as a measure to gauge their exposure to interest rate movements and adjust their portfolios accordingly to minimize potential losses.

- Convexity: Measuring Non-Linear Price Changes: Convexity is a measure of the curvature in the relationship between bond prices and changes in interest rates. While duration provides a linear approximation of price changes, convexity accounts for the fact that price-yield relationships are non-linear. Bonds with higher convexity experience greater price increases when interest rates fall and smaller price declines when rates rise, making them more attractive in a volatile market.

- Duration Strategies for Bond Portfolio Management: Portfolio managers use duration strategies to align their portfolios with interest rate expectations. For example, shortening the duration of a bond portfolio reduces interest rate sensitivity, which is beneficial when interest rates are expected to rise. Conversely, extending duration increases sensitivity and can generate higher returns if rates decline.

- Immunization and Risk Hedging Techniques: Immunization strategies seek to protect bond portfolios from adverse interest rate movements by matching asset and liability durations. This technique ensures that changes in interest rates have a minimal impact on the portfolio’s value, providing stability and predictability. Risk hedging can also involve the use of derivatives, such as interest rate swaps, to offset exposure.

- Impact of Market Volatility on Bond Sensitivity: Market volatility can amplify the effects of duration and convexity. When interest rates are highly volatile, bonds with higher convexity tend to offer better price stability, making convexity an important consideration for risk management.

Application in Market Selection and Strategy

The application of bond models in market selection and strategy involves using various analytical tools and methods to make informed investment decisions, manage risks, and optimize portfolio performance in the bond market. This approach integrates theoretical models with practical considerations to adapt to changing market dynamics. Here’s a detailed explanation:

- Assessing Bond Market Cycles and Trends: Understanding market cycles and trends is crucial for identifying the best times to invest in bonds. Investors analyze economic cycles, interest rate environments, and historical performance to anticipate market shifts. For example, during economic downturns, defensive bonds or high-quality bonds may be preferred, while riskier bonds might be chosen in periods of economic growth.

- Real-World Scenarios for Bond Investing: Applying bond models to real-world scenarios involves interpreting current economic data, interest rate trends, and market sentiment to make sound investment decisions. For example, changes in central bank policies or macroeconomic indicators may prompt adjustments in bond allocations, such as moving from short-duration to long-duration bonds or shifting between different bond sectors.

- Using Bond Models for Market Timing Decisions: Accurate market timing is key to maximizing returns and minimizing risk in bond investments. Bond models help investors identify favorable entry and exit points by analyzing yield curves, interest rate trends, and market conditions. Effective market timing allows investors to benefit from shifts in interest rates, inflation expectations, or other market variables.

- Interpreting Yield Spreads for Market Opportunities: Yield spread analysis compares the yields of different bonds, such as corporate bonds versus government bonds or bonds with different maturities. Wider spreads often indicate higher risk and potential opportunity for higher returns. By analyzing yield spreads, investors can identify under- or overvalued bonds, assess risk, and make strategic decisions on bond selection and allocation.

- Integrating Bond Models in Risk Management Frameworks: Risk management is a critical component of market strategy, and bond models provide tools to manage interest rate risk, credit risk, and market volatility. For example, duration and convexity can be used to assess a portfolio’s sensitivity to interest rate changes, while derivatives like interest rate swaps can help hedge against unfavorable movements.

- Practical Case Studies and Examples in Fixed-Income Analysis: Real-world case studies illustrate how bond models perform under different market conditions, such as economic expansions, recessions, or changes in monetary policy. Studying these examples helps investors refine their strategies, understand the limitations and strengths of various models, and apply lessons learned to future market scenarios.

Examples

Example 1: Assessing Economic Cycles for Bond Allocation

An investor applies bond models to analyze macroeconomic indicators such as GDP growth, inflation, and interest rates. During economic expansion, they allocate a higher proportion of their portfolio to high-yield corporate bonds, while shifting towards safer government bonds or shorter-duration securities during recessions, managing risk and optimizing returns based on economic cycles.

Example 2: Yield Spread Analysis for Market Opportunities

A trader observes a widening spread between corporate bonds and government bonds, indicating increased market risk aversion. By leveraging this analysis, the trader reduces exposure to riskier corporate bonds and shifts capital towards high-grade government securities, seeking to balance return potential with risk management in volatile market conditions.

Example 3: Using Duration and Convexity for Risk Management

A portfolio manager uses duration and convexity measures to adjust a bond portfolio’s interest rate sensitivity. Anticipating rising interest rates, they reduce exposure to long-term bonds and increase holdings in short-term bonds, minimizing potential price declines while maintaining income generation through yield optimization.

Example 4: Market Timing with Yield Curve Movements

An investor notices an inverted yield curve, historically a potential signal of economic downturns. In response, they shift their investments from long-term bonds to shorter maturities and high-quality assets, aiming to reduce exposure to market volatility and preserve capital during periods of uncertainty.

Example 5: Applying Real-World Scenarios for Bond Strategy

Following a central bank’s announcement of an interest rate hike, an investor uses bond models to adjust their portfolio by focusing on higher-yield and shorter-maturity bonds. This approach mitigates the impact of rising rates on bond prices and seeks to optimize returns in the new interest rate environment.

Practice Questions

Question 1:

Which of the following best describes the primary use of bond models for market timing decisions?

A) To assess the creditworthiness of a bond issuer

B) To identify favorable entry and exit points in bond investments

C) To analyze historical yield spreads for future predictions

D) To calculate a bond’s intrinsic value

Answer: B) To identify favorable entry and exit points in bond investments

Explanation:

Bond models help investors make market timing decisions by analyzing trends, interest rate movements, and market conditions to identify when to buy or sell bonds. This is essential for maximizing returns and minimizing risks. While historical yield spreads (C) and creditworthiness (A) analysis are important, market timing primarily focuses on optimal entry and exit strategies.

Question 2:

Yield spread analysis is most useful for which of the following purposes in bond market strategy?

A) Predicting the duration of a bond

B) Evaluating differences between bond yields to assess risk and opportunity

C) Determining the present value of future cash flows

D) Identifying macroeconomic indicators that influence stock prices

Answer: B) Evaluating differences between bond yields to assess risk and opportunity

Explanation:

Yield spread analysis involves comparing the yields of different bonds to understand risk differentials, potential returns, and market sentiment. It helps investors identify over- or undervalued bonds and informs strategic decisions. Duration (A) and present value calculations (C) serve different purposes, and macroeconomic indicators influencing stock prices (D) fall outside the scope of yield spread analysis.

Question 3:

When applying bond models to real-world scenarios, which factor is most critical to consider for effective market selection?

A) Currency exchange rates

B) Historical performance of unrelated asset classes

C) Current economic data and interest rate trends

D) Seasonal patterns in stock market activity

Answer: C) Current economic data and interest rate trends

Explanation:

Effective market selection with bond models requires analyzing current economic data and interest rate trends, as these factors significantly impact bond prices and yields. Currency exchange rates (A) and unrelated asset classes (B) are less directly relevant, while stock market seasonality (D) does not directly apply to bond market strategies.