Economic Growth

Economic growth is the increase in a nation’s output of goods and services over time, typically measured by the growth rate of real GDP. In AP Macroeconomics, understanding the factors that drive economic growth, such as capital accumulation, technological advancements, and improved productivity, is essential for analyzing long-term economic performance. Growth fosters higher living standards, job creation, and increased government revenue. However, it also presents challenges, including managing inflation, income inequality, and environmental sustainability, all of which are important considerations in macroeconomic analysis.

Learning Objectives

For the topic of Economic Growth in AP Macroeconomics, you should learn how to analyze the factors that contribute to GDP growth, including capital accumulation, technological advancements, and labor productivity. You should understand different growth models like the Solow-Swan model and endogenous growth theory. Additionally, study the role of government policies, investment in infrastructure, and foreign trade in promoting growth. Finally, recognize the benefits and limitations of economic growth, such as its impact on living standards, income inequality, and environmental sustainability.

Introduction Economic growth refers to the increase in the amount of goods and services produced per head of the population over a period of time. It is typically measured by the growth rate of a nation’s Gross Domestic Product (GDP). Economic growth is a critical aspect of a country’s economic health as it contributes to higher living standards, more job opportunities, and improved public services. Understanding the factors that influence economic growth is essential for policymakers to promote sustainable development and for students aiming to excel in the AP Macroeconomics Exam.Key Components of Economic Growth

Gross Domestic Product (GDP) Growth

- GDP is the total value of all goods and services produced in a country within a specific period.

- Economic growth is commonly measured by the annual percentage change in real GDP, which adjusts for inflation to reflect the true value of growth.

- A sustained rise in GDP indicates an expanding economy, while negative growth suggests economic contraction.

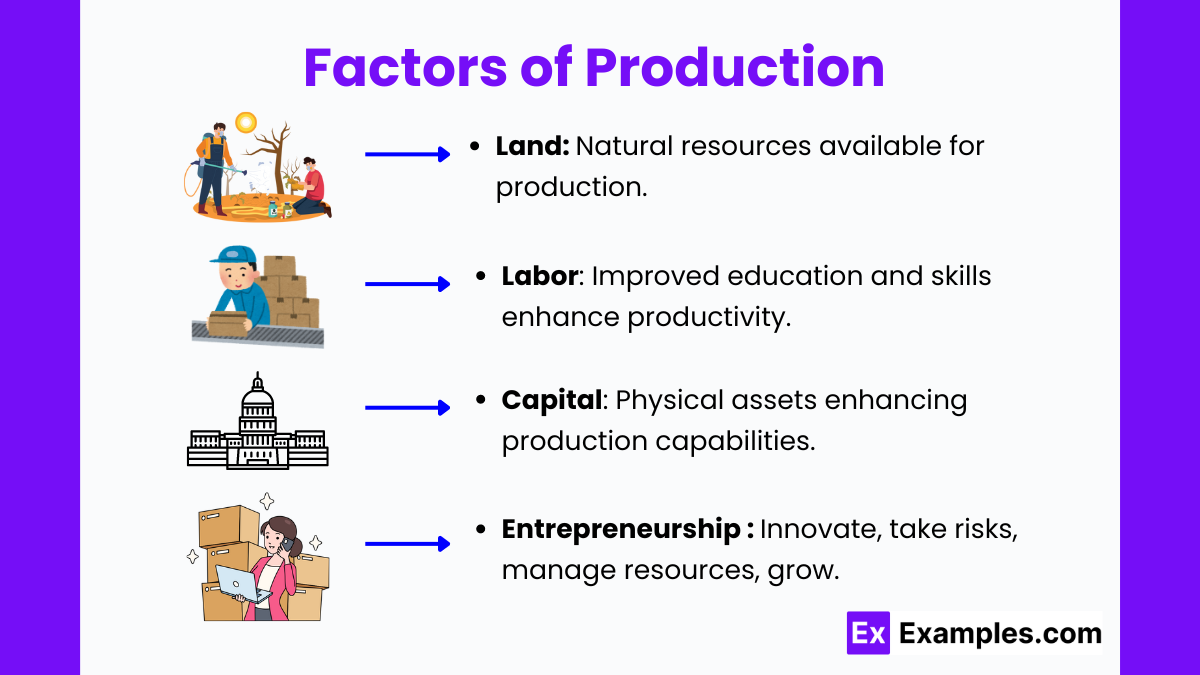

Factors of Production

Economic growth is driven by the efficient use of the four factors of production:

- Land: Natural resources available for production.

- Labor: The workforce; improvements in education and skills enhance labor productivity.

- Capital: Physical tools, machinery, and infrastructure that boost production capabilities.

- Entrepreneurship: The ability to innovate, take risks, and efficiently manage resources to drive growth.

Productivity and Technological Advancements

- Productivity refers to the output per unit of input (e.g., per labor hour). When workers and industries become more productive, the economy can produce more goods and services with the same level of inputs.

- Technological advancements are central to boosting productivity. Innovations in machinery, automation, and software allow firms to operate more efficiently, reducing costs and increasing output.

- The role of education and training, as well as investment in research and development (R&D), are critical for sustaining long-term growth.

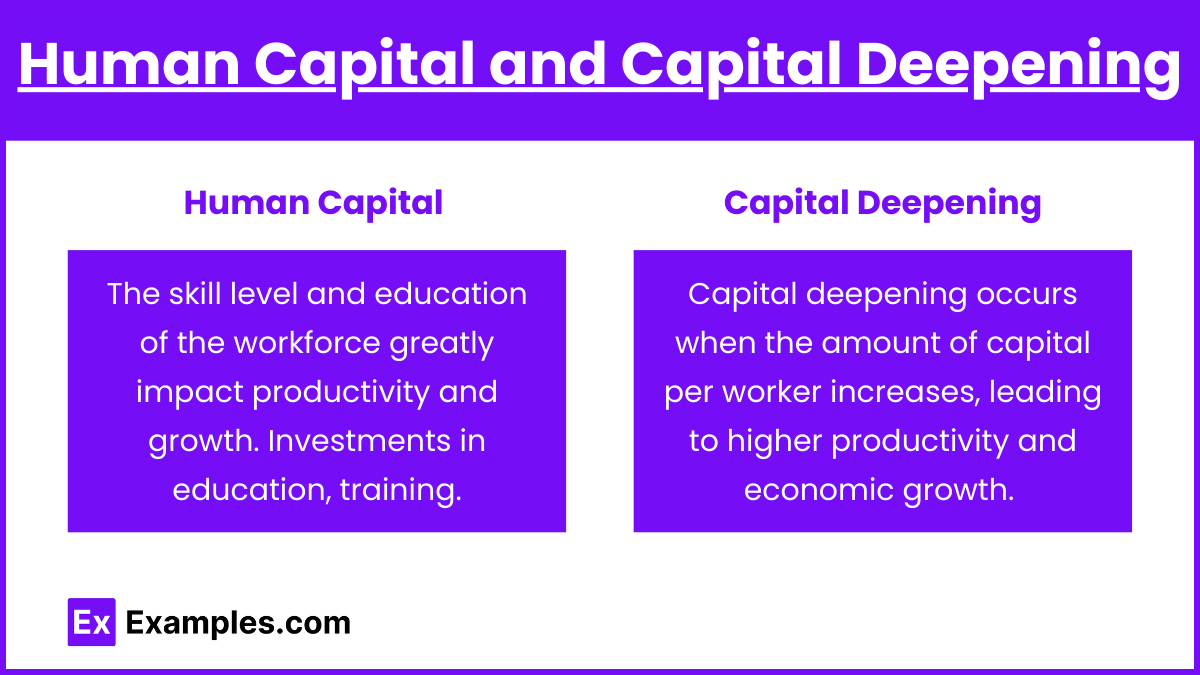

Human Capital and Capital Deepening

- The skill level and education of the workforce greatly impact productivity and growth. Investments in education, training, and health contribute to building human capital, leading to higher output and better quality of work.

- Capital deepening occurs when the amount of capital per worker increases, leading to higher productivity and economic growth. Examples include investing in new machinery or advanced technologies that make production more efficient.

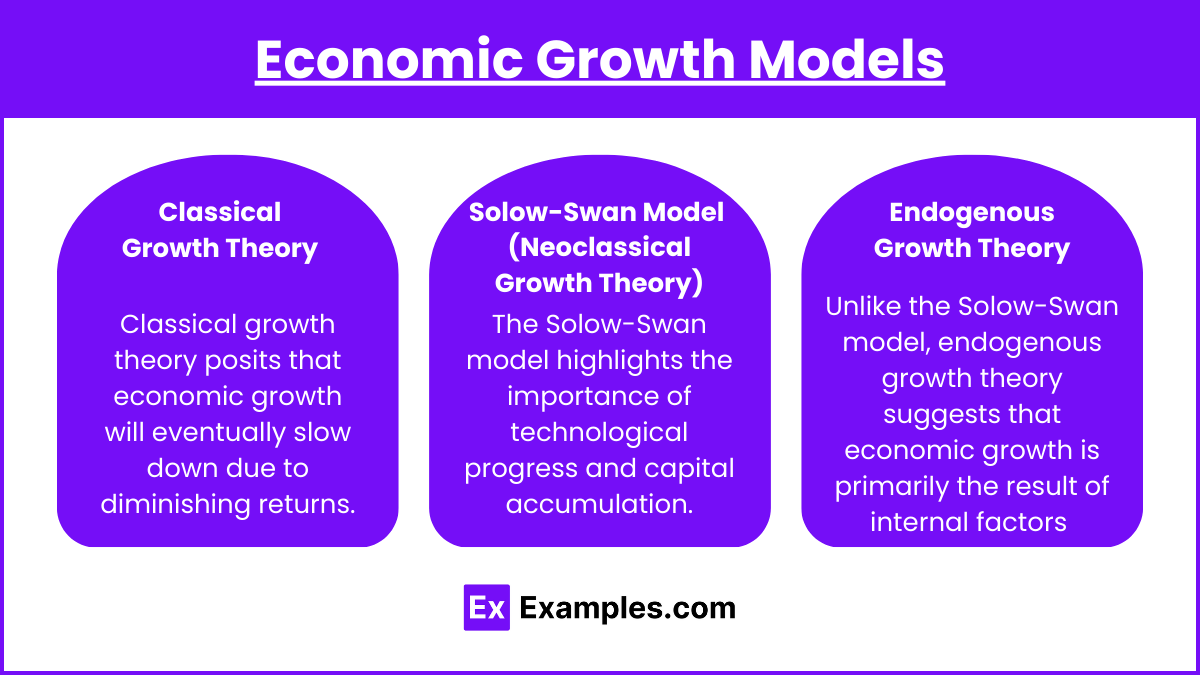

Economic Growth Models

- Classical Growth Theory

- Classical growth theory posits that economic growth will eventually slow down due to diminishing returns. As population grows, resources such as land become more limited, and additional labor contributes less and less to overall output.

- Solow-Swan Model (Neoclassical Growth Theory)

- The Solow-Swan model highlights the importance of technological progress and capital accumulation. It argues that without technological advancements, growth will stagnate as the economy reaches its steady-state level of capital.

- Endogenous Growth Theory

- Unlike the Solow-Swan model, endogenous growth theory suggests that economic growth is primarily the result of internal factors like innovation, human capital development, and knowledge. It emphasizes the role of policies and institutions in sustaining long-term growth.

Benefits of Economic Growth

- Higher Living Standards : Sustained economic growth leads to an increase in the national income, enabling higher consumption levels and improvements in living standards.

- Job Creation : As businesses expand in a growing economy, more jobs are created, reducing unemployment and underemployment rates.

- Government Revenue : Economic growth increases tax revenues, allowing governments to invest more in infrastructure, public services, and social welfare programs.

- Reduction in Poverty :Higher economic growth often leads to a more equitable distribution of wealth and reduces poverty rates, especially when coupled with targeted social policies.

Examples

Example 1: Technological Innovation in Manufacturing

One of the most notable examples of economic growth is the increase in productivity resulting from technological innovation. For instance, the development of automation and robotics in manufacturing industries has significantly boosted production output with the same amount of labor input. This has led to faster growth in GDP as businesses are able to produce more goods at lower costs, which enhances overall economic efficiency and stimulates growth.

Example 2: Investment in Human Capital

Countries that prioritize education and training programs often see substantial economic growth over time. For example, South Korea’s investment in its education system over the past several decades has resulted in a highly skilled labor force, which has driven rapid economic development. The increase in human capital boosts productivity, innovation, and competitiveness in global markets, leading to sustained economic growth.

Example 3: Infrastructure Development

Investment in infrastructure such as highways, airports, and public transportation systems can lead to significant economic growth. China’s focus on large-scale infrastructure projects, including the construction of high-speed rail networks, has greatly reduced transportation costs, enhanced connectivity between regions, and improved the efficiency of goods and services delivery. These improvements have helped sustain China’s rapid GDP growth over the past decades.

Example 4: Expansion of International Trade

Economic growth can also result from opening up to international trade. Countries that engage in free trade agreements and reduce trade barriers experience increased exports, which contribute to economic expansion. An example is Germany, where the export-driven economy has benefited from global demand for high-quality automobiles and industrial machinery, significantly contributing to its GDP growth.

Example 5: Discovery and Utilization of Natural Resources

Countries that discover and utilize natural resources effectively often see a sharp rise in economic growth. For instance, the discovery of oil reserves in Saudi Arabia transformed its economy from a largely agrarian base to one of the largest oil producers globally. The revenues generated from oil exports have fueled government investments, job creation, and overall growth in GDP, making the country a leading economy in the Middle East.

Multiple Choice Questions

Question 1

Which of the following is the primary factor that drives long-term economic growth?

A) Increase in the money supply

B) Increase in government spending

C) Improvement in technology

D) Decrease in taxesRecommended

Answer: C) Improvement in technology

Explanation: Long-term economic growth is primarily driven by advancements in technology, which improve productivity and efficiency. Technological improvements allow firms to produce more with the same level of input, leading to sustainable increases in output. While increasing the money supply, government spending, or reducing taxes can stimulate short-term growth, they do not ensure sustained growth over the long term like technological advancements do.Conclusion: Technological improvement is critical for sustaining long-term economic growth by continuously boosting productivity.

Question 2

What is the impact of capital deepening on economic growth?

A) It causes inflation to rise.

B) It increases labor productivity.

C) It reduces the amount of natural resources needed.

D) It decreases the marginal cost of production.Recommended

Answer: B) It increases labor productivity

Explanation: Capital deepening refers to the process of increasing the amount of capital (such as machines, tools, and technology) per worker. This boosts labor productivity as workers can produce more output with better tools and equipment. Capital deepening is a key driver of economic growth because it enhances the efficiency of production, leading to higher output per worker.Conclusion: Increasing the capital available to workers is vital for improving labor productivity and, consequently, promoting economic growth.

Question 3

Which of the following is an example of sustainable economic growth?

A) Rapid industrialization that depletes natural resources

B) Investment in renewable energy and green technologies

C) An increase in consumer spending driven by lower interest rates

D) A short-term boost in GDP from government stimulus packagesRecommended

Answer: B) Investment in renewable energy and green technologies

Explanation: Sustainable economic growth occurs when growth is achieved without depleting resources or causing long-term harm to the environment. Investing in renewable energy and green technologies ensures that growth can continue over time without exhausting natural resources or creating environmental damage. Rapid industrialization that depletes resources or temporary increases in GDP from stimulus packages do not represent sustainable growth.