Financial Assets

Financial assets are non-physical assets that represent a claim on future income or wealth, such as stocks, bonds, savings accounts, and mutual funds. In AP Macroeconomics, they play a critical role in the economy by facilitating investment, transferring risk, and promoting liquidity. Understanding financial assets helps explain how money flows between savers and borrowers, influencing economic growth and stability.

Learning Objectives

Understand the types of financial assets (stocks, bonds, mutual funds, savings accounts), their roles in the economy, and how they transfer risk, promote liquidity, and facilitate investment. Focus on how interest rates and monetary policy affect the value and risk of these assets.

Financial Assets

Financial assets are claims on the income or wealth of an entity (like a government, corporation, or individual). Unlike physical assets (like land or machinery), financial assets do not have intrinsic value but derive their value from the contractual claims they represent.

Common examples of financial assets include:

- Stocks

- Bonds

- Savings accounts

- Certificates of deposit (CDs)

- Mutual funds

These assets are essential in the transfer of money from savers (those with excess funds) to borrowers (those in need of funds).

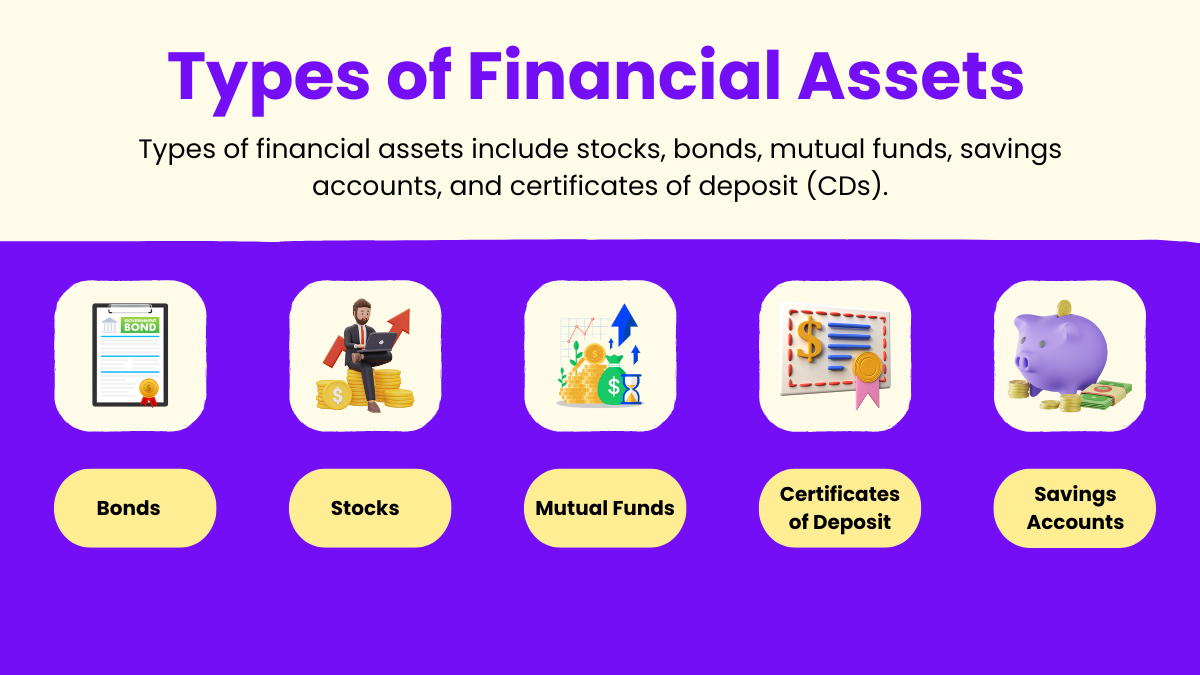

Types of Financial Assets

1. Bonds

- Definition: Bonds are debt securities where the issuer (e.g., government or corporation) promises to pay back the principal (the amount borrowed) along with periodic interest payments.

- Key Features:

- Coupon rate: The interest rate the bondholder receives.

- Maturity date: The date when the bond’s principal is repaid.

- Face value: The original amount borrowed or loaned.

- Government bonds (like U.S. Treasury bonds): Issued by governments to finance expenditures.

- Corporate bonds: Issued by companies to raise capital.

2. Stocks

- Definition: Stocks represent ownership in a company. When you buy a stock, you become a shareholder and own a portion of the company’s equity.

- Types:

- Common stock: Shareholders can vote in corporate decisions and receive dividends, but they are last in line during liquidation.

- Preferred stock: Shareholders have no voting rights but get prioritized for dividend payments.

3. Mutual Funds

- Definition: Mutual funds pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other securities.

- Key Advantages:

- Diversification: Reduces risk by spreading investments across many assets.

- Professional Management: Fund managers decide which assets to invest in on behalf of investors.

4. Certificates of Deposit (CDs)

- Definition: A savings certificate issued by banks with a fixed interest rate and maturity date.

- Key Feature: Offers a higher interest rate than regular savings accounts, but funds are locked until the maturity date.

5. Savings Accounts

- Definition: Low-risk accounts held at financial institutions where individuals can deposit money and earn interest.

- Importance: These accounts are liquid, meaning funds can be easily accessed, but they typically offer lower interest rates.

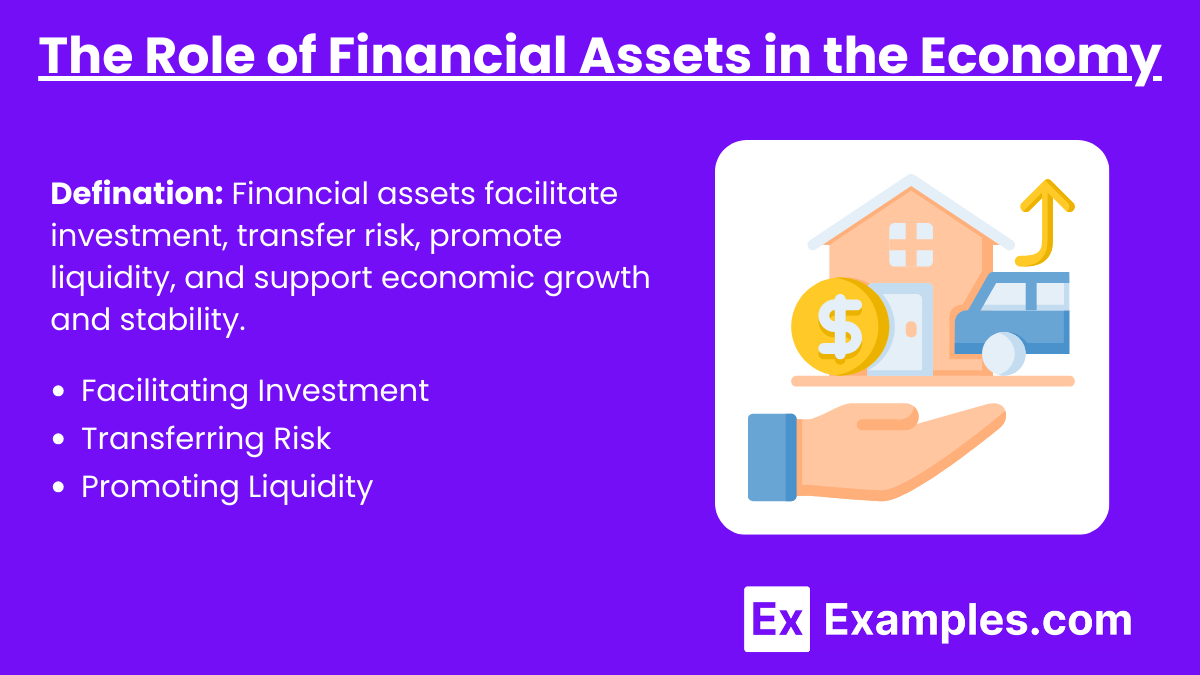

The Role of Financial Assets in the Economy

1. Facilitating Investment

- Financial assets allow savers to lend money to businesses or governments. In return, savers receive interest (on bonds) or dividends (on stocks), while businesses use the funds to invest in capital (like machinery or infrastructure). This stimulates economic growth.

2. Transferring Risk

- Some financial assets, such as derivatives, help manage and transfer risk. Derivatives are contracts based on the value of underlying assets (like stocks or bonds). Investors use them to hedge against price fluctuations, ensuring stability in uncertain economic times.

3. Promoting Liquidity

- Financial markets make it easier to buy and sell assets. Highly liquid assets, such as stocks and bonds, can be easily converted to cash, allowing investors to quickly respond to market changes or opportunities.

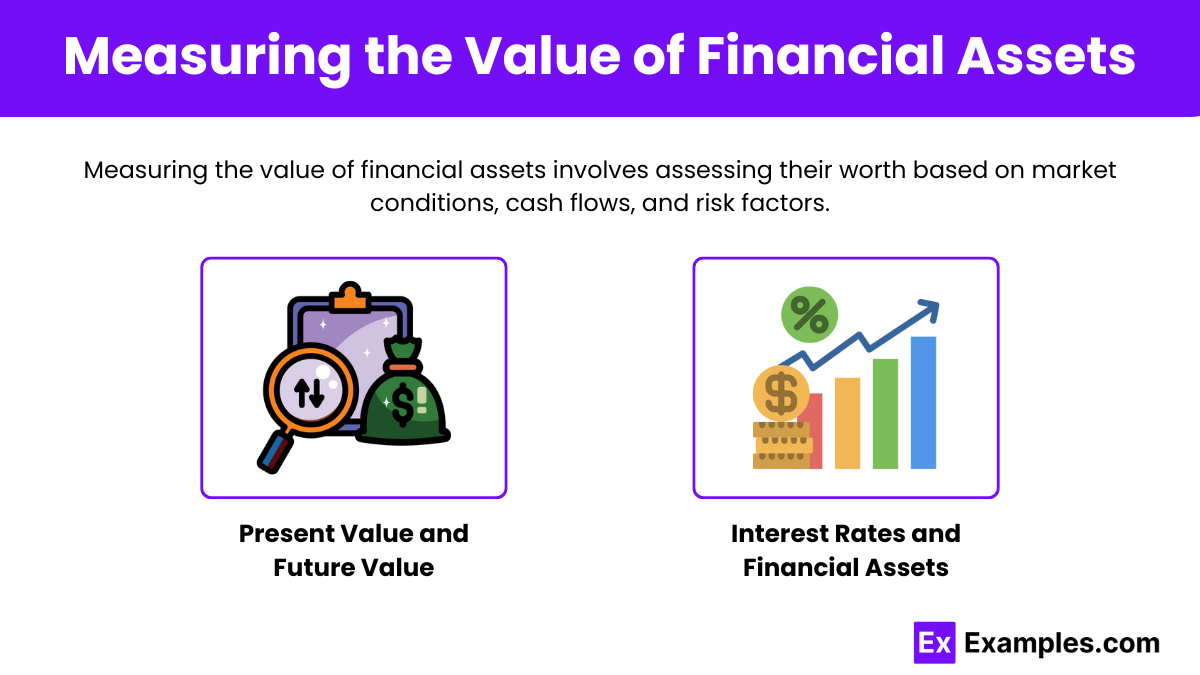

Measuring the Value of Financial Assets

1. Present Value and Future Value

- Present value (PV): The current worth of a financial asset based on future cash flows, discounted at a certain interest rate.

- Future value (FV): The value of an investment after a specified period, considering compound interest. Formula for Future Value:

[

FV = PV \times (1 + r)^t

]

Where: - r = interest rate

- t = number of periods This calculation is essential when comparing different investment options and understanding how interest rates impact the economy.

2. Interest Rates and Financial Assets

- The value of financial assets is sensitive to interest rate changes. When interest rates rise, the present value of future cash flows (like bond payments) falls, making bonds and other fixed-income securities less valuable.

- Monetary policy: Central banks, like the Federal Reserve, influence interest rates to stabilize the economy. Lowering interest rates encourages borrowing and investment, while raising rates aims to reduce inflation by discouraging excessive spending.

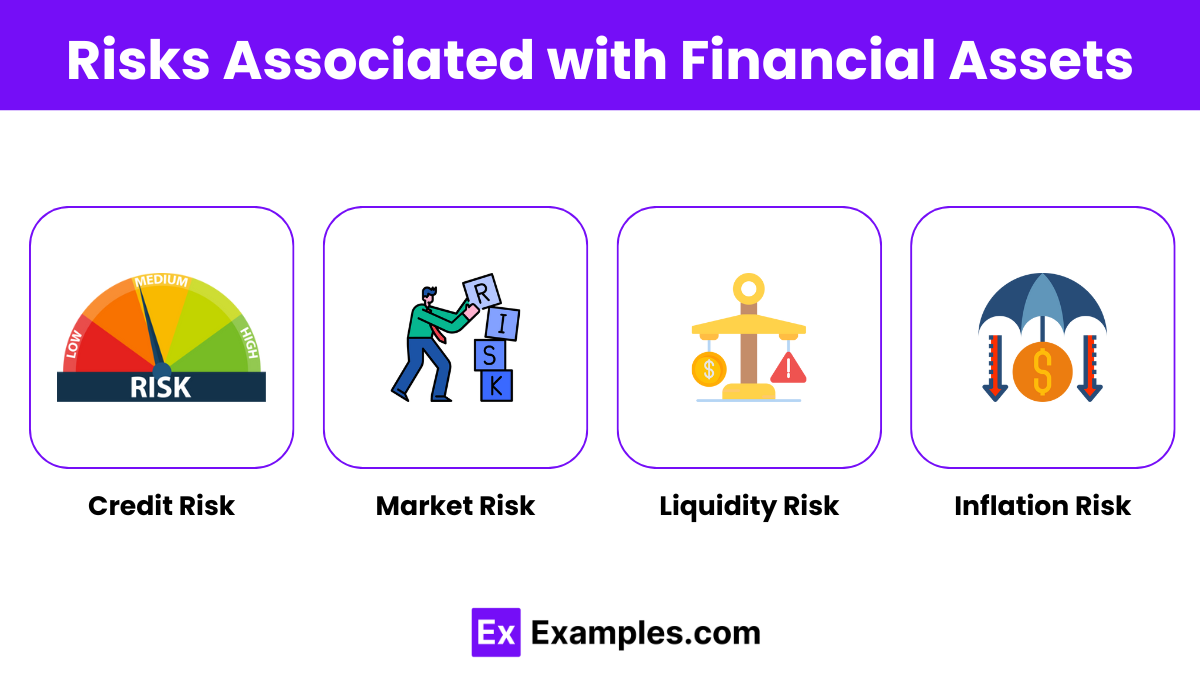

Risks Associated with Financial Assets

1. Credit Risk

- The risk that a borrower will default on their payments. For example, bondholders might not receive interest or principal if the issuing company or government defaults.

2. Market Risk

- The risk that the value of a financial asset will fluctuate due to changes in market conditions. Stock prices, for instance, can be volatile based on investor sentiment, economic conditions, or company performance.

3. Liquidity Risk

- The risk that an asset cannot be sold quickly without incurring a loss. Some financial assets, like real estate or certain bonds, are less liquid than stocks or savings accounts.

4. Inflation Risk

- The risk that inflation will erode the purchasing power of money. This is particularly important for fixed-income assets, like bonds, where future payments may not keep pace with inflation.

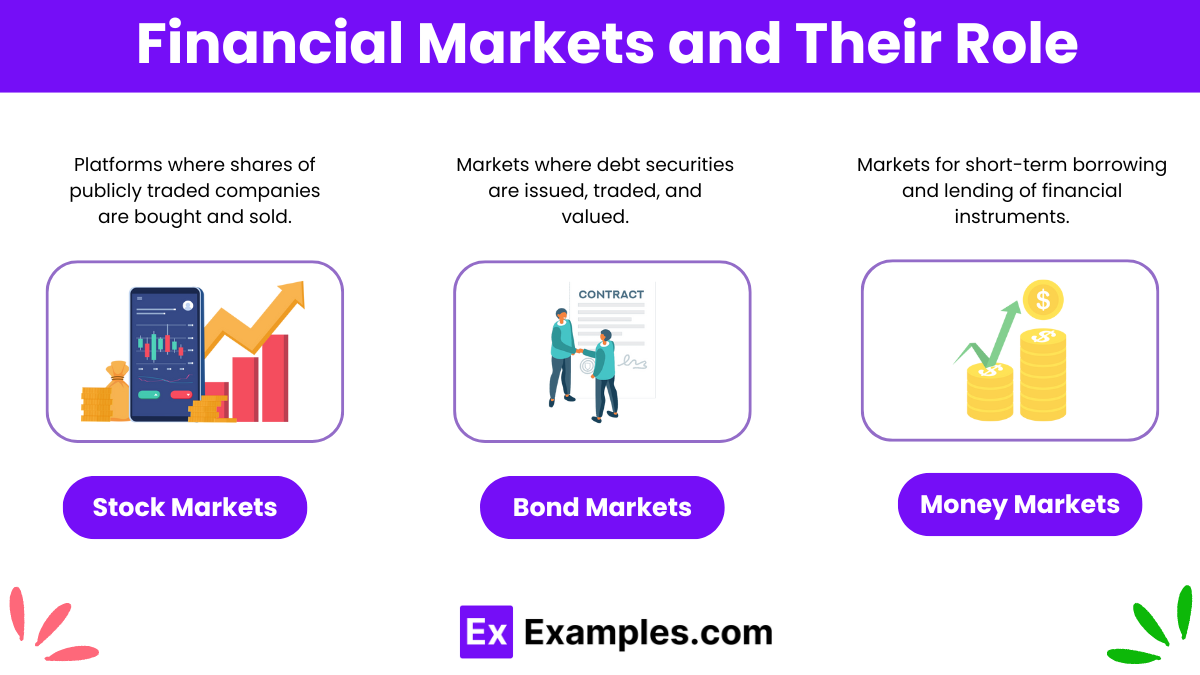

Financial Markets and Their Role

1. Stock Markets

- These are platforms where investors buy and sell stocks. The New York Stock Exchange (NYSE) and Nasdaq are prominent U.S. stock exchanges.

2. Bond Markets

- In the bond market, governments and corporations issue bonds to raise funds, and investors buy these bonds to earn interest over time.

3. Money Markets

- Money markets deal in short-term financial assets like treasury bills and certificates of deposit. They are important for providing liquidity to the financial system.

Example 1: Stocks

Stocks represent ownership in a company, providing shareholders with dividends and potential capital gains based on company performance and market value.

Example 2: Bonds

Bonds are debt securities where investors lend money to issuers, like governments or corporations, in exchange for fixed interest payments until maturity.

Example 3: Mutual Funds

Mutual funds pool money from multiple investors to create a diversified portfolio of stocks, bonds, or other securities, managed by professional fund managers.

Example 4: Certificates of Deposit (CDs)

CDs are time deposits offered by banks with a fixed interest rate and maturity date, providing higher returns than savings accounts but limiting access to funds.

Example 5: Savings Accounts

Savings accounts are low-risk, interest-earning accounts held at financial institutions, offering liquidity but typically with lower interest rates than other financial assets.

MCQs

Question 1

What is a primary characteristic of a bond as a financial asset?

A) It represents ownership in a company

B) It involves lending money to an issuer

C) It offers no interest payments

D) It can only be bought in stock exchanges

Answer: B) It involves lending money to an issuer

Explanation: A bond is a debt security where the investor lends money to an issuer, like a government or corporation, in exchange for interest payments.

Question 2

Which financial asset offers ownership rights in a company?

A) Mutual funds

B) Certificates of deposit

C) Stocks

D) Bonds

Answer: C) Stocks

Explanation: Stocks provide shareholders with ownership in a company, allowing them to receive dividends and have voting rights in certain corporate decisions.

Question 3

Which of the following financial assets is known for providing higher interest rates but limited access to funds?

A) Savings accounts

B) Stocks

C) Mutual funds

D) Certificates of deposit (CDs)

Answer: D) Certificates of deposit (CDs)

Explanation: CDs offer higher interest rates than regular savings accounts but restrict access to funds until a fixed maturity date.