Supply and Demand

Supply and demand are the foundational principles of economics, determining the price and quantity of goods in a market. In AP Macroeconomics, understanding how these forces interact helps explain market equilibrium, price fluctuations, and the impact of external factors like government policies. Mastering supply and demand is crucial for analyzing broader economic systems and behaviors.

Learning Objectives

Understand the laws of supply and demand, how they interact to determine market equilibrium, and the impact of shifts in supply and demand on price and quantity. Master the concepts of elasticity, government interventions (price ceilings, floors, taxes), and graphical analysis.

Demand

Demand refers to the quantity of a good or service that consumers are willing and able to purchase at various price levels during a specific time period.

Law of Demand

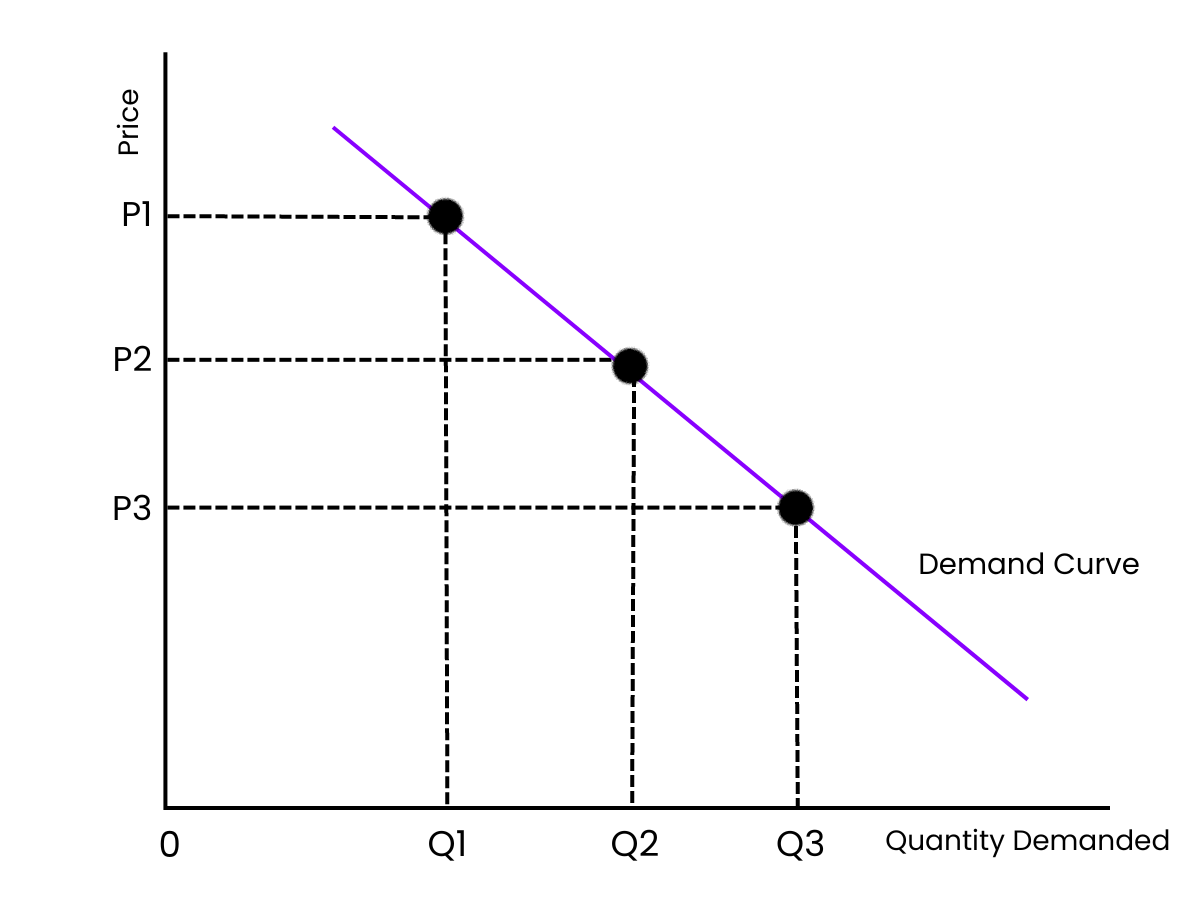

The Law of Demand states that, all else being equal, when the price of a good decreases, the quantity demanded increases, and when the price increases, the quantity demanded decreases. This inverse relationship is due to two main effects:

- Substitution Effect: As the price of a good rises, consumers may switch to cheaper substitutes.

- Income Effect: As the price of a good falls, consumers’ real income increases, allowing them to purchase more of the good.

Determinants of Demand (Non-Price Factors)

These are factors that shift the demand curve to the right (increase in demand) or to the left (decrease in demand):

- Income: As consumers’ income increases, demand for normal goods increases.

- Preferences: Changes in consumer preferences can increase or decrease demand.

- Prices of Related Goods:

- Substitutes: An increase in the price of a substitute good increases demand for the good.

- Complements: An increase in the price of a complement reduces demand.

- Expectations of Future Prices: If consumers expect prices to rise in the future, they may demand more now.

- Number of Buyers: An increase in the number of buyers leads to an increase in demand.

Demand Curve

The demand curve is downward sloping, reflecting the inverse relationship between price and quantity demanded. It shifts based on changes in the determinants of demand.

Supply

Supply refers to the quantity of a good or service that producers are willing and able to offer for sale at various price levels over a specific period.

Law of Supply

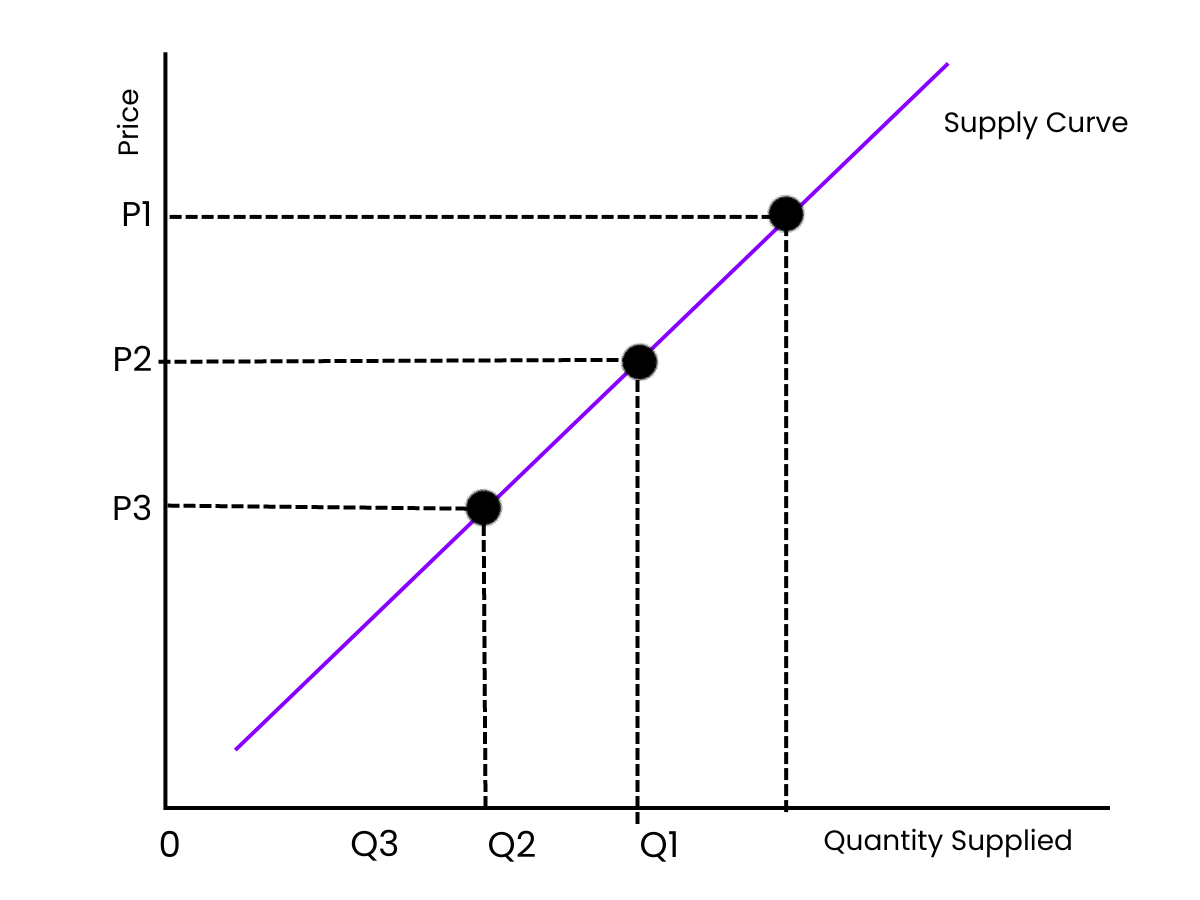

The Law of Supply states that, all else being equal, an increase in the price of a good leads to an increase in the quantity supplied, and a decrease in price leads to a decrease in quantity supplied. This direct relationship occurs because higher prices incentivize producers to supply more goods.

Determinants of Supply (Non-Price Factors)

These factors shift the supply curve to the right (increase in supply) or to the left (decrease in supply):

- Input Prices: An increase in the cost of inputs decreases supply.

- Technology: Technological advancements can lower production costs and increase supply.

- Prices of Related Goods in Production: If the price of a substitute good in production increases, producers may shift production toward that good, decreasing the supply of the other.

- Expectations of Future Prices: If producers expect higher prices in the future, they may reduce current supply.

- Number of Sellers: More sellers in the market increase supply.

- Taxes and Subsidies: Taxes increase production costs and decrease supply, while subsidies decrease costs and increase supply.

Supply Curve

The supply curve is upward sloping, reflecting the direct relationship between price and quantity supplied. It shifts based on changes in the determinants of supply.

Market Equilibrium

Market equilibrium occurs where the quantity demanded equals the quantity supplied at a specific price level. This is called the equilibrium price or market-clearing price.

- Surplus: Occurs when the quantity supplied exceeds the quantity demanded at a given price, leading to downward pressure on prices.

- Shortage: Occurs when the quantity demanded exceeds the quantity supplied at a given price, leading to upward pressure on prices.

Shifts in Supply and Demand

When either the supply or demand curve shifts, it causes a new equilibrium price and quantity.

- Increase in Demand: Leads to a higher equilibrium price and quantity.

- Decrease in Demand: Leads to a lower equilibrium price and quantity.

- Increase in Supply: Leads to a lower equilibrium price and higher equilibrium quantity.

- Decrease in Supply: Leads to a higher equilibrium price and lower equilibrium quantity.

Simultaneous Shifts

If both the supply and demand curves shift at the same time, the impact on equilibrium price and quantity depends on the relative magnitude of the shifts:

- If demand increases and supply decreases, prices will rise, but the change in quantity depends on the size of each shift.

- If both demand and supply increase, quantity will rise, but the change in price depends on which shift is larger.

Examples

Example 1: Gasoline Prices

When global oil supply decreases due to political instability, gasoline prices rise, reducing consumer demand as people drive less or seek alternative transportation.

Example 2: Seasonal Produce

During summer, the supply of strawberries increases, causing prices to drop. Higher supply leads to greater demand as consumers buy more at lower prices.

Example 3: Housing Market

In cities with high demand and limited housing supply, prices surge. Fewer homes available pushes up prices, reducing affordability and shifting demand to cheaper areas.

Example 4: Concert Tickets

Limited supply of tickets for popular concerts leads to high demand, driving prices up, and some consumers may choose to forgo attending or find secondary options.

Example 5: Smartphone Releases

New smartphone models create high demand, and when supply is limited at launch, prices stay high. As supply increases over time, prices drop, and demand levels out.

MCQs

Question 1

What happens to the equilibrium price and quantity when there is an increase in demand but no change in supply?

A) Price increases, quantity decreases

B) Price decreases, quantity increases

C) Price increases, quantity increases

D) Price decreases, quantity decreases

Answer: C) Price increases, quantity increases

Explanation: An increase in demand shifts the demand curve to the right, leading to a higher equilibrium price and quantity as more consumers are willing to buy the good at higher prices.

Question 2

If a government sets a price floor above the equilibrium price, what is the most likely outcome?

A) Shortage

B) Surplus

C) Equilibrium

D) No effect

Answer: B) Surplus

Explanation: A price floor set above the equilibrium price leads to a surplus because the higher price encourages more production but fewer consumers are willing to buy at that price.

Question 3

Which of the following is an example of a complementary good in the context of supply and demand?

A) Coffee and tea

B) Bread and butter

C) Pencils and pens

D) Soda and water

Answer: B) Bread and butter

Explanation: Complementary goods are typically used together, so an increase in the price of bread could lead to a decrease in the demand for butter, illustrating the relationship between related goods.