Short- and Long-run Production Costs

In AP Microeconomics, understanding Short- and Long-run Production Costs is essential for analyzing how firms operate and make decisions. In the short run, at least one input, such as capital, remains fixed, leading to the presence of fixed and variable costs. Conversely, the long run allows all inputs to be varied, enabling firms to achieve optimal production efficiency through economies or diseconomies of scale. Mastering these concepts helps explain cost behaviors, pricing strategies, and the scalability of businesses within different time frames.

Free AP Microeconomics Practice Test

Learning Objectives

When studying Short- and Long-Run Production Costs for AP Microeconomics, you should understand the distinctions between fixed and variable costs in the short run and how all costs become variable in the long run. Learn to analyze and graph short-run and long-run cost curves, including average and marginal costs. Grasp the concepts of economies and diseconomies of scale, and how they affect a firm’s production decisions and cost structures. Additionally, recognize the relationships between different cost measures and how firms achieve cost minimization and optimal production levels over different time horizons.

1. Introduction to Production Costs

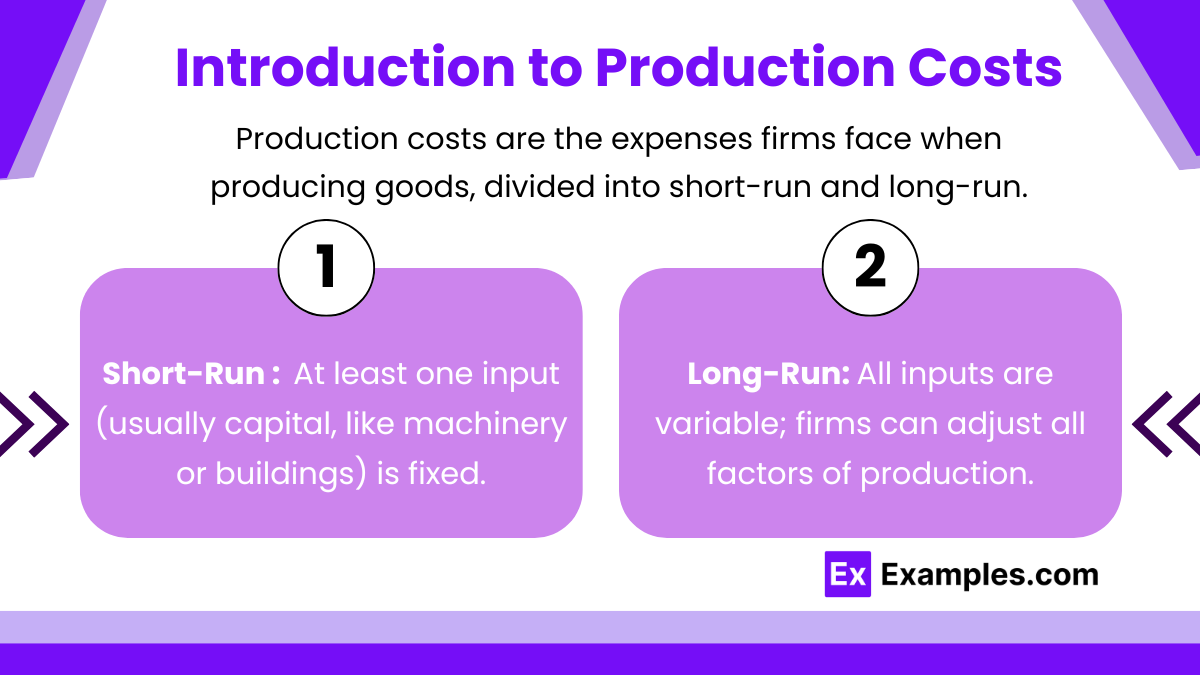

Production Costs refer to the expenses a firm incurs to produce goods or services. They are typically divided into short-run and long-run costs based on the flexibility of adjusting input factors.

Short-Run: At least one input (usually capital, like machinery or buildings) is fixed.

Long-Run: All inputs are variable; firms can adjust all factors of production.

2. Short-Run Production Costs

In the short run, firms face both fixed costs and variable costs due to some inputs being fixed.

A. Fixed Costs (FC)

Definition: Costs that do not change with the level of output. They must be paid even if output is zero.

Examples: Rent, salaries of permanent staff, insurance, depreciation of capital.

B. Variable Costs (VC)

Definition: Costs that vary directly with the level of output.

Examples: Raw materials, wages of hourly workers, utilities for production.

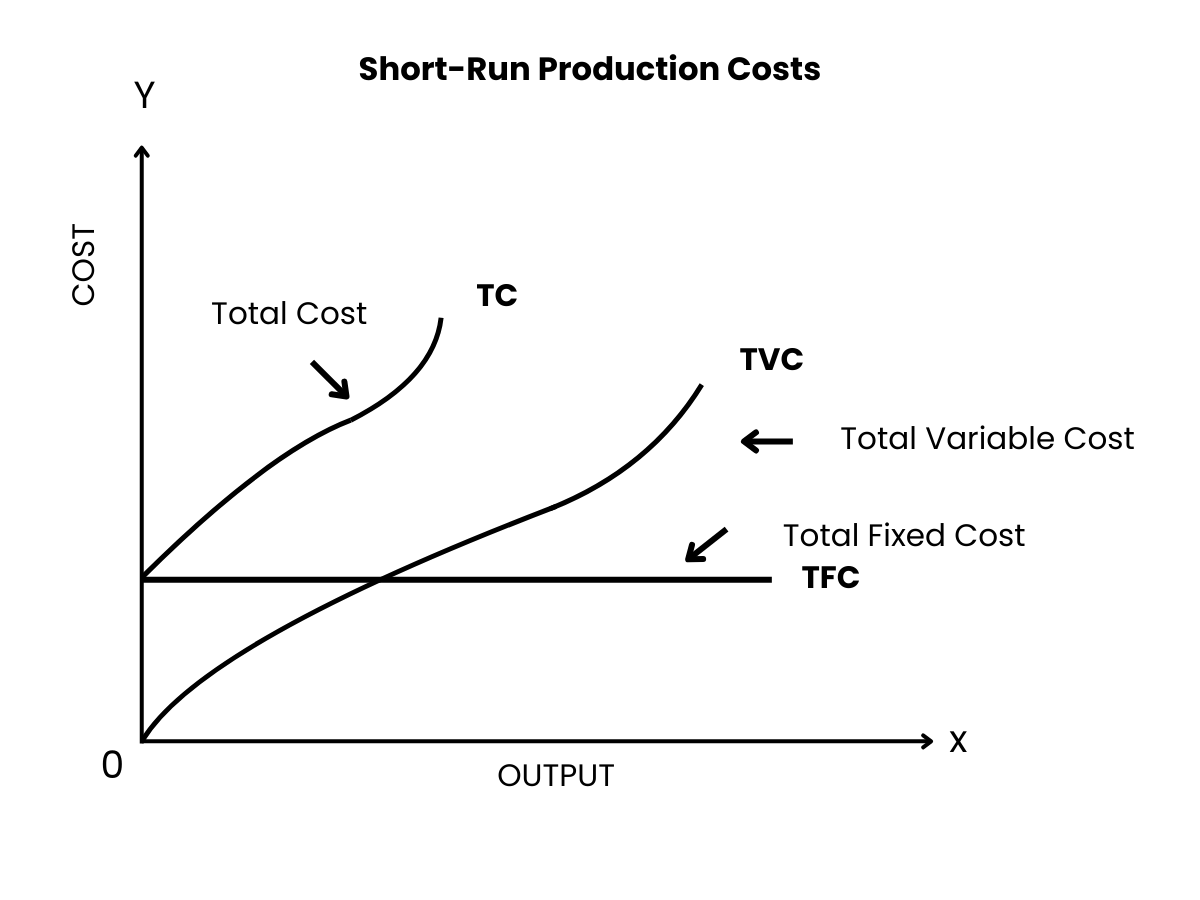

C. Total Costs (TC) :

TC = FC+VC

Total Fixed Costs (TFC): Sum of all fixed costs.

Total Variable Costs (TVC): Sum of all variable costs.

Total Costs (TC): Combined total of TFC and TVC.

D. Average Costs

Average Fixed Cost (AFC):

Average Variable Cost (AVC):

Average Total Cost (ATC):

E. Marginal Cost (MC)

Definition: The additional cost of producing one more unit of output.

Behavior: Typically U-shaped due to diminishing marginal returns; initially decreases, then increases as production scales up.

3. Long-Run Production Costs

In the long run, all inputs are variable, allowing firms to adjust all factors of production to achieve optimal efficiency.

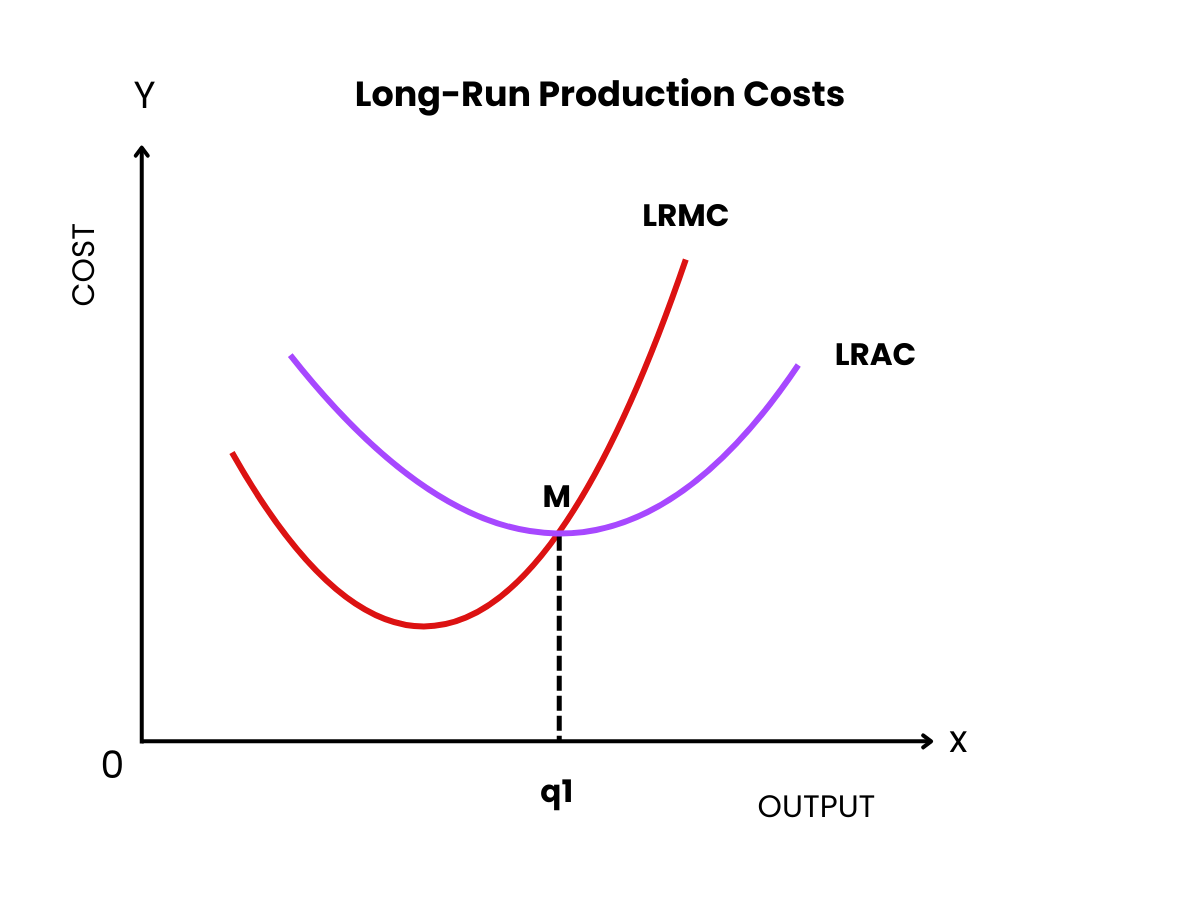

A. Long-Run Average Cost (LRAC)

Definition: The lowest possible average cost of production, allowing all inputs to be varied.

Shape: Typically U-shaped due to economies and diseconomies of scale.

B. Economies of Scale

Definition: Cost advantages that firms obtain due to expansion.

Causes:

Technical economies: More efficient production techniques.

Managerial economies: Better management as firms grow.

Financial economies: Access to cheaper financing.

Marketing economies: Spreading marketing costs over more units.

Purchasing economies: Buying inputs in bulk at discounts.

Effect: Decrease in LRAC as output increases.

C. Diseconomies of Scale

Definition: Cost disadvantages that firms face as they grow too large.

Causes:

Coordination problems: Difficulty in managing a large workforce.

Communication issues: Slower information flow.

Bureaucracy: Increased administrative costs.

Effect: Increase in LRAC as output continues to rise beyond an optimal point.

D. Constant Returns to Scale

Definition: When increasing all inputs by a certain factor leads to an increase in output by the same factor.

Effect: LRAC remains constant as output increases.

4. E. Long-Run Cost Curves vs. Short-Run Cost Curves

LRAC Curve: Encompasses all possible short-run ATC curves. Represents the envelope of short-run average total cost curves for different levels of fixed inputs.

Shape: Smoother U-shape compared to short-run ATC due to the flexibility in choosing optimal plant sizes.

Diagram:Figure 2: Long-Run Average Cost Curve and Short-Run ATC Curves

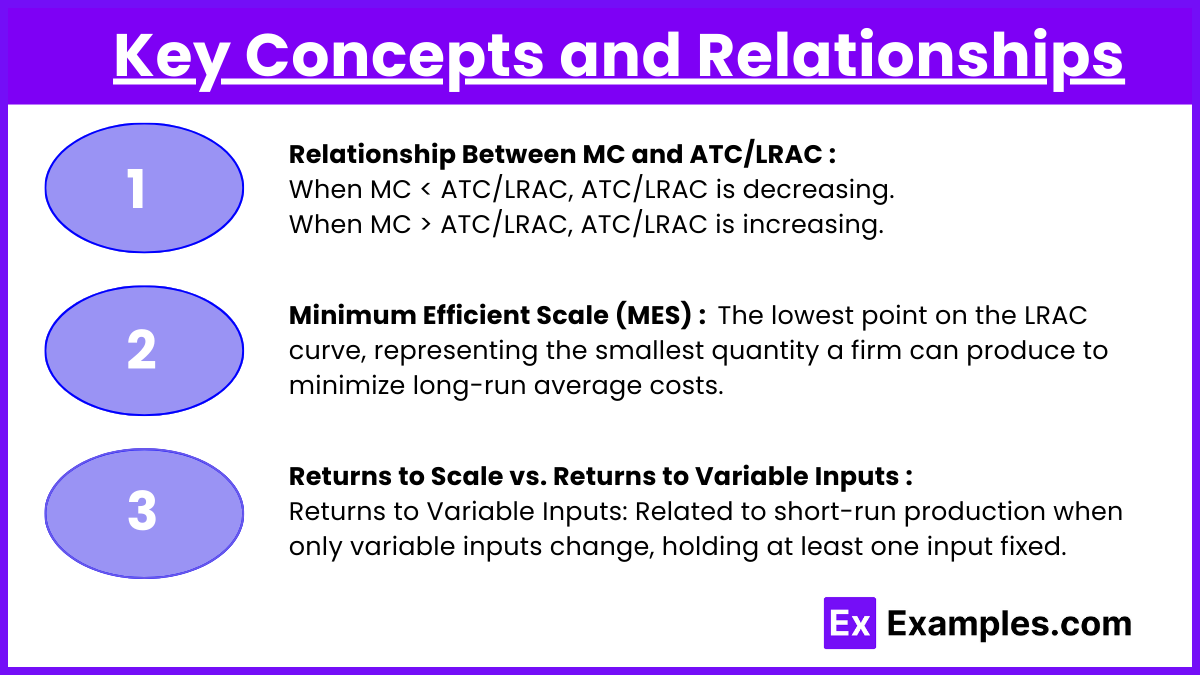

5. Key Concepts and Relationships

A. Relationship Between MC and ATC/LRAC

MC intersects ATC and LRAC at their minimum points:

When MC < ATC/LRAC, ATC/LRAC is decreasing.

When MC > ATC/LRAC, ATC/LRAC is increasing.

B. Minimum Efficient Scale (MES)

Definition: The lowest point on the LRAC curve, representing the smallest quantity a firm can produce to minimize long-run average costs.

Significance: Determines the size at which a firm achieves economies of scale.

C. Returns to Scale vs. Returns to Variable Inputs

Returns to Scale: Related to long-run production changes when all inputs are varied.

Returns to Variable Inputs: Related to short-run production when only variable inputs change, holding at least one input fixed.

Examples

Example 1. Automobile Manufacturing Company

Short-Run Production Costs:

In the short run, an automobile manufacturer has several fixed and variable costs. Fixed costs include expenses like the cost of machinery, factory buildings, and salaried employees. These costs remain constant regardless of the number of cars produced. Variable costs encompass materials such as steel, rubber, and electronics, as well as wages for hourly workers involved in assembly. If demand increases, the company can ramp up production by utilizing more labor and materials without altering its fixed capital.

Long-Run Production Costs:

In the long run, the manufacturer can adjust all inputs, including capital. If the company anticipates sustained high demand, it might invest in additional factories or more advanced machinery to increase production capacity. This investment could lead to economies of scale, reducing the average cost per vehicle as production volume increases. Conversely, if the company becomes too large, it might face diseconomies of scale due to increased complexity in management and coordination, potentially raising average costs.

Example 2. Fast-Food Restaurant Chain

Short-Run Production Costs:

For a fast-food restaurant, fixed costs include rent for the restaurant space, salaries for managerial staff, and equipment like ovens and fryers. These costs must be paid regardless of how many meals are served. Variable costs include ingredients, hourly wages for kitchen and service staff, and utility bills that fluctuate with the level of operations. During peak hours, the restaurant can increase output by hiring more staff or extending operating hours without altering its fixed infrastructure.

Long-Run Production Costs:

In the long run, the restaurant can modify all inputs to optimize costs. For example, it might expand to additional locations or redesign the kitchen layout for greater efficiency. Investing in automated cooking equipment could reduce labor costs and increase consistency, leading to lower average costs through technical economies. Alternatively, if the restaurant chain grows too rapidly, it might encounter diseconomies of scale such as challenges in maintaining quality and brand consistency across all locations, thereby increasing long-run average costs.

Example 3. Software Development Company

Short-Run Production Costs:

A software company faces fixed costs like office leases, salaries for permanent staff (e.g., developers and administrators), and costs for essential software licenses and hardware. Variable costs might include expenses for freelance developers, cloud computing services that scale with usage, and marketing campaigns that vary based on the product launch cycle. In the short run, the company can adjust variable costs to meet project demands without changing its fixed capital investments.

Long-Run Production Costs:

Over the long term, the company can scale its operations by investing in additional office space, hiring more full-time employees, or developing proprietary software tools to enhance productivity. These adjustments can lead to economies of scale by spreading fixed costs over a larger output and improving efficiencies through specialized roles. However, if the company becomes too large, it may suffer from diseconomies of scale such as increased bureaucracy and slower decision-making processes, which can raise the long-run average costs.

Example 4. Agricultural Farm

Short-Run Production Costs:

An agricultural farm incurs fixed costs like land leases, machinery (tractors, harvesters), and permanent labor contracts. Variable costs include seeds, fertilizers, pesticides, and wages for seasonal workers. In the short run, the farm can increase production by hiring more seasonal labor or purchasing additional inputs without changing its land or machinery.

Long-Run Production Costs:

In the long run, the farm can expand its land holdings, invest in more advanced machinery, or adopt new farming technologies such as irrigation systems or genetically modified crops. These changes can lead to economies of scale by increasing output efficiency and reducing the average cost per unit of produce. However, expanding too much might result in diseconomies of scale due to factors like overuse of resources, environmental degradation, or increased management complexity, which can elevate long-run average costs.

Example 5. Retail Clothing Store

Short-Run Production Costs:

A retail clothing store has fixed costs such as rent for the storefront, salaries for permanent staff, and expenses for store fixtures and fittings. Variable costs include inventory purchases, utilities that vary with store hours, and wages for part-time or seasonal employees. In the short run, the store can manage inventory levels and staffing to respond to seasonal demand without altering its fixed assets.

Long-Run Production Costs:

In the long run, the store can expand by opening additional locations, investing in online sales platforms, or diversifying its product lines. These adjustments can lead to economies of scale by allowing bulk purchasing of inventory, spreading marketing costs across multiple locations, and leveraging a broader customer base to reduce average costs. However, managing multiple locations may introduce diseconomies of scale such as higher administrative costs, challenges in maintaining consistent service quality, and increased logistical complexities, which can raise the long-run average costs.

Multiple Choice Questions

Question 1

Which of the following statements best describes the relationship between marginal cost (MC) and average total cost (ATC) in the short run?

A) MC is always above ATC.

B) MC intersects ATC at the ATC’s minimum point.

C) MC and ATC move in the same direction at all levels of output.

D) MC is always below ATC.

Answer: B) MC intersects ATC at the ATC’s minimum point.

Explanation:

Marginal Cost (MC) is the additional cost of producing one more unit of output.

Average Total Cost (ATC) is the total cost per unit of output.

Why Other Options Are Incorrect:

A) MC is always above ATC.

Incorrect. MC can be both above and below ATC depending on the output level.C) MC and ATC move in the same direction at all levels of output.

Incorrect. MC can cross ATC, causing them to move in different directions.D) MC is always below ATC.

Incorrect. Similar to option A, MC can be both above and below ATC.

Question 2

A firm experiences decreasing average costs as it increases production. This situation is an example of:

A) Diseconomies of scale

B) Constant returns to scale

C) Economies of scale

D) Increasing marginal costs

Answer: C) Economies of scale

Explanation:

Economies of Scale occur when a firm’s average costs decrease as production increases. This can happen due to factors like bulk purchasing, specialized labor, and more efficient use of resources.

Key Points:

Decreasing Average Costs: As output rises, the cost per unit falls.

Causes: Technical efficiencies, managerial expertise, bulk discounts, etc.

Why Other Options Are Incorrect:

A) Diseconomies of scale

Incorrect. Diseconomies of scale occur when average costs increase as production increases.B) Constant returns to scale

Incorrect. Constant returns to scale mean that average costs remain unchanged as production increases.D) Increasing marginal costs

Incorrect. While marginal costs may be increasing, the specific situation described is about decreasing average costs, which is best explained by economies of scale.

Question 3

In the long run, a firm can adjust all inputs and choose the optimal plant size. Which of the following is not a characteristic of long-run production costs?

A) All costs are variable.

B) Firms face fixed costs.

C) Firms can achieve economies of scale.

D) The long-run average cost curve is the envelope of short-run average cost curves.

Answer: B) Firms face fixed costs.

Explanation:

In the long run, all inputs are variable, meaning there are no fixed costs. Firms have the flexibility to adjust all factors of production, including plant size, which allows them to optimize costs fully.

Why Other Options Are Incorrect:

A) All costs are variable.

Correct characteristic of long-run costs.C) Firms can achieve economies of scale.

Correct, as firms can optimize input combinations and production scales.D) The long-run average cost curve is the envelope of short-run average cost curves.

Correct, as the LRAC represents the minimum cost for each output level by enveloping all SRAC curves.