The growth of the global economy

The growth of the global economy refers to the expansion and integration of trade, finance, and technology across continents. Beginning with European exploration and colonization, it evolved through industrialization, imperialism, and modern globalization. This process reshaped societies, economies, and politics, creating interconnected markets, fostering cultural exchanges, and influencing global power dynamics, while also posing challenges like inequality.

Free AP World History: Modern Practice Test

Learning Objective

In studying "The Growth of the Global Economy" for AP World History: Modern, you should learn to identify the major factors contributing to global economic expansion, including technological advancements, industrialization, and trade networks. Analyze the rise of multinational corporations, global finance systems, and labor migrations, and evaluate how economic globalization influenced social structures, political relationships, and disparities between nations.

1. Early Modern Global Trade Networks (1450–1750)

European Exploration: In the 15th and 16th centuries, European explorers like Vasco da Gama and Christopher Columbus sought direct routes to Asia, leading to the discovery of the Americas and the establishment of global trade networks.

Columbian Exchange: This exchange involved the transfer of plants, animals, diseases, and people between the Americas, Africa, and Eurasia. It greatly impacted agricultural production, population growth, and cultural exchanges worldwide.

Triangular Trade: The system connected Europe, Africa, and the Americas. Manufactured goods from Europe were traded for enslaved Africans, who were sent to the Americas to work on plantations, producing cash crops like sugar and tobacco for European markets.

2. Industrial Revolution and Economic Expansion (1750–1900)

Technological Advances: The Industrial Revolution began in Britain and spread to other parts of Europe and the United States, transforming production processes. Innovations like the steam engine and mechanized textile manufacturing increased productivity.

Rise of Capitalism: Adam Smith's ideas on free markets and capitalism, as outlined in "The Wealth of Nations," fueled economic growth. The shift from agrarian economies to industrialized, market-based economies marked a turning point in global economic structures.

Global Trade and Imperialism: Industrialized nations sought raw materials and new markets, leading to imperial expansion in Africa and Asia. This increased global trade and established a system of economic dependence, with colonies providing resources to European powers.

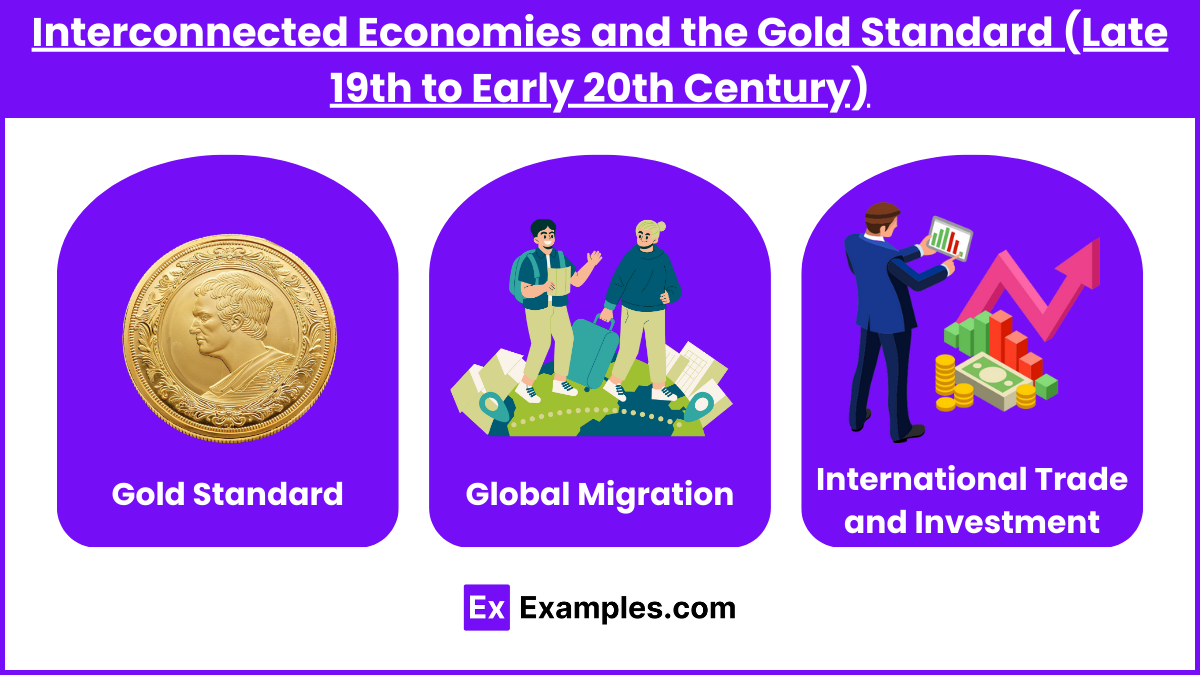

3. Interconnected Economies and the Gold Standard (Late 19th to Early 20th Century)

Gold Standard: Most major economies adopted the gold standard, linking their currencies to gold. This system facilitated international trade by providing a stable exchange rate but also made economies vulnerable to global financial fluctuations.

Global Migration: The growth of the global economy was accompanied by mass migrations. Workers from China, India, and Europe moved to different parts of the world, such as the Americas, Africa, and Southeast Asia, seeking economic opportunities or forced into labor.

International Trade and Investment: As transportation improved, trade became more efficient, and international investments increased. European banks and companies invested heavily in railroads, mining, and agriculture in Latin America, Africa, and Asia.

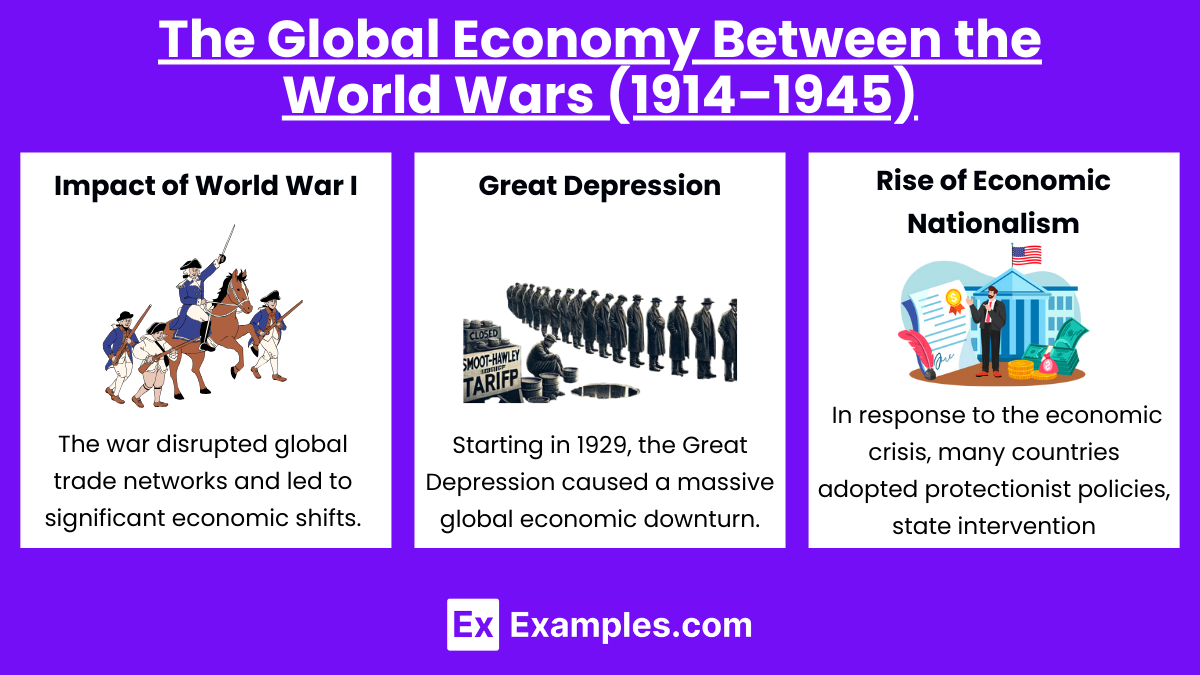

4. The Global Economy Between the World Wars (1914–1945)

Impact of World War I: The war disrupted global trade networks and led to significant economic shifts, with the United States emerging as a leading creditor nation. European countries faced debt and economic instability.

Great Depression: Starting in 1929, the Great Depression caused a massive global economic downturn. Protectionist policies like the Smoot-Hawley Tariff worsened the crisis by reducing international trade.

Rise of Economic Nationalism: In response to the economic crisis, many countries adopted protectionist policies, state intervention, and government-planned economies, leading to a decline in global trade and investment.

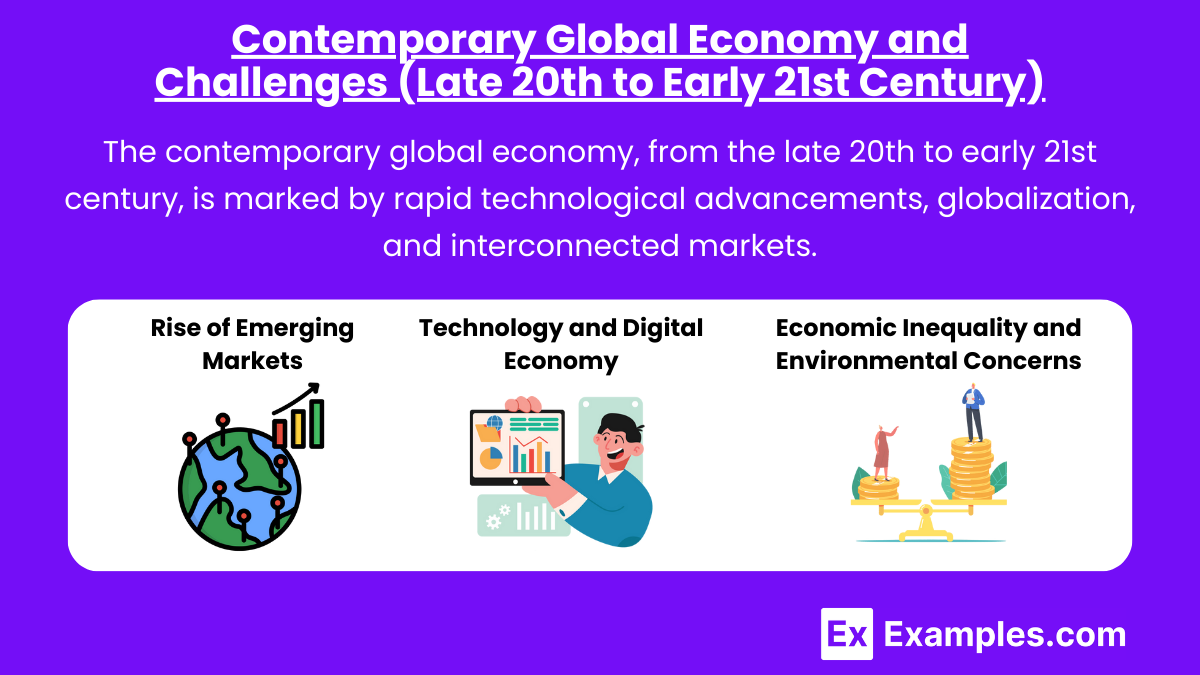

5. Contemporary Global Economy and Challenges (Late 20th to Early 21st Century)

The contemporary global economy, from the late 20th to early 21st century, is marked by rapid technological advancements, globalization, and interconnected markets. Challenges include income inequality, climate change, geopolitical tensions, and economic instability. The rise of digital economies and shifts in trade patterns also shape this complex and evolving landscape.

Rise of Emerging Markets: Countries like China, India, and Brazil have emerged as major economic players, contributing to the growth of the global economy. China's entry into the WTO in 2001 accelerated its integration into the global market.

Technology and Digital Economy: The internet and digital technologies revolutionized communication, trade, and finance. E-commerce giants like Amazon and Alibaba transformed retail, while financial technologies enabled faster cross-border transactions.

Economic Inequality and Environmental Concerns: Globalization has contributed to economic growth but also led to widening wealth disparities. Environmental issues, such as climate change and resource depletion, pose significant challenges to sustainable economic growth.

Examples

Example 1: The Columbian Exchange

This transatlantic trade between the Americas, Europe, and Africa exchanged goods, plants, animals, and diseases, significantly boosting global economic interactions and agricultural production.

Example 2: Industrial Revolution

The technological advancements and mass production during the Industrial Revolution accelerated manufacturing, increased trade, and connected economies worldwide, fueling rapid economic growth and urbanization.

Example 3: The Gold Standard

Linking currencies to gold in the 19th century stabilized international trade, enabling predictable exchange rates and expanding cross-border investments, fostering global economic integration.

Example 4: Bretton Woods System

Post-World War II, this system established the IMF and World Bank, promoting global financial stability and encouraging international trade, investment, and reconstruction.

Example 5: China's Entry into the WTO

China's 2001 entry into the World Trade Organization expanded its global trade participation, leading to rapid economic growth, increased exports, and global market integration.

MCQs

Question 1

Which event significantly contributed to the expansion of global trade networks during the 15th and 16th centuries?

A) The Industrial Revolution

B) The Columbian Exchange

C) The Bretton Woods Conference

D) The Great Depression

Answer: B) The Columbian Exchange

Explanation: The Columbian Exchange facilitated the transfer of goods, crops, and animals between the Americas, Europe, and Africa, greatly expanding global trade networks.

Question 2

How did the Industrial Revolution impact the growth of the global economy?

A) By reducing the need for raw materials

B) By decreasing global trade

C) By accelerating mass production and trade

D) By ending colonial expansion

Answer: C) By accelerating mass production and trade

Explanation: The Industrial Revolution introduced technological advancements, which boosted manufacturing, increased production, and promoted trade, significantly contributing to global economic growth and interconnectedness.

Question 3

Why was the Bretton Woods System important in shaping the post-World War II global economy?

A) It ended international trade

B) It established the Gold Standard

C) It created institutions like the IMF and World Bank

D) It isolated economies

Answer: C) It created institutions like the IMF and World Bank

Explanation: The Bretton Woods System established the IMF and World Bank, promoting financial stability and fostering international trade and investment, shaping the modern global economy.