4 General Ledger Examples

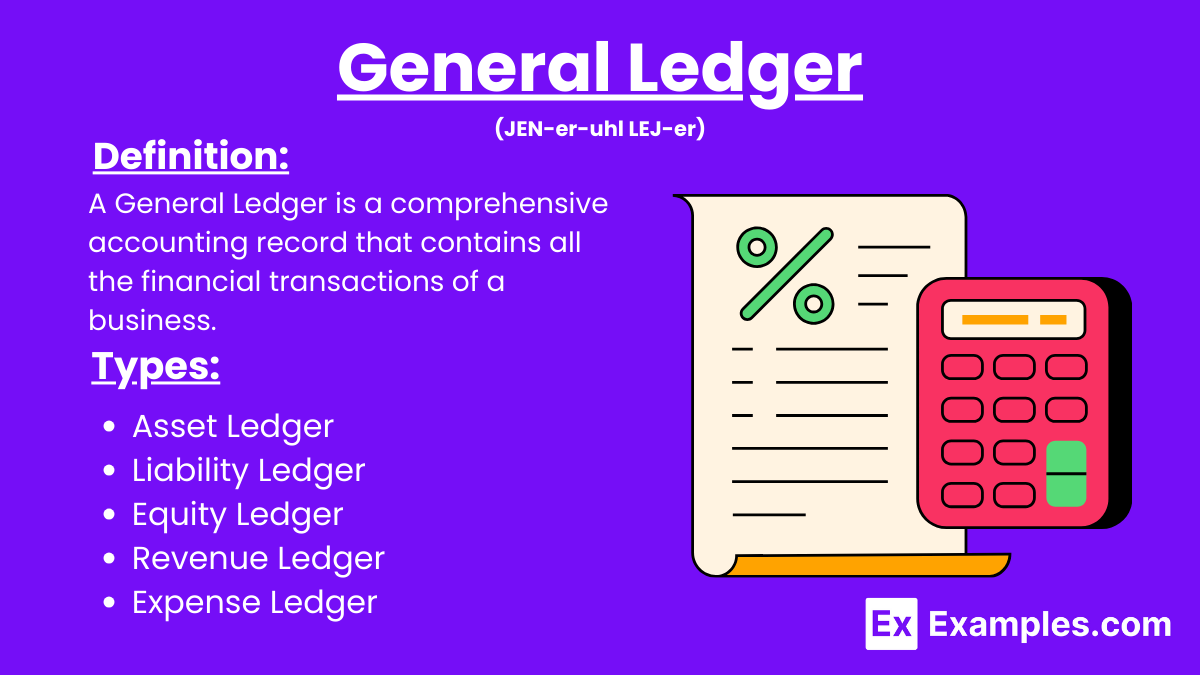

A general ledger is a comprehensive accounting record that contains all the financial transactions of a business. It serves as the central repository for all accounting data, summarizing the financial activities of the company over a specific period. The general ledger is a key component of the double-entry bookkeeping system and provides the basis for creating financial statements. It includes various specific ledgers such as a rental ledger for tracking rental income and expenses, project costing for monitoring the costs associated with specific projects, and sales invoices for recording revenue from sales transactions.

What is General Ledger?

Examples of General Ledger

- Cash

- Accounts Receivable

- Inventory

- Prepaid Expenses

- Equipment

- Accumulated Depreciation

- Accounts Payable

- Salaries Payable

- Unearned Revenue

- Common Stock

- Retained Earnings

- Sales Revenue

- Cost of Goods Sold

- Advertising Expense

- Interest Expense

Types of General Ledger

1. Asset Ledger

- Description: Records all assets owned by the company.

- Examples: Cash, Accounts Receivable, Inventory, Property, and Equipment.

2. Liability Ledger

- Description: Tracks all obligations and debts owed by the company.

- Examples: Accounts Payable, Loans Payable, Accrued Expenses.

3. Equity Ledger

- Description: Contains accounts related to the owners’ interest in the company.

- Examples: Common Stock, Retained Earnings, Owner’s Capital.

4. Revenue Ledger

- Description: Captures all income generated by the company’s operations.

- Examples: Sales Revenue, Service Revenue, Interest Income.

5. Expense Ledger

- Description: Records all costs incurred in the process of earning revenue.

- Examples: Salaries Expense, Rent Expense, Utilities Expense, Depreciation Expense.

Problem of General Ledger Account

General Ledger Account

A general ledger account is a record within the general ledger that tracks all financial transactions related to a specific aspect of a business. These accounts are fundamental components of the double-entry bookkeeping system, ensuring accurate and balanced financial reporting. Tools like printable financial accounting and auditing resources help maintain and verify these records. In addition, a personal care agreement might be tracked as a specific account in the ledger, ensuring all related expenses and incomes are accounted for. Regularly generating a reconciliation statement ensures that the ledger is accurate and aligns with external records.

Components of a General Ledger Account

- Account Name: Each account has a unique name that identifies its purpose, such as “Cash,” “Accounts Receivable,” or “Sales Revenue.”

- Account Number: Accounts are often assigned a number for easier reference and organization.

- Debits and Credits: Transactions are recorded as debits and credits, impacting the account’s balance. Debits typically increase asset or expense accounts, while credits increase liability, equity, or revenue accounts.

- Running Balance: Each account maintains a running balance, reflecting the cumulative effect of all transactions over time.

Controlling Accounts vs. Subsidiary ledger

| Aspect | Controlling Accounts | Subsidiary Ledger |

|---|---|---|

| Definition | A summary account in the general ledger that consolidates the total balances of related subsidiary accounts. | A detailed ledger that provides individual transaction records for each specific account under the controlling account. |

| Purpose | To provide a summarized view of multiple related transactions in the general ledger. | To offer detailed information and tracking for each individual account within the controlling account. |

| Location | Located in the general ledger. | Maintained separately but linked to the controlling account in the general ledger. |

| Examples | Accounts Receivable, Accounts Payable | Individual customer accounts (Accounts Receivable), individual supplier accounts (Accounts Payable) |

| Balance Representation | Shows the total balance of all related subsidiary accounts combined. | Displays the detailed transactions and balances for each specific account. |

| Transaction Details | Does not show individual transaction details, only the total. | Provides detailed transaction history and balances for each account. |

| Reconciliation | Used to verify that the total balances of subsidiary ledgers match the controlling account balance. | Helps in tracking and verifying individual transactions that make up the total balance in the controlling account. |

| Use in Financial Reporting | Used in the preparation of financial statements to provide aggregate figures. | Not directly used in financial reporting but essential for internal tracking and reconciliation. |

| Example Transactions | The total amount owed by all customers combined. | The specific amounts owed by each individual customer. |

General Ledgers and Double-Entry Bookkeeping

The general ledger and double-entry bookkeeping are interdependent:

- Recording Transactions: Double-entry bookkeeping ensures each transaction is recorded twice, once as a debit and once as a credit, in the general ledger.

- Account Maintenance: The general ledger maintains balances for each account, updated through double-entry bookkeeping.

- Financial Reporting: Accurate double-entry records in the general ledger facilitate reliable financial statements, such as the balance sheet and income statement.

Link to Balance Sheet and Income Statement

The general ledger, balance sheet, and income statement are interconnected elements of a company’s financial reporting system. Here’s how they relate to each other:

General Ledger

The general ledger is the central repository for all financial transactions. It contains detailed records of all the company’s accounts, including assets, liabilities, equity, revenue, and expenses. Each transaction recorded in the general ledger affects at least two accounts through the double-entry bookkeeping system.

Balance Sheet

The balance sheet provides a snapshot of a company’s financial position at a specific point in time. It summarizes the general ledger accounts into three main categories:

- Assets: Resources owned by the company (e.g., cash, inventory, accounts receivable).

- Liabilities: Obligations owed by the company (e.g., accounts payable, loans).

- Equity: Owner’s interest in the company (e.g., common stock, retained earnings).

The balance sheet follows the accounting equation:

Assets=Liabilities+Equity\text{Assets} = \text{Liabilities} + \text{Equity}Assets=Liabilities+Equity

Income Statement

The income statement (also known as the profit and loss statement) shows the company’s financial performance over a specific period. It summarizes revenue and expenses from the general ledger, resulting in net income or loss:

Net Income=Revenue−Expenses\text{Net Income}=\text{Revenue}\text{Expenses}Net Income=Revenue−Expenses

Linkage Process

- From General Ledger to Balance Sheet:

- Assets: Summarize asset accounts from the general ledger.

- Liabilities: Summarize liability accounts from the general ledger.

- Equity: Summarize equity accounts from the general ledger, including retained earnings which are affected by net income from the income statement.

- From General Ledger to Income Statement:

- Revenue: Summarize revenue accounts from the general ledger.

- Expenses: Summarize expense accounts from the general ledger.

- Net Income: Calculate net income (or loss) by subtracting total expenses from total revenue.

- From Income Statement to Balance Sheet:

- The net income calculated in the income statement impacts the retained earnings in the equity section of the balance sheet.

- Retained Earnings: Begin with the previous period’s retained earnings, add net income (or subtract net loss), and subtract any dividends paid.

Decentralized Ledger – Blockchain Technology

Blockchain is a type of decentralized ledger technology (DLT) that securely records transactions across a network of computers. Each transaction is grouped into a block, and these blocks are linked (chained) together in a chronological order, forming a continuous chain of blocks.

Features of Blockchain Technology

- Decentralization: No single central authority controls the blockchain. Instead, it is managed by a distributed network of nodes.

- Transparency: All transactions are visible to participants in the network, ensuring transparency.

- Security: Transactions are secured using cryptographic techniques, making them tamper-proof and immutable.

- Consensus Mechanisms: Transactions are validated through consensus mechanisms such as Proof of Work (PoW) or Proof of Stake (PoS), ensuring agreement among network participants.

Uses of General Ledger

- Centralized Financial Data: The general ledger serves as a centralized repository for all financial transactions. It consolidates data from various sub-ledgers, such as accounts receivable and accounts payable, providing a complete and integrated view of the company’s financial activities.

- Financial Reporting: General ledgers provide the essential data needed to prepare key financial statements, such as the balance sheet, income statement, and cash flow statement. These reports are critical for stakeholders to understand the financial health and performance of the business.

- Budgeting and Forecasting: By analyzing historical data recorded in the general ledger, companies can develop accurate budgets and financial forecasts. This historical financial information helps businesses predict future revenues, expenses, and cash flows, facilitating better financial planning.

- Compliance and Auditing: General ledgers help ensure compliance with accounting standards, regulations, and tax laws. They provide a clear and detailed record of all transactions, which is essential for internal and external audits. Auditors use the general ledger to verify the accuracy and integrity of financial statements.

- Internal Controls: The general ledger supports internal controls by providing a detailed record of transactions. This transparency helps detect and prevent errors, fraud, and financial discrepancies. Regular reconciliation of ledger accounts ensures accuracy and accountability.

- Performance Analysis: Businesses use general ledger data to analyze financial performance and profitability. By examining revenue and expense accounts, companies can identify trends, evaluate the effectiveness of business strategies, and make informed decisions to improve operational efficiency.

- Cost Management: The general ledger tracks all costs associated with business operations. This tracking allows management to monitor expenses, identify cost-saving opportunities, and ensure that resources are used efficiently.

How is a general ledger structured?

A general ledger is structured with accounts for assets, liabilities, equity, revenue, and expenses, each recording individual transactions.

What is double-entry bookkeeping in the general ledger?

Double-entry bookkeeping records each transaction as both a debit and a credit in the general ledger, ensuring balanced accounts.

How does the general ledger relate to the trial balance?

The general ledger’s account balances are used to prepare the trial balance, ensuring all debits equal all credits.

What types of accounts are in a general ledger?

A general ledger includes asset, liability, equity, revenue, and expense accounts.

How often is the general ledger updated?

The general ledger is typically updated regularly, often daily, to ensure accurate and up-to-date financial records.

What is the difference between a general ledger and a subledger?

A subledger details transactions for specific accounts, while the general ledger summarizes all transactions across all accounts.

How does the general ledger support financial statements?

The general ledger’s summarized account balances form the basis for financial statements like the balance sheet and income statement.

What software is commonly used for general ledger management?

Software like QuickBooks, SAP, and Oracle are commonly used to manage general ledger accounts and transactions.

How do you reconcile a general ledger?

You reconcile a general ledger by comparing its accounts with external records, correcting discrepancies to ensure accuracy.

What is a general ledger code?

A general ledger code is a unique identifier for each account in the general ledger, used to categorize transactions.

Share :