Asset Allocation to Alternative Investments

Preparing for the CFA Exam requires a thorough understanding of asset allocation to alternative investments, a key area within portfolio management. Mastery of this topic involves knowing the characteristics, risks, and benefits of alternative assets, including real estate, hedge funds, and private equity. This expertise supports informed decision-making and portfolio diversification strategies essential for achieving high CFA scores.

Learning Objective

In studying “Asset Allocation to Alternative Investments” for the CFA Exam, you should learn to understand the role of alternative investments in a diversified portfolio, including assets such as private equity, hedge funds, real estate, and commodities. Analyze the unique risk-return characteristics of these investments and how they contribute to portfolio risk management and potential returns. Evaluate the principles and strategies involved in allocating assets to alternatives, considering liquidity, correlation with traditional assets, and economic cycles. Additionally, explore how these allocations impact portfolio diversification and performance, and apply your understanding to practical scenarios and case studies relevant to CFA exam topics.

Overview of Alternative Investments in Portfolio Allocation

Alternative investments include asset classes beyond the traditional stocks, bonds, and cash. They encompass a range of assets such as private equity, hedge funds, real estate, commodities, infrastructure, and more. These investments are often included in portfolios to enhance diversification, potentially improve returns, and manage risks more effectively.

Unlike traditional asset classes, alternative investments tend to exhibit unique characteristics, such as lower liquidity, higher complexity, and different risk-return profiles. They are less correlated with traditional investments, meaning they often behave differently in response to market conditions, which can reduce overall portfolio volatility.

In portfolio allocation, alternative investments serve specific roles:

- Diversification: By including assets with low or negative correlation to traditional investments, alternative assets help reduce unsystematic risk.

- Risk Management: Alternatives like real estate or commodities may act as hedges during inflationary periods or economic downturns, stabilizing the portfolio.

- Return Enhancement: Certain alternative assets, such as private equity or hedge funds, have the potential for higher returns, though often with increased risk.

Investors should carefully consider factors such as liquidity, fees, transparency, and the investor’s time horizon and risk tolerance when allocating to alternative investments. Proper allocation to these assets requires strategic planning and may involve weighing the trade-offs between return potential and added complexity, aligning with specific investment goals and risk profiles.

Risk-Return Characteristics of Alternative Investments

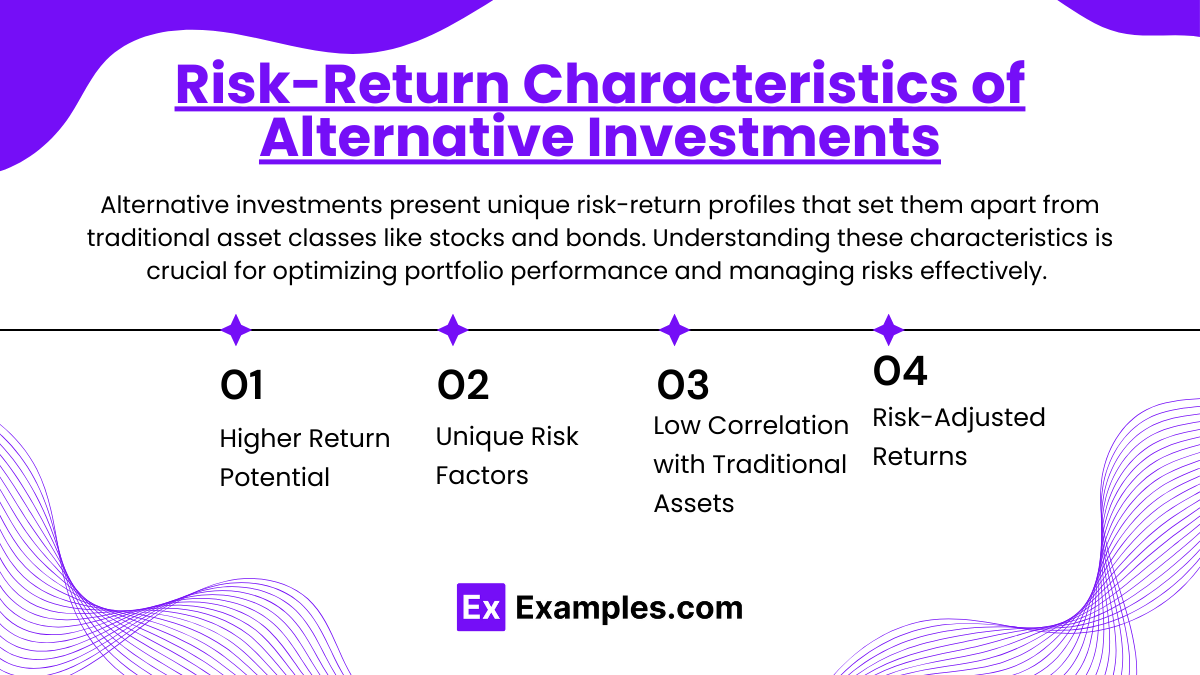

Alternative investments present unique risk-return profiles that set them apart from traditional asset classes like stocks and bonds. Understanding these characteristics is crucial for optimizing portfolio performance and managing risks effectively.

- Higher Return Potential: Certain alternative investments, such as private equity and hedge funds, aim for returns that can exceed those of traditional investments. Private equity, for instance, often targets high-growth companies or turnaround opportunities that may yield substantial profits. Hedge funds use diverse strategies, including leverage and short selling, to pursue gains that are less dependent on traditional market movements.

- Unique Risk Factors: Alternative investments carry specific risks:

- Liquidity Risk: Many alternative assets, such as real estate and private equity, are illiquid. Investors may face lock-up periods or limited exit options, making it harder to access their capital quickly.

- Complexity and Transparency Risk: Alternatives can involve complex strategies and structures, making them less transparent and more challenging to analyze than traditional assets. Hedge funds, for example, may use derivatives, leverage, or non-traditional strategies that require a sophisticated understanding.

- Manager Risk: Performance can be highly dependent on the expertise of fund managers, particularly in hedge funds and private equity. Investors face the risk of underperformance if managers don’t execute their strategies effectively.

- Low Correlation with Traditional Assets: Many alternative investments have lower correlation with stocks and bonds, meaning they are less likely to be affected by the same economic factors as traditional assets. For instance, commodities may perform well during inflation, while real estate can offer steady returns even when equities are volatile. This low correlation helps to reduce overall portfolio volatility, acting as a stabilizing force during market downturns.

- Risk-Adjusted Returns: The potential for attractive risk-adjusted returns is a primary reason for including alternatives in a portfolio. The returns are often accompanied by higher risks, but the addition of these assets can improve the risk-return profile of a portfolio when managed appropriately. Real estate, for example, tends to offer steady income with moderate risk, while commodities can serve as an inflation hedge.

Overall, the risk-return characteristics of alternative investments make them valuable tools for achieving diversified, balanced portfolios. However, the potential for higher returns comes with unique risks, requiring careful evaluation and expertise to maximize their benefits within an investment strategy.

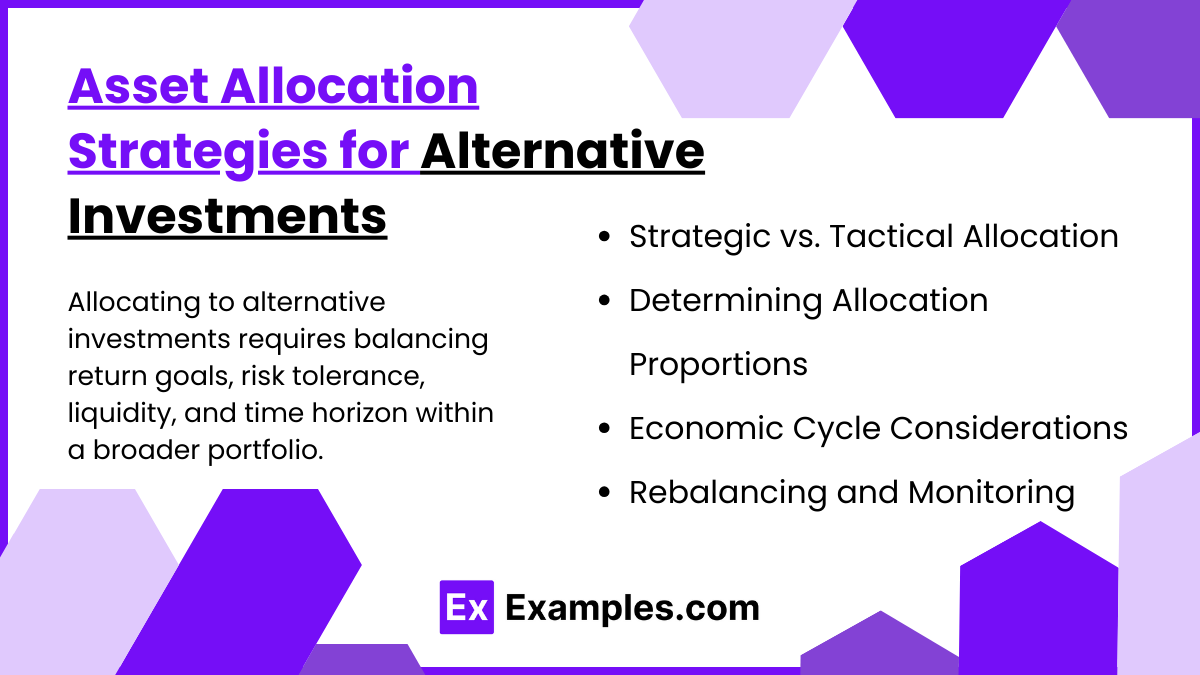

Asset Allocation Strategies for Alternative Investments

Allocating assets to alternative investments involves strategies that optimize the benefits of these unique assets within a broader portfolio. Effective allocation to alternatives requires balancing return objectives, risk tolerance, liquidity needs, and the investor’s time horizon. Here are key strategies for allocating to alternative investments:

- Strategic vs. Tactical Allocation

- Strategic Asset Allocation: This approach is long-term and aligns with an investor’s fundamental objectives and risk profile. Strategic allocation involves setting fixed target weights for alternative assets, such as private equity, real estate, or commodities, based on their role in the portfolio. Periodic rebalancing is done to maintain these target weights.

- Tactical Asset Allocation: This short-term strategy allows for adjusting allocations in response to market conditions or anticipated economic changes. Investors may overweight or underweight certain alternatives, such as increasing commodities during inflationary periods, to capture potential gains and mitigate risks associated with current market dynamics.

- Determining Allocation Proportions

- Risk Tolerance and Return Objectives: Investors determine the proportion of alternatives based on their risk appetite and return expectations. Higher-risk investors may allocate more to volatile alternatives, such as hedge funds or venture capital, seeking higher returns, while conservative investors may opt for stable alternatives, like real estate.

- Time Horizon: Longer time horizons support higher allocations to illiquid alternatives, such as private equity and real estate, as these investments may require capital to be tied up for several years to realize returns.

- Client-Specific Objectives: Tailoring allocation proportions to individual needs, such as income generation or capital appreciation, helps align alternative investments with specific financial goals.

- Economic Cycle Considerations

- Alternative investment performance can vary with economic cycles, making it essential to consider these cycles in allocation decisions. For instance:

- Real Estate: Often performs well in periods of economic expansion with low-interest rates, providing rental income and potential appreciation.

- Commodities: Typically serve as an inflation hedge and may be favored in inflationary or late-cycle environments.

- Hedge Funds: Certain hedge fund strategies, such as long-short equity or global macro, can perform well in volatile markets, providing downside protection during economic downturns.

- Alternative investment performance can vary with economic cycles, making it essential to consider these cycles in allocation decisions. For instance:

- Rebalancing and Monitoring

- Periodic Rebalancing: Because alternative investments often experience varying levels of performance relative to traditional assets, periodic rebalancing helps maintain target allocations and risk levels. This process may involve increasing or decreasing positions in certain alternatives to ensure alignment with long-term strategic goals.

- Performance and Risk Monitoring: Regularly reviewing the performance, risk characteristics, and liquidity of alternative investments ensures they continue to meet the portfolio’s objectives. Monitoring is crucial for managing manager-specific risks, as well as adapting to any shifts in market conditions or economic forecasts.

Implementing these asset allocation strategies requires understanding how alternative assets behave under different conditions and tailoring allocations to meet overall portfolio goals. By managing exposure levels and adjusting allocations strategically, investors can effectively enhance returns and manage risks associated with alternative investments.

Examples

Example 1

A pension fund allocates 15% of its total assets to alternative investments, including 5% in real estate, 5% in private equity, and 5% in hedge funds. The real estate investments aim to provide stable income through rental yields, while private equity offers potential for high growth. Hedge funds are included to provide diversification and reduce volatility within the overall portfolio.

Example 2

An endowment fund adopts a strategic allocation strategy, designating 20% of its portfolio to alternatives. This allocation includes 8% to commodities as an inflation hedge, 7% to infrastructure for steady cash flows, and 5% to private debt for higher yields. The fund periodically rebalances these holdings based on economic conditions to maintain its strategic weightings.

Example 3

A high-net-worth individual allocates 30% of their portfolio to alternative investments, with 10% in venture capital, 10% in hedge funds, and 10% in real estate. The venture capital allocation focuses on emerging technology startups with high growth potential, while hedge funds are selected to diversify risks. Real estate investments are aimed at providing a stable income base and capital appreciation over time.

Example 4

An insurance company invests 12% of its portfolio in alternative assets, including 6% in private equity and 6% in commodities. The private equity investments target mature companies with stable cash flows, aligning with the company’s long-term liabilities. Commodities are included to act as a buffer against inflation, preserving purchasing power for the company’s future obligations.

Example 5

A family office allocates 25% of its investment portfolio to alternatives, dividing the allocation as follows: 10% to hedge funds, 8% to real estate, and 7% to infrastructure projects. The hedge funds provide downside protection during market volatility, real estate investments offer a balance of income and appreciation, and infrastructure projects offer steady cash flows, aligning with the family’s objective for wealth preservation and income stability

Practice Questions

Question 1

Which of the following best describes the primary benefit of including alternative investments in a diversified portfolio?

A. Higher liquidity and lower fees

B. Enhanced diversification and potential for risk-adjusted returns

C. Guaranteed returns and reduced management complexity

D. Reduced market volatility and increased transparency

Answer: B. Enhanced diversification and potential for risk-adjusted returns

Explanation:

Alternative investments often have lower correlations with traditional asset classes like stocks and bonds, which helps enhance diversification in a portfolio. They also provide opportunities for higher risk-adjusted returns, although they may come with increased complexity, fees, and lower liquidity. Options A, C, and D do not accurately reflect the benefits and characteristics of alternative investments.

Question 2

An investor with a long-term horizon and high-risk tolerance is most likely to allocate a significant portion of their portfolio to which type of alternative investment?

A. Money market funds

B. Venture capital

C. Government bonds

D. Treasury bills

Answer: B. Venture capital

Explanation:

Venture capital is suitable for investors with a long-term horizon and high-risk tolerance, as it involves investing in high-growth, often high-risk, early-stage companies. Options A, C, and D are more conservative investments that do not align with the risk and return profile desired by this type of investor.

Question 3

Which alternative asset class is most often used as a hedge against inflation within a portfolio?

A. Hedge funds

B. Real estate

C. Private equity

D. Corporate bonds

Answer: B. Real estate

Explanation:

Real estate is commonly used as an inflation hedge because property values and rental income tend to increase with inflation. This asset class can help maintain purchasing power within a portfolio. While hedge funds and private equity may provide diversification benefits, they do not typically act as inflation hedges. Corporate bonds, on the other hand, may be negatively affected by inflation due to fixed interest payments.