Financial Analysis Techniques

Financial Analysis Techniques are essential tools in evaluating a company’s financial health and performance. This topic focuses on a variety of methods, including ratio analysis, trend analysis, and common-size statements, which allow analysts to assess profitability, liquidity, and solvency. Understanding these techniques provides insights into financial statements, enabling a thorough comparison of companies within an industry or across sectors. By mastering these techniques, financial analysts can make informed decisions, identify strengths and weaknesses, and forecast future financial performance, supporting both investment strategies and risk assessment.

Learning Objectives

In studying “Financial Analysis Techniques” for the CFA, you should learn to evaluate financial statements and apply key ratios to assess a company’s profitability, liquidity, solvency, and operational efficiency. Understand the use of vertical and horizontal analysis to compare financial performance over time and across companies. Gain proficiency in calculating and interpreting ratios related to return on equity, asset turnover, debt levels, and liquidity. Analyze financial data to identify trends, red flags, and opportunities for improvement in a company’s financial health. Additionally, learn to apply financial analysis techniques in valuing a business and making informed investment decisions based on financial performance and industry benchmarks.

Evaluating Financial Statements

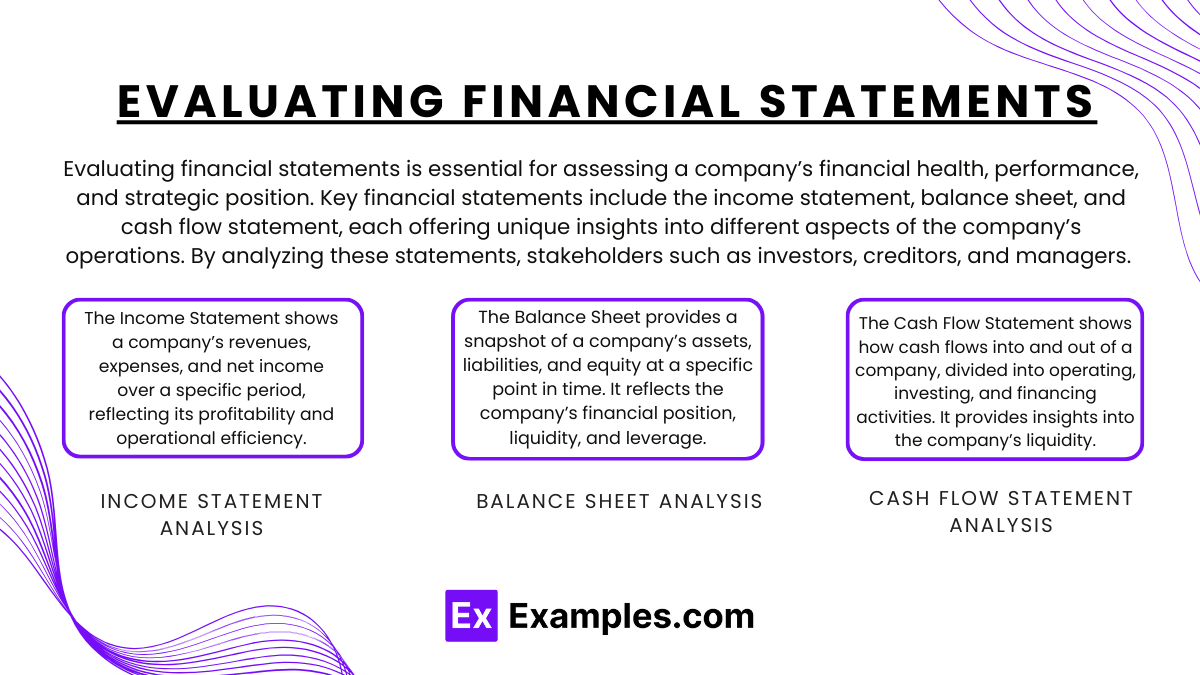

Evaluating financial statements is essential for assessing a company’s financial health, performance, and strategic position. Key financial statements include the income statement, balance sheet, and cash flow statement, each offering unique insights into different aspects of the company’s operations. By analyzing these statements, stakeholders such as investors, creditors, and managers can make informed decisions. Here’s a breakdown of how to evaluate financial statements effectively:

1. Income Statement Analysis

The Income Statement (or Profit & Loss Statement) shows a company’s revenues, expenses, and net income over a specific period, reflecting its profitability and operational efficiency.

Key Components of Income Statement Analysis

- Revenue Growth: Assessing trends in revenue growth reveals if the company’s products or services are experiencing increasing demand.

- Gross Profit Margin: Gross profit margin (gross profit divided by revenue) indicates the percentage of revenue remaining after the cost of goods sold (COGS). A high gross margin suggests effective cost control and pricing strategies.

- Operating Expenses: Analyzing expenses, such as selling, general, and administrative (SG&A) costs, provides insight into the company’s efficiency. Increasing expenses without corresponding revenue growth may signal inefficiencies.

- Operating Income (EBIT): Earnings Before Interest and Taxes (EBIT) reveals the company’s operational performance, excluding financing and tax effects.

- Net Profit Margin: The net profit margin (net income divided by revenue) indicates the portion of revenue that remains as profit after all expenses. A stable or growing net margin indicates strong profitability and cost management.

Common Ratios for Income Statement Analysis

- Gross Profit Margin = Gross Profit / Revenue

- Operating Margin = Operating Income / Revenue

- Net Profit Margin = Net Income / Revenue

- Earnings per Share (EPS) = Net Income / Outstanding Shares

Example: A company with a rising gross profit margin and stable operating expenses demonstrates efficient production and cost control, leading to improved profitability.

2. Balance Sheet Analysis

The Balance Sheet provides a snapshot of a company’s assets, liabilities, and equity at a specific point in time. It reflects the company’s financial position, liquidity, and leverage, helping assess its ability to meet obligations and fund growth.

Key Components of Balance Sheet Analysis

- Current Assets and Liabilities: Assessing current assets (e.g., cash, accounts receivable, inventory) and current liabilities (e.g., accounts payable, short-term debt) helps gauge the company’s liquidity and ability to meet short-term obligations.

- Long-Term Assets and Liabilities: Analyzing long-term assets (e.g., property, equipment, and intangible assets) and long-term liabilities (e.g., bonds, loans) reveals the company’s capital structure and financial stability.

- Shareholders’ Equity: Equity represents the ownership interest in the company, including retained earnings and capital raised from shareholders. A growing equity base often signals profitability and reinvestment.

Common Ratios for Balance Sheet Analysis

- Current Ratio = Current Assets / Current Liabilities (indicates short-term liquidity)

- Quick Ratio = (Current Assets – Inventory) / Current Liabilities (indicates liquidity without relying on inventory)

- Debt-to-Equity Ratio = Total Liabilities / Shareholders’ Equity (measures financial leverage and risk)

- Return on Equity (ROE) = Net Income / Shareholders’ Equity (measures profitability relative to equity)

Example: A company with a high current ratio and low debt-to-equity ratio has strong liquidity and financial stability, making it less vulnerable to financial distress.

3. Cash Flow Statement Analysis

The Cash Flow Statement shows how cash flows into and out of a company, divided into operating, investing, and financing activities. It provides insights into the company’s liquidity, cash generation, and capital allocation.

Key Components of Cash Flow Statement Analysis

- Operating Cash Flow: Cash flow from operations indicates the cash generated from core business activities. Positive operating cash flow is a strong indicator of the company’s ability to fund itself.

- Investing Cash Flow: Cash used in or provided by investing activities, such as purchasing equipment or selling assets, shows how the company is allocating capital for growth. Negative cash flow from investing activities is typical for growing companies.

- Financing Cash Flow: Cash from financing activities, such as issuing debt or equity or paying dividends, reveals how the company funds its operations and returns capital to shareholders.

Common Ratios for Cash Flow Statement Analysis

- Operating Cash Flow to Sales Ratio = Operating Cash Flow / Revenue (indicates cash generation efficiency relative to sales)

- Free Cash Flow (FCF) = Operating Cash Flow – Capital Expenditures (measures cash available after reinvestment in the business)

- Cash Flow Coverage Ratio = Operating Cash Flow / Total Debt (indicates the ability to cover debt obligations with cash flow)

Example: A company with high and growing free cash flow can reinvest in the business or return capital to shareholders, enhancing shareholder value.

Vertical and Horizontal Analysis

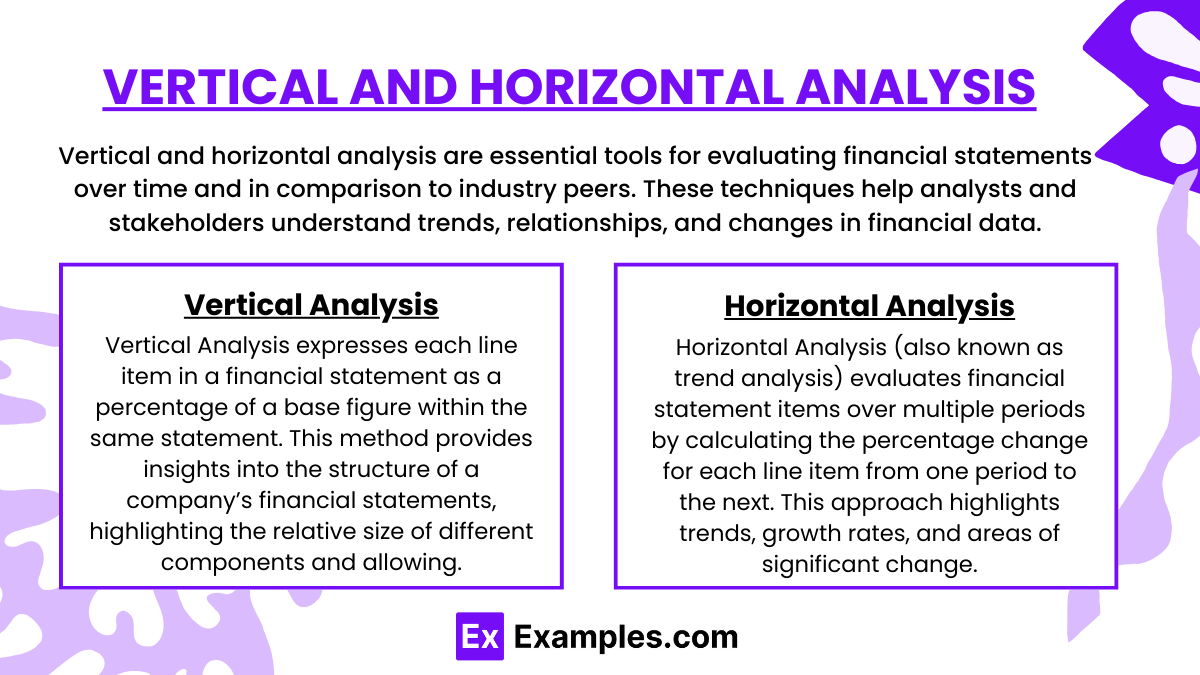

Vertical and horizontal analysis are essential tools for evaluating financial statements over time and in comparison to industry peers. These techniques help analysts and stakeholders understand trends, relationships, and changes in financial data, enabling a more comprehensive assessment of a company’s financial health and performance.

1. Vertical Analysis

Vertical Analysis (also known as common-size analysis) expresses each line item in a financial statement as a percentage of a base figure within the same statement. This method provides insights into the structure of a company’s financial statements, highlighting the relative size of different components and allowing for easier comparison across periods or with other companies

How Vertical Analysis Works

- Income Statement: Each item is shown as a percentage of total revenue (or net sales), giving insight into how much of each dollar of revenue is spent on COGS, operating expenses, and taxes.

- Balance Sheet: Each item is shown as a percentage of total assets or total liabilities and equity, highlighting the proportion of different asset classes, liabilities, and equity in the company’s financial structure.

2. Horizontal Analysis

Horizontal Analysis (also known as trend analysis) evaluates financial statement items over multiple periods by calculating the percentage change for each line item from one period to the next. This approach highlights trends, growth rates, and areas of significant change, allowing stakeholders to assess a company’s financial trajectory.

How Horizontal Analysis Works

- Year-over-Year Comparison: Each line item is compared to its value in a prior period, with the percentage change calculated to show growth, stability, or decline over time.

- Multi-Year Trends: By analyzing data over several years, horizontal analysis provides insights into long-term trends and the consistency of a company’s performance.

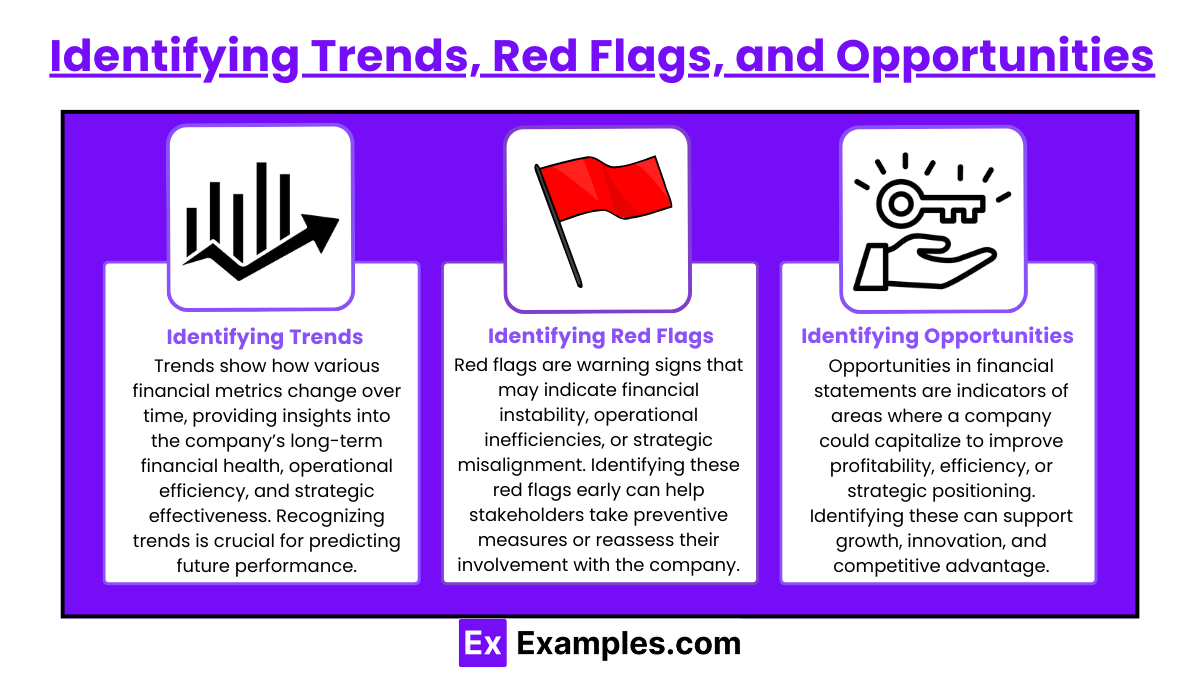

Identifying Trends, Red Flags, and Opportunities

1. Identifying Trends

Trends show how various financial metrics change over time, providing insights into the company’s long-term financial health, operational efficiency, and strategic effectiveness. Recognizing trends is crucial for predicting future performance and making informed investment or management decisions.

Key Trends to Look For

- Revenue Growth: A consistent increase in revenue indicates strong demand for products or services and effective sales strategies. Conversely, stagnant or declining revenue may suggest market challenges.

- Profitability Trends: Examining gross profit, operating profit, and net profit margins over time can reveal if the company is improving its cost efficiency and operational performance.

- Expense Management: Tracking changes in major expense categories, such as COGS, SG&A, and R&D, shows if the company is managing costs effectively. Rising costs relative to revenue may require closer examination.

- Cash Flow Stability: Consistent positive operating cash flows indicate a healthy cash-generating business. Examining trends in free cash flow reveals whether the company has funds for reinvestment and growth.

- Debt Levels: A stable or declining debt-to-equity ratio suggests responsible debt management, while rising debt levels relative to equity may signal financial stress.

Example: A retail company with consistent revenue growth, stable or improving profit margins, and positive cash flow trends likely demonstrates effective cost management and a growing customer base.

2. Identifying Red Flags

Red flags are warning signs that may indicate financial instability, operational inefficiencies, or strategic misalignment. Identifying these red flags early can help stakeholders take preventive measures or reassess their involvement with the company.

Common Red Flags

- Declining Revenue: Persistent revenue declines can indicate weakening demand, increased competition, or loss of market share.

- Rising COGS or Operating Expenses: If COGS or operating expenses increase faster than revenue, it may signal cost inefficiencies or rising input costs, which could erode profitability.

- Negative Cash Flow: A prolonged negative operating cash flow may suggest that the company is struggling to generate enough cash from its operations, possibly requiring external funding.

- High Leverage and Debt Levels: A high or increasing debt-to-equity ratio indicates financial risk, especially if interest expenses grow and coverage ratios decline, signaling potential issues with debt servicing.

- Decreasing Margins: Shrinking gross, operating, or net profit margins can indicate pricing pressures, increased costs, or declining efficiency.

- Inventory Buildup: Rising inventory levels relative to sales can be a red flag for overproduction or slowing demand, tying up cash in unsold goods.

Example: A manufacturing company with declining revenue, increasing debt, and rising inventory levels may face financial strain, suggesting potential challenges in market demand or operational efficiency.

3. Identifying Opportunities

Opportunities in financial statements are indicators of areas where a company could capitalize to improve profitability, efficiency, or strategic positioning. Identifying these can support growth, innovation, and competitive advantage.

Key Opportunities to Consider

- Improving Margins: If the company’s gross profit or operating margins are lower than industry averages, there may be opportunities to improve pricing strategies, negotiate better supplier terms, or streamline operations.

- Growing Market Segments: Revenue growth in specific product lines or geographic regions highlights areas of high demand, presenting opportunities for increased focus or investment.

- Cash Flow Surplus: A strong free cash flow position provides the company with flexibility to reinvest in growth, pay down debt, or return capital to shareholders.

- Underutilized Assets: Reviewing the balance sheet for underutilized assets, such as excess cash or real estate, may reveal opportunities for reinvestment, asset sales, or expansion.

- Innovation in R&D: A significant portion of spending on R&D can indicate a strong commitment to innovation, potentially leading to new products, services, or cost-saving technologies that can drive future growth.

- Mergers and Acquisitions (M&A): A strong cash position and low debt levels may provide an opportunity for strategic acquisitions that enhance market position, diversify revenue streams, or offer operational synergies.

Example: A technology firm with robust free cash flow, low debt, and a growing customer base may have the opportunity to invest in product development or consider strategic acquisitions to strengthen its market position.

Applying Key Ratios for Financial Assessment

Evaluating financial ratios helps stakeholders understand a company’s performance, financial health, and strategic potential. Ratios can reveal insights into profitability, liquidity, efficiency, leverage, and market valuation, providing a comprehensive view of the company’s strengths and weaknesses. Here’s an overview of key ratios used for financial assessment and what they indicate.

1. Profitability Ratios

Profitability ratios gauge a company’s ability to generate profit relative to its revenues, assets, and equity. These ratios highlight how efficiently the company manages its expenses and operations to produce earnings.

Key Profitability Ratios

- Gross Profit Margin: Shows the percentage of revenue left after covering direct production costs, reflecting the company’s production efficiency.

- Operating Profit Margin: Reveals how much revenue remains after accounting for all operating expenses, providing insights into operational efficiency.

- Net Profit Margin: Indicates the portion of revenue retained as profit after all costs, taxes, and interest, showing overall profitability.

- Return on Assets (ROA): Assesses how effectively the company uses its assets to generate profit, with a higher ratio suggesting efficient asset utilization.

- Return on Equity (ROE): Measures how well the company generates returns on shareholder investments, indicating how effectively equity is used.

Insight: Consistently high profitability ratios suggest effective management and strong earnings potential, while lower ratios may indicate challenges in cost control or pricing.

2. Liquidity Ratios

Liquidity ratios measure a company’s ability to meet its short-term obligations, highlighting financial flexibility and solvency. These ratios are crucial for assessing whether a company has enough assets to cover its liabilities in the near term.

Key Liquidity Ratios

- Current Ratio: Reflects the company’s capacity to pay short-term debts with short-term assets, providing a general sense of liquidity.

- Quick Ratio: Excludes inventory from current assets to focus on highly liquid assets, giving a stricter view of the company’s ability to cover short-term liabilities.

- Cash Ratio: Measures the company’s ability to pay off current liabilities using cash alone, indicating immediate liquidity.

Insight: High liquidity ratios imply that the company can comfortably meet its short-term obligations, while lower ratios may suggest potential liquidity issues or reliance on inventory or credit.

3. Efficiency Ratios

Efficiency ratios assess how well a company utilizes its assets and manages its liabilities. These ratios provide insights into operational efficiency and asset management, showing how effectively the company generates revenue from its resources.

Key Efficiency Ratios

- Inventory Turnover: Indicates how frequently inventory is sold and replaced, reflecting inventory management efficiency.

- Receivables Turnover: Measures how effectively the company collects payments from customers, indicating efficiency in managing credit.

- Asset Turnover: Shows how well the company uses its assets to generate revenue, with a higher ratio suggesting more effective asset utilization.

Insight: High efficiency ratios demonstrate strong asset management and operational efficiency, while lower ratios may indicate underutilized assets or slow collections.

4. Leverage Ratios

Leverage ratios evaluate the company’s use of debt in its capital structure and assess its ability to meet financial obligations. These ratios highlight the level of financial risk and indicate how much the company relies on debt financing.

Key Leverage Ratios

- Debt-to-Equity Ratio: Shows the proportion of debt compared to equity, indicating the extent of leverage and financial risk.

- Debt Ratio: Reflects the percentage of assets financed by debt, highlighting the level of financial leverage.

- Interest Coverage Ratio: Measures the company’s ability to cover interest payments with operating income, indicating how comfortably it can manage its debt obligations.

Insight: Moderate leverage ratios suggest balanced use of debt, while high leverage ratios indicate greater financial risk, potentially signaling vulnerability during economic downturns.

5. Market Ratios

Market ratios evaluate a company’s stock performance relative to earnings, dividends, and book value. These ratios are used by investors to assess valuation, growth potential, and returns.

Key Market Ratios

- Price-to-Earnings (P/E) Ratio: Shows how much investors are willing to pay for each dollar of earnings, reflecting market expectations for growth.

- Earnings per Share (EPS): Indicates profit allocated to each outstanding share, showing the earning power of individual shares.

- Dividend Yield: Represents the return on investment from dividends relative to the stock price, important for income-focused investors.

- Price-to-Book (P/B) Ratio: Compares the market price to the book value of equity, showing how investors value the company relative to its assets.

Insight: High P/E and P/B ratios suggest high growth expectations, while high dividend yields appeal to income investors. Lower ratios may indicate undervaluation or limited growth prospects.

Examples

Example 1: Ratio Analysis

Ratio analysis involves evaluating the relationships between various financial statement items to assess a company’s performance and financial health. Common ratios include the current ratio, which measures liquidity; the return on equity (ROE), which assesses profitability; and the debt-to-equity ratio, which evaluates leverage. By analyzing these ratios, investors and analysts can compare a company’s performance over time and against industry peers, providing valuable insights for decision-making.

Example 2: Vertical Analysis

Vertical analysis is a technique that presents each item in a financial statement as a percentage of a base item, allowing for easy comparison across time periods and companies. For example, in an income statement, each expense can be expressed as a percentage of total revenue. This approach highlights the relative size of various financial components and helps identify trends, such as changes in cost structure or profit margins, facilitating a clearer understanding of a company’s operational efficiency.

Example 3: Horizontal Analysis

Horizontal analysis focuses on the changes in financial statement line items over time, comparing the same item across different periods. This technique allows analysts to identify trends, growth rates, and anomalies in financial performance. For instance, a company may evaluate its sales revenue over several years to determine growth patterns and understand the factors driving increases or declines. This comparative analysis is essential for forecasting future performance and making informed strategic decisions.

Example 4: Cash Flow Analysis

Cash flow analysis examines the inflows and outflows of cash within a company over a specific period. This technique is crucial for understanding a company’s liquidity and ability to generate cash to fund operations, pay debts, and invest in growth. By analyzing cash flow statements, investors can assess operational efficiency, working capital management, and financial sustainability, helping them gauge the company’s short-term and long-term viability.

Example 5: Trend Analysis

Trend analysis involves evaluating historical financial data to identify patterns and predict future performance. Analysts look at various metrics, such as revenue, expenses, and profit margins, over time to establish trends. For example, a company may analyze its sales growth rate over the past five years to forecast future revenue. This technique is valuable for strategic planning and risk assessment, enabling businesses to make proactive decisions based on observed patterns and market conditions.

Practice Questions

Question 1

Which of the following techniques is commonly used to evaluate a company’s profitability?

A) Ratio analysis

B) Cost-volume-profit analysis

C) Trend analysis

D) All of the above

Correct Answer: D) All of the above.

Explanation: All of the listed techniques can be utilized to evaluate a company’s profitability. Ratio analysis helps assess profitability through metrics such as net profit margin and return on equity. Cost-volume-profit analysis examines how changes in costs and volume affect profit, while trend analysis looks at historical data to identify patterns over time. Using these techniques collectively provides a comprehensive view of a company’s profitability.

Question 2

What is the primary purpose of horizontal analysis in financial statements?

A) To compare a company’s financial performance with industry averages

B) To evaluate financial performance over multiple periods

C) To assess the financial health of a company at a specific point in time

D) To analyze the relationship between different financial metrics

Correct Answer: B) To evaluate financial performance over multiple periods.

Explanation: Horizontal analysis involves comparing financial statement line items over several periods to identify trends and growth patterns. This technique allows analysts to evaluate how specific accounts have changed over time, facilitating a better understanding of a company’s financial performance. Options A and D refer to other forms of analysis, while C describes vertical analysis.

Question 3

Which financial analysis technique focuses on the relationship between different financial statement items?

A) Ratio analysis

B) Vertical analysis

C) Horizontal analysis

D) Sensitivity analysis

Correct Answer: A) Ratio analysis.

Explanation: Ratio analysis is a financial analysis technique that examines the relationships between different financial statement items, such as profitability, liquidity, and solvency ratios. It allows analysts to assess a company’s financial health, operational efficiency, and performance compared to industry benchmarks. Vertical analysis focuses on the composition of financial statements, while horizontal analysis examines trends over time. Sensitivity analysis assesses how changes in one variable affect outcomes but does not primarily focus on the relationships between financial statement items.