Fixed-Income Issuance and Trading

Preparing for the CFA Exam requires a solid understanding of Fixed-Income Issuance and Trading, a key component of the Fixed-Income foundation. Mastery of debt issuance processes, trading mechanisms, and market participants is essential. This knowledge provides insights into bond markets, pricing, and yield structures, crucial for achieving a high CFA score.

Learning Objective

In studying "Fixed-Income Issuance and Trading" for the CFA Exam, you should develop an understanding of the processes involved in issuing fixed-income securities, including public offerings and private placements. Learn the roles of different market participants, such as underwriters, issuers, and institutional investors, in both primary and secondary markets. Explore trading mechanisms and platforms for fixed-income securities, including over-the-counter (OTC) and exchange-traded environments. Evaluate the principles behind pricing, yield calculations, and trading strategies. Additionally, understand how regulatory frameworks impact issuance and trading activities, applying this knowledge to analyze fixed-income scenarios and solve complex problems in CFA practice questions.

What is Fixed-Income Securities?

Fixed-income securities are financial instruments that pay a set amount of interest or dividends to investors over a specified period until maturity. Upon maturity, the principal amount is returned to the investor. These securities include bonds, treasury bills, and other debt instruments issued by governments, corporations, or other entities, and are characterized by predictable income streams and lower risk relative to equities.

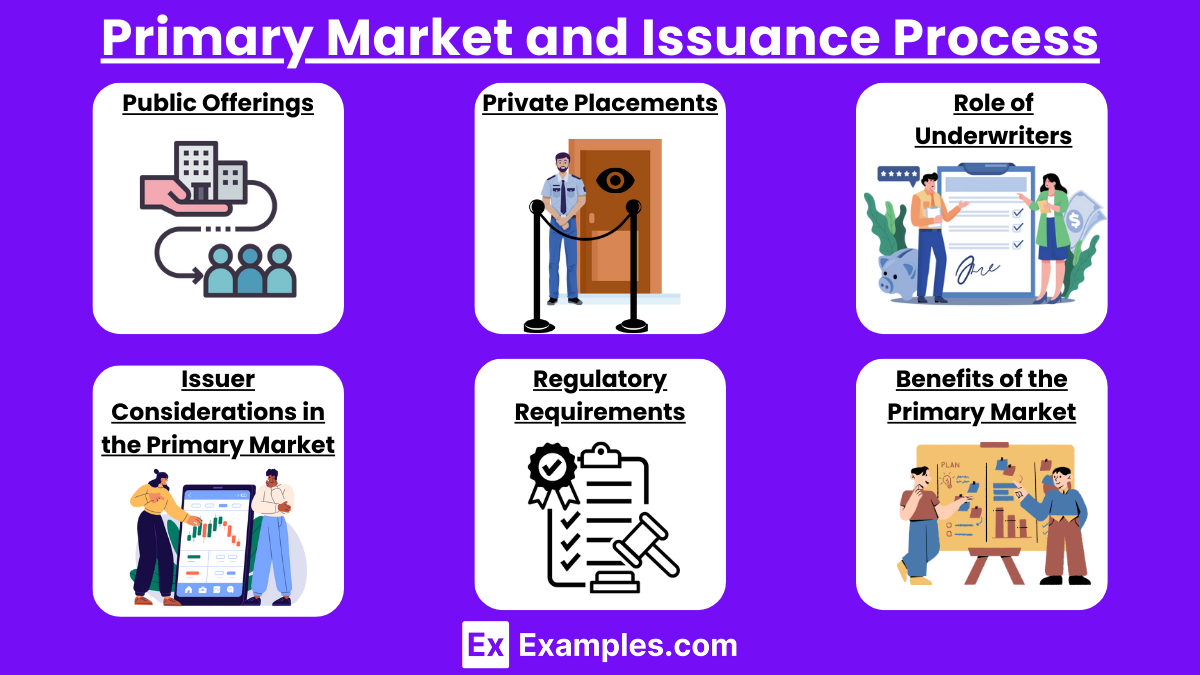

Primary Market and Issuance Process

The Primary Market and Issuance Process is where new securities, including fixed-income securities like bonds, are created and sold for the first time to investors. This market enables issuers, such as corporations, governments, or municipalities, to raise capital by selling these newly issued securities directly to investors. Here’s an overview of the key components and steps involved:

1. Public Offerings

In a public offering, an issuer offers securities to the general public, making them accessible to a wide range of investors.

Underwriting Process: Investment banks (acting as underwriters) help facilitate the issuance. They assess the risk, set a price, and may buy the securities from the issuer to resell to investors.

Initial Pricing and Marketing: Underwriters help determine the issue price based on market conditions, demand, and the issuer's financial health. They also market the securities to ensure successful sales.

2. Private Placements

In private placements, securities are sold directly to select institutional investors, such as mutual funds, insurance companies, or pension funds, rather than the general public.

Advantages for Issuers: Private placements often have fewer regulatory requirements and lower costs, and they allow issuers to raise funds more quickly.

Investor Considerations: Investors in private placements typically require higher returns due to the limited liquidity and higher risks.

3. Role of Underwriters

Syndicate Formation: Large issuances may require a syndicate of multiple investment banks to spread the risk and manage the distribution more effectively.

Pricing and Risk Management: Underwriters analyze the issuer’s credit quality and market conditions to price the security attractively while managing potential risks.

Book-Building Process: For larger issuances, underwriters gauge investor demand by collecting indications of interest, which helps set the final issuance price.

4. Issuer Considerations in the Primary Market

Interest Rates: Issuers aim to raise funds at favorable interest rates. The timing of issuance may depend on the current interest rate environment.

Maturity Terms: Issuers choose maturity periods that align with their financing needs. Shorter maturities provide quicker capital recycling, while longer terms offer stability in funding.

Investor Demand: High demand can lead to favorable pricing and terms, allowing issuers to raise more capital efficiently.

5. Regulatory Requirements

In public offerings, issuers must comply with regulations set by governing bodies like the Securities and Exchange Commission (SEC) in the U.S. These regulations include filing registration statements and providing disclosures to ensure transparency and protect investors.

Private placements are subject to lighter regulatory scrutiny but must adhere to specific requirements, such as limiting the offering to qualified or institutional investors.

6. Benefits of the Primary Market

For Issuers: Enables access to large-scale funding for various purposes, such as expansion, research, or paying down existing debt.

For Investors: Provides opportunities to invest directly in new securities at issuance prices, often with favorable terms compared to secondary market prices.

The primary market and issuance process play a critical role in financial markets by enabling capital formation, supporting economic growth, and offering investment opportunities. After issuance in the primary market, these securities can then be bought and sold in the secondary market

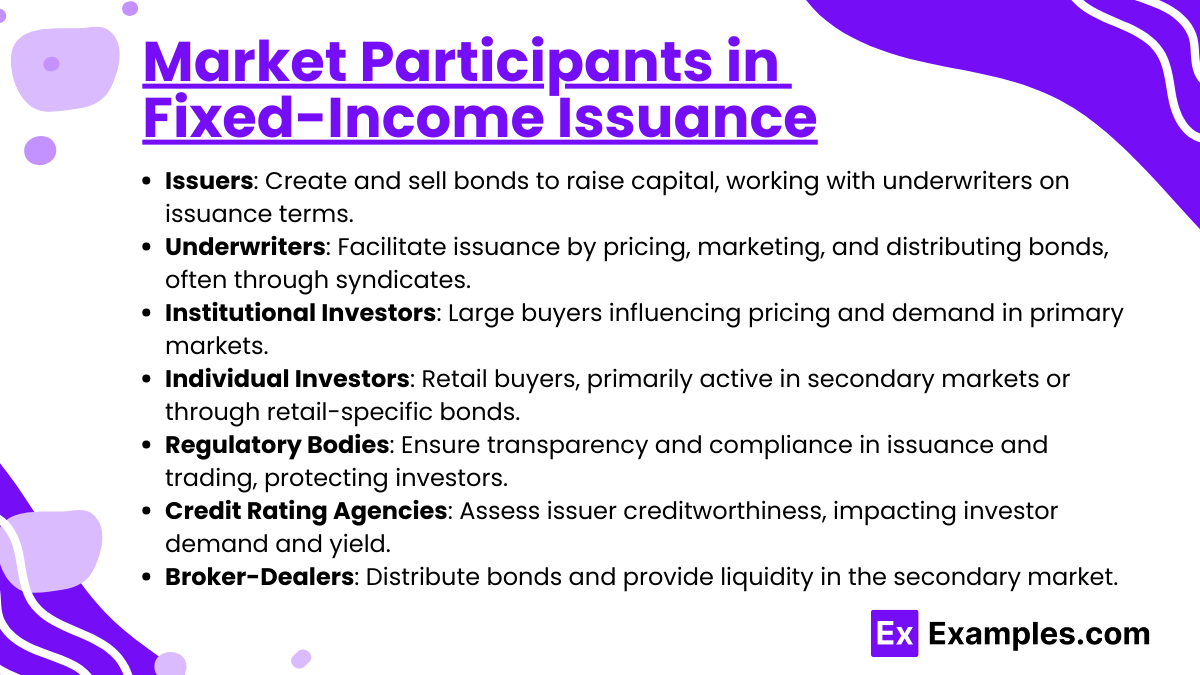

Market Participants in Fixed-Income Issuance

In the Fixed-Income Issuance process, several key market participants play specific roles in ensuring successful issuance and distribution of securities. Here’s a breakdown of these participants and their roles:

1. Issuers

Definition: Entities that create and sell fixed-income securities to raise funds.

Types of Issuers:

Governments: Issue bonds (like treasury bonds) to finance public spending, infrastructure, and other national projects.

Corporations: Issue corporate bonds to finance business expansions, acquisitions, and operational needs.

Municipalities: Local or regional governments issue municipal bonds to fund public projects like schools, roads, and hospitals.

Role: Issuers determine the type, amount, maturity, and interest rate of the securities and work with underwriters to bring the issuance to market.

2. Underwriters

Definition: Financial institutions, usually investment banks, that facilitate the issuance process for fixed-income securities.

Functions:

Pricing and Risk Assessment: Underwriters help set the issue price and terms based on market conditions, demand, and issuer risk profile.

Syndicate Formation: For larger issuances, underwriters may form a syndicate (a group of banks) to share the risk and responsibility of distributing the securities.

Book-Building and Demand Assessment: They gauge investor interest to help set the final issuance price, making the issuance more attractive to potential buyers.

Types of Underwriting:

Firm Commitment: The underwriter buys the entire issuance from the issuer and resells it to investors, assuming the risk of any unsold securities.

Best Efforts: The underwriter commits to selling as much of the issuance as possible but does not assume the risk for any unsold portion.

3. Institutional Investors

Definition: Large-scale investors, such as mutual funds, pension funds, insurance companies, and hedge funds, that purchase substantial portions of fixed-income issuances.

Role:

Primary Market Buyers: Institutional investors often participate in the primary issuance, buying directly from underwriters.

Influence on Pricing: Their demand and purchasing power can influence pricing and issuance terms, as issuers seek to attract their investments.

Long-Term Holders: Many institutional investors buy fixed-income securities for long-term investment, focusing on stable returns and capital preservation.

4. Individual Investors

Definition: Retail investors who may purchase fixed-income securities, though they are usually more active in the secondary market than in primary issuances.

Role:

Indirect Access: Individual investors may gain exposure to new fixed-income issuances through funds or brokerage accounts.

Retail Bonds: Some issuances are structured specifically for retail investors, offering smaller denominations and terms tailored for individual participation.

5. Regulatory Bodies

Definition: Governmental and regulatory agencies that oversee the issuance and trading of fixed-income securities.

Examples:

U.S. Securities and Exchange Commission (SEC): Regulates the issuance process in the U.S. to ensure transparency and protect investors.

Financial Industry Regulatory Authority (FINRA): Oversees the conduct of brokerage firms and investment banks.

Role:

Ensuring Compliance: Regulatory bodies set rules and standards for disclosures, pricing practices, and market fairness.

Investor Protection: Regulations help protect investors by requiring issuers to provide accurate information about the security’s risks and returns.

6. Credit Rating Agencies

Definition: Organizations that assess and assign credit ratings to fixed-income securities, such as bonds, based on the issuer’s creditworthiness.

Examples: Moody’s, Standard & Poor’s (S&P), and Fitch.

Role:

Risk Assessment: Rating agencies evaluate the financial health and repayment capability of issuers, helping investors gauge risk.

Influence on Investor Demand: Higher ratings can attract more investors, as they indicate lower risk. Conversely, lower ratings may deter investors or require issuers to offer higher yields.

7. Broker-Dealers

Definition: Financial intermediaries that buy and sell securities on behalf of clients and may participate in distributing fixed-income issuances.

Role:

Distribution: Broker-dealers help distribute securities to both institutional and retail investors, particularly in the secondary market.

Liquidity Provision: By actively trading securities, broker-dealers help provide liquidity, making it easier for investors to buy or sell fixed-income instruments.

These market participants collectively enable the efficient issuance, distribution, and regulation of fixed-income securities, helping ensure that issuers can access the capital they need while providing investors with secure investment options

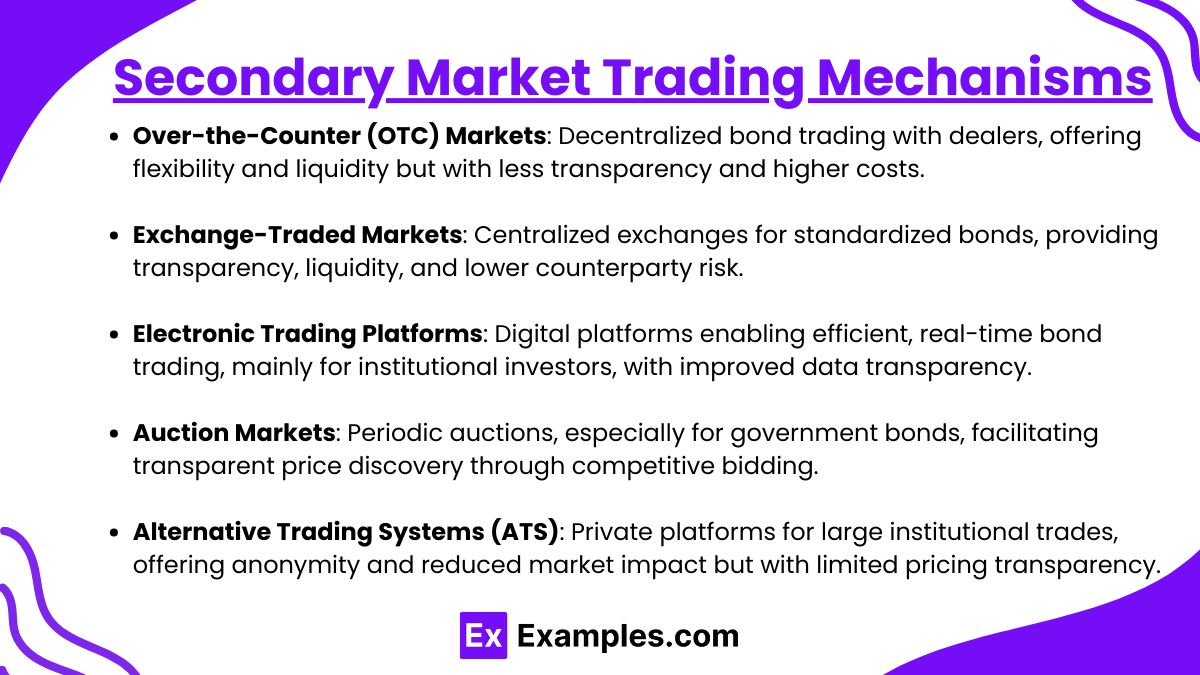

Secondary Market Trading Mechanisms

The Secondary Market Trading Mechanisms in fixed-income markets involve the buying and selling of previously issued fixed-income securities, such as bonds. Unlike the primary market, where securities are sold directly by issuers to investors, the secondary market provides liquidity and price discovery, enabling investors to trade these securities with each other. Here’s an overview of the main trading mechanisms and components:

1. Over-the-Counter (OTC) Markets

Definition: OTC markets are decentralized networks where fixed-income securities are traded directly between parties, typically via brokers or dealers, without a centralized exchange.

Characteristics:

Flexibility: The OTC market allows for a wide variety of bonds, including government, corporate, and municipal bonds, to be traded with custom terms.

Dealer-Based System: Dealers (often large banks or financial institutions) act as intermediaries, buying and selling bonds from their inventories to meet investor demand.

Advantages:

Liquidity: The presence of multiple dealers provides liquidity, even for less commonly traded bonds.

Price Discovery: Through negotiation, the OTC market helps determine the fair value of bonds based on supply and demand.

Challenges:

Less Transparency: Prices are not always as visible as on exchanges, making it more challenging for individual investors to gauge fair value.

Higher Costs: Due to less regulation and direct negotiation, transaction costs can be higher.

2. Exchange-Traded Markets

Definition: In contrast to OTC markets, some fixed-income securities, such as certain government or corporate bonds, may be traded on centralized exchanges like the New York Stock Exchange (NYSE).

Characteristics:

Standardization: Exchange-traded bonds generally have standardized terms, making them easier to trade in a regulated environment.

Transparency: Exchanges provide visible pricing and standardized transaction processes, benefiting investors with up-to-date price information.

Centralized Clearing: Exchanges have a centralized clearing and settlement process that reduces counterparty risk.

Advantages:

Enhanced Liquidity and Transparency: Exchanges offer high liquidity and real-time pricing, making it easier for investors to execute trades at fair market value.

Lower Counterparty Risk: The exchange clearing process reduces the risk of default by the trading counterpart.

Challenges:

Limited Bond Types: Not all bonds are suitable for exchange trading; many remain in OTC markets due to complexity or customization.

3. Electronic Trading Platforms

Definition: Digital platforms that facilitate bond trading between institutional investors and dealers, such as MarketAxess or Bloomberg Terminal, are becoming increasingly popular.

Characteristics:

Real-Time Pricing: Electronic platforms provide up-to-the-minute pricing, allowing for faster trades and improved transparency.

Automated Trading: Some platforms offer automated trading and algorithms to optimize trade execution and manage large orders.

Direct Access: Investors can access multiple dealers and other participants directly, bypassing traditional broker channels.

Advantages:

Increased Efficiency: Electronic trading speeds up transactions, providing greater ease of access and competitive pricing.

Enhanced Data Availability: Investors benefit from data insights and price transparency, helping in decision-making.

Challenges:

Technology Dependence: Reliance on technology means system outages or failures can disrupt trading.

Limited Access for Retail Investors: Many electronic platforms are tailored for institutional users, limiting access for individual investors.

4. Auction Markets

Definition: Certain government bonds, such as U.S. Treasury securities, are issued and traded through periodic auctions. Auctions also act as a secondary market mechanism for these securities.

Characteristics:

Primary Dealer Participation: Primary dealers (large financial institutions) submit bids on behalf of clients or for themselves.

Bid Types: Bids are classified as competitive or non-competitive. Competitive bidders specify the yield or price, while non-competitive bidders accept the auction's determined yield.

Price Discovery: Auctions set the yield and price for government bonds based on investor demand and bid submissions.

Advantages:

Transparent Pricing: Auctions provide a clear mechanism for price discovery, driven by demand and bid types.

Accessibility: Individual investors can participate through non-competitive bids, making it an accessible option.

Challenges:

Limited to Specific Bonds: Auctions are typically limited to government securities, so they are not applicable for corporate or municipal bonds.

5. Alternative Trading Systems (ATS)

Definition: ATS are private trading platforms that match buy and sell orders for bonds, operating outside of traditional exchanges but still regulated.

Characteristics:

Institutional Focus: ATS primarily serve institutional investors, facilitating trades in large blocks to reduce market impact.

Anonymity: ATS provide anonymity for buyers and sellers, which can be advantageous for large trades.

Advantages:

Reduced Market Impact: Large trades on ATS platforms are less likely to influence public market prices, preserving the investor’s position.

Improved Privacy: Anonymity can prevent revealing trading strategies or positions.

Challenges:

Limited Transparency: Less visible pricing can make price discovery challenging for investors without direct platform access

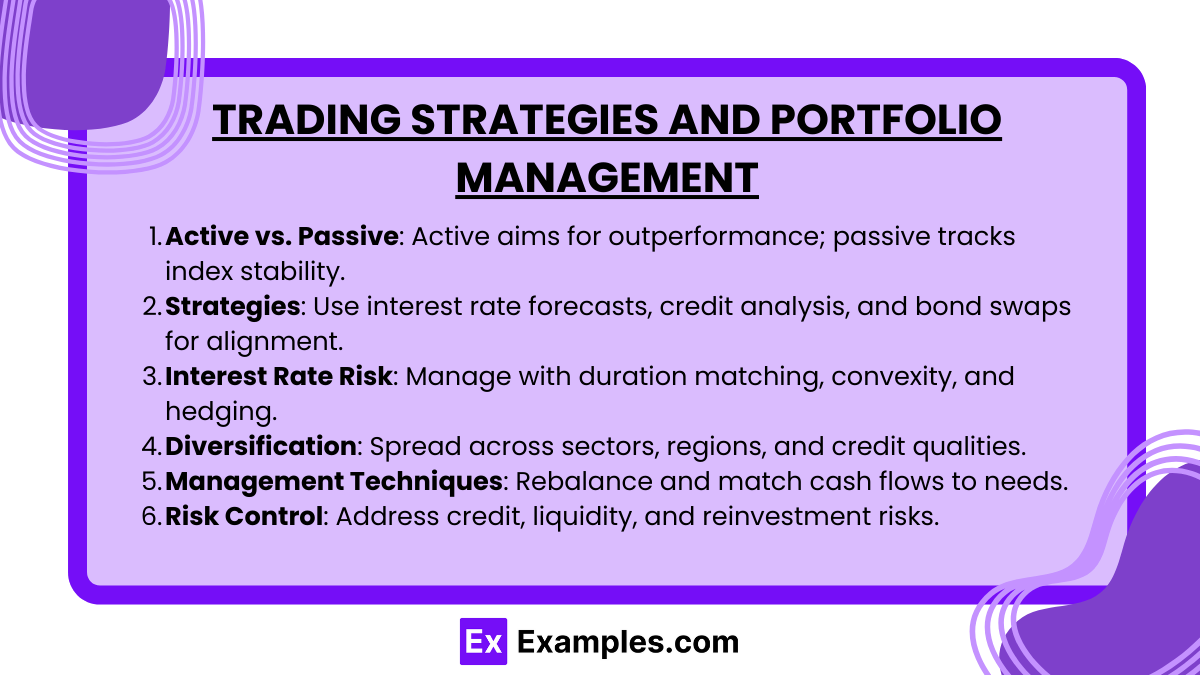

Trading Strategies and Portfolio Management

Fixed-income trading strategies and portfolio management aim to maximize returns while managing risks related to interest rates, credit quality, and market shifts. Key approaches include:

1. Active vs. Passive Management

Active: Involves frequent trading based on interest rate and economic forecasts to outperform a benchmark.

Passive: Aims to replicate index returns, focusing on stability and lower transaction costs.

2. Key Trading Strategies

Interest Rate Anticipation: Adjusts duration and yield curve positioning based on interest rate forecasts (e.g., bullet, barbell, and ladder strategies).

Credit Analysis: Evaluates credit spreads and sector rotation for optimal risk-adjusted returns.

Bond Swaps: Swaps bonds to enhance yield, credit quality, or maturity alignment.

3. Interest Rate Risk Management

Duration Matching: Aligns portfolio duration with the investment horizon.

Convexity and Hedging: Uses convexity analysis and derivatives to mitigate interest rate risks.

4. Portfolio Diversification

Diversifies across sectors, geographic regions, and credit qualities to spread risk and enhance stability.

5. Portfolio Management Techniques

Rebalancing: Adjusts allocations periodically.

Cash Flow Matching and Immunization: Aligns bond maturities with cash flow needs or specific return targets despite interest rate changes.

6. Risk Management

Credit, Liquidity, and Reinvestment Risks: Monitors credit quality, ensures sufficient liquidity, and manages reinvestment risks through strategic maturity distribution

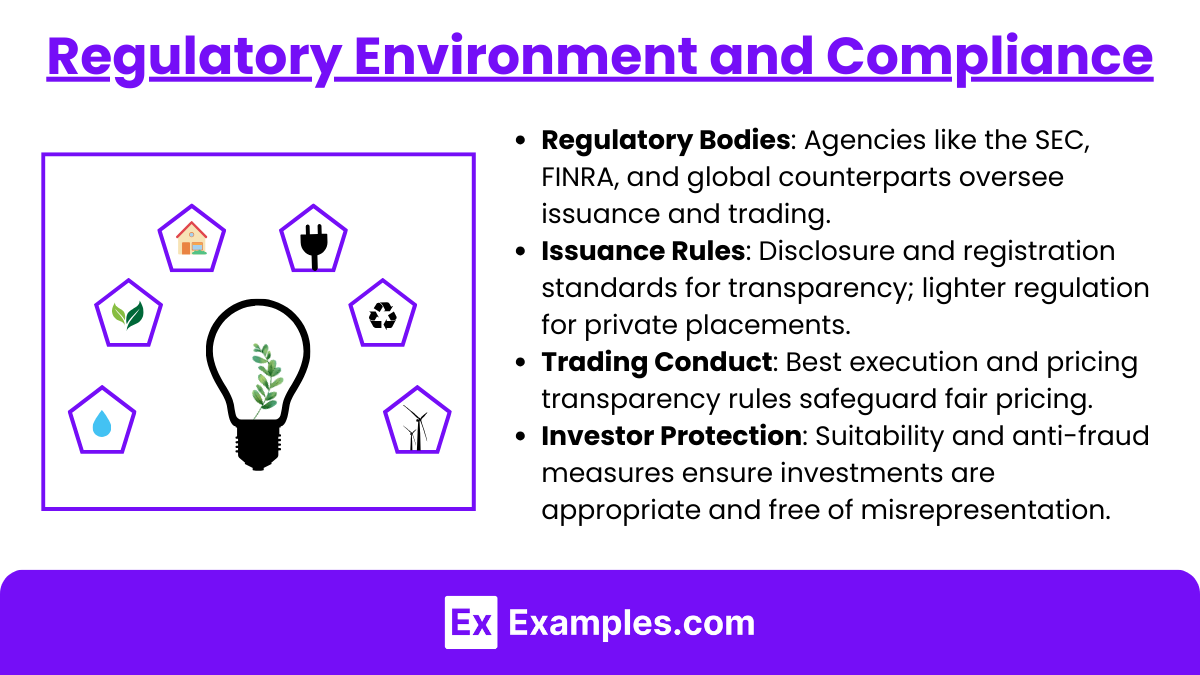

Regulatory Environment and Compliance

The regulatory environment ensures transparency, stability, and fairness in fixed-income markets, protecting investors and maintaining market integrity. Key regulatory aspects include:

1. Regulatory Bodies

SEC (Securities and Exchange Commission): Oversees public fixed-income offerings in the U.S., ensuring proper disclosures and investor protections.

FINRA (Financial Industry Regulatory Authority): Regulates broker-dealers and investment banks involved in fixed-income trading.

Global Counterparts: Other countries have similar bodies, like the FCA in the UK and ESMA in the EU.

2. Issuance Regulations

Disclosure Requirements: Issuers must provide detailed information on financial health, risks, and bond terms, allowing investors to make informed decisions.

Registration Processes: Publicly offered bonds undergo rigorous registration, while private placements face lighter regulation but are limited to qualified investors.

3. Trading and Market Conduct Rules

Best Execution: Brokers and dealers are required to seek the best available price for clients.

Transparency in Pricing: Regulatory frameworks mandate transparency, especially in the OTC market, to ensure fair pricing.

4. Investor Protection Measures

Suitability Requirements: Brokers must assess whether fixed-income investments are appropriate for their clients’ risk profiles.

Anti-Fraud Protections: Regulatory bodies enforce laws against misrepresentation and insider trading in bond markets

Examples

Example 1: U.S. Treasury Bond Issuance

U.S. Treasury bonds are issued by the federal government to finance national debt and fund public projects. These bonds are sold in the primary market through auctions managed by the Treasury. Investors submit bids, and bonds are allocated based on demand and bid type (competitive or non-competitive). Once issued, these bonds trade in the secondary market, where they are bought and sold by investors, with prices influenced by interest rates and economic conditions.

Example 2: Corporate Bond Issuance

A corporation issues bonds to raise capital for expansion, acquisitions, or refinancing debt. Investment banks act as underwriters, assisting with bond pricing, marketing, and distribution. The bond’s coupon rate reflects the corporation’s credit rating and current market rates. After issuance, corporate bonds are traded in the secondary market, often through over-the-counter (OTC) networks, allowing investors to buy and sell them based on company performance and market conditions.

Example 3: Municipal Bond Trading

Municipal bonds are issued by local governments or municipalities to fund projects like schools, roads, and hospitals. These bonds are often tax-exempt, making them attractive to individual investors. After issuance, municipal bonds trade in the secondary market, where prices are influenced by changes in interest rates, the issuing municipality's creditworthiness, and local economic conditions.

Example 4: Fixed-Income Electronic Trading Platforms

Fixed-income electronic trading platforms, such as MarketAxess and Bloomberg, allow institutional investors to trade bonds with real-time pricing and data transparency. These platforms facilitate the trading of corporate, municipal, and government bonds, enhancing market liquidity and efficiency by allowing direct transactions between buyers and sellers. Electronic platforms are becoming increasingly important for fixed-income trading as they offer reduced transaction times and improved price transparency.

Example 5: Yield Curve Strategies in Trading

Traders in fixed-income markets often use strategies based on the shape of the yield curve. For example, if the yield curve is upward-sloping, traders might buy longer-term bonds expecting higher returns over time. In contrast, if the curve is flat or inverted, they may focus on shorter-term bonds. Yield curve analysis helps traders anticipate interest rate movements and make informed decisions, influencing both primary issuance terms and secondary market trading strategies.

Practice Questions

Question 1

What is the primary purpose of the primary market in fixed-income issuance?

A) To facilitate the resale of bonds between investors

B) To provide a platform for issuing new securities to raise capital

C) To establish a centralized exchange for bond trading

D) To determine bond ratings for investors

Answer: B) To provide a platform for issuing new securities to raise capital

Explanation: The primary market is where new fixed-income securities are issued directly by the issuer, such as a corporation or government, to raise funds. The secondary market, on the other hand, is where bonds are traded between investors after issuance.

Question 2

Which of the following is a characteristic of the secondary market for fixed-income securities?

A) Bonds are initially sold to investors directly by issuers

B) It provides liquidity by allowing bonds to be traded after issuance

C) Bonds are only available to institutional investors

D) It is regulated exclusively by the issuer’s internal policies

Answer: B) It provides liquidity by allowing bonds to be traded after issuance

Explanation: The secondary market allows investors to buy and sell bonds after the initial issuance, providing liquidity to the market. This market enables investors to adjust their holdings, trade bonds, and helps with price discovery based on current demand and supply.

Question 3

Which of the following roles do investment banks play in the fixed-income issuance process?

A) They set interest rates independently for each bond issued

B) They act as intermediaries, underwriting and distributing new bond issuances

C) They exclusively handle all secondary market trades of fixed-income securities

D) They regulate fixed-income markets to ensure compliance

Answer: B) They act as intermediaries, underwriting and distributing new bond issuances

Explanation: Investment banks play a crucial role in the issuance process by underwriting and distributing bonds, assisting issuers in setting appropriate terms and marketing the bonds to investors. They help determine the bond's pricing based on market conditions and demand, but they do not control interest rates independently or handle all secondary market trades