Fixed-Income Markets for Corporate Issuers

Preparing for the CFA Exam requires a solid grasp of Fixed-Income Markets for Corporate Issuers, a vital aspect of the Fixed-Income Investments foundation. Mastery of corporate debt instruments, yield analysis, credit risk, and bond valuation is crucial. This knowledge is essential for evaluating corporate financing strategies and understanding market dynamics, key to achieving high CFA scores.

Learning Objective

In studying “Fixed-Income Markets for Corporate Issuers” for the CFA Exam, you should aim to understand the characteristics and types of corporate bonds, including investment-grade and high-yield debt. Analyze the yield structure and various risks associated with corporate fixed-income securities, such as credit risk, interest rate risk, and liquidity risk. Evaluate techniques for assessing a company’s creditworthiness and the impact of market conditions on corporate bond pricing and yields. Additionally, explore bond covenants, issuance structures, and the role of credit ratings. Apply these concepts to analyze corporate financing decisions and assess market behavior in CFA practice scenarios

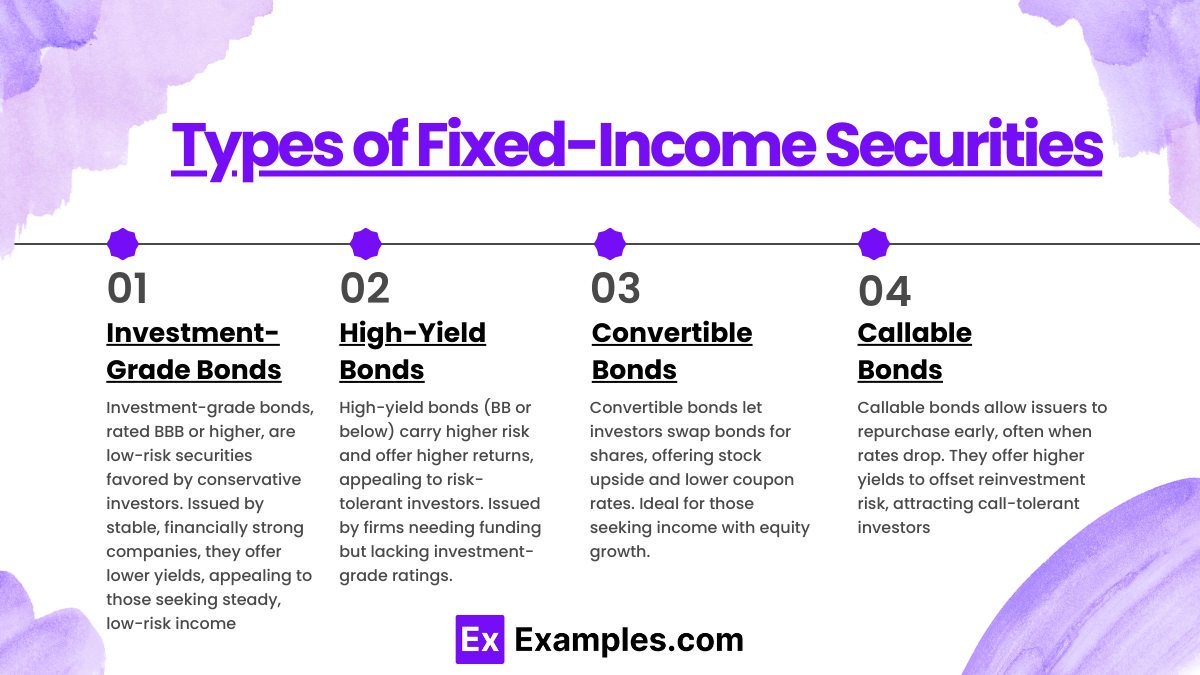

Types of Corporate Bonds

1. Investment-Grade Bonds

- Definition and Characteristics: Investment-grade bonds are issued by companies with high credit ratings, typically rated BBB or higher by agencies like S&P and Moody’s. They have a lower risk of default, which makes them more appealing to conservative investors.

- Issuer Profile: These bonds are generally issued by well-established companies with stable cash flows and a strong financial position.

- Risk-Return Profile: Investment-grade bonds offer lower yields compared to high-yield bonds, reflecting their lower risk level. They are suitable for investors seeking steady income with minimal credit risk.

2. High-Yield (Junk) Bonds

- Definition and Characteristics: High-yield bonds, often called junk bonds, are issued by companies with lower credit ratings (BB or below). These bonds carry a higher risk of default due to the issuer’s weaker financial position.

- Higher Yield Potential: To compensate for the increased risk, high-yield bonds offer higher interest rates. This appeals to investors looking for higher returns and willing to accept additional risk.

- Issuer Profile: Typically issued by companies with significant growth potential or those undergoing financial restructuring, high-yield bonds provide funding options for companies that may not qualify for investment-grade ratings.

3. Convertible Bonds

- Convertible Feature: Convertible bonds allow investors to convert the bond into a predetermined number of the issuer’s common shares, typically at a set price. This feature provides potential upside if the company’s stock price appreciates.

- Risk-Return Trade-Off: Convertibles offer a lower coupon rate than non-convertible bonds of similar credit quality, as investors gain the option to benefit from equity participation.

- Appeal to Investors: Convertible bonds appeal to investors seeking fixed income with the potential for equity-like returns, making them popular in volatile markets.

4. Callable Bonds

- Callable Feature: Callable bonds allow the issuer to repurchase the bond at a predetermined price before maturity. Issuers typically call bonds when interest rates decline, enabling them to refinance at lower rates.

- Impact on Investors: Callable bonds carry reinvestment risk for investors, as they may need to reinvest the proceeds at lower rates if the bond is called.

- Yield Advantage: To compensate for the call risk, callable bonds usually offer a higher yield compared to non-callable bonds of similar credit quality, attracting investors willing to accept potential call risk

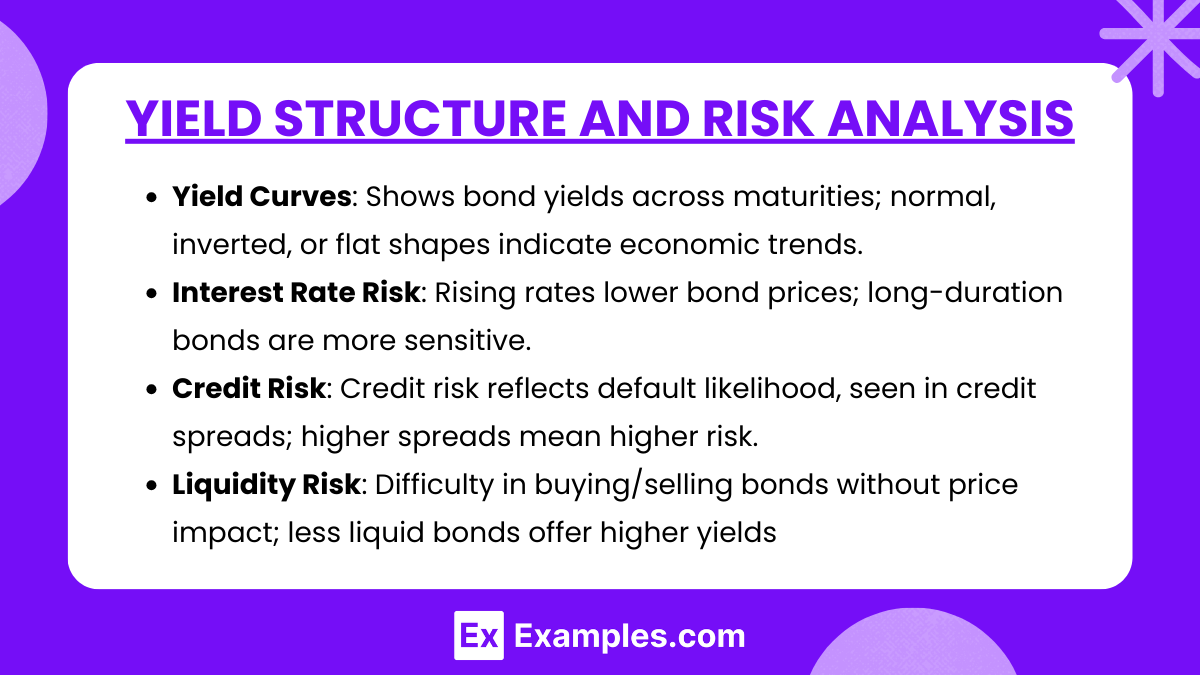

Yield Structure and Risk Analysis

1. Yield Curves

- Definition and Types: The yield curve represents the relationship between bond yields and their maturities. Key types include the normal (upward-sloping), inverted (downward-sloping), and flat yield curves.

- Implications for Corporate Bonds: The shape of the yield curve affects corporate bond pricing and investor sentiment. For example, a steep yield curve indicates higher expected inflation or economic growth, which may lead to higher yields on long-term corporate bonds.

- Use in Forecasting: The yield curve is often used to gauge economic conditions. An inverted yield curve, where short-term rates are higher than long-term rates, can signal a potential economic downturn, influencing corporate bond yields and investor demand.

2. Interest Rate Risk

- Impact on Bond Prices: When interest rates rise, bond prices generally fall, as newly issued bonds offer higher yields, making existing bonds with lower coupons less attractive. This inverse relationship is a fundamental aspect of bond valuation.

- Duration and Sensitivity: Duration measures a bond’s sensitivity to interest rate changes. Bonds with longer durations (e.g., long-term corporate bonds) are more sensitive to interest rate movements, while shorter-duration bonds experience less price volatility.

- Managing Interest Rate Risk: Investors may manage interest rate risk by choosing bonds with appropriate duration based on their interest rate outlook. For instance, they may favor shorter-duration bonds in a rising rate environment to mitigate price decline.

3. Credit Risk Assessment

- Default Risk: Credit risk in corporate bonds primarily revolves around the risk of default, where the issuer fails to meet interest or principal payments. Credit ratings from agencies like Moody’s and S&P help assess this risk.

- Credit Spread: The credit spread is the difference in yield between a corporate bond and a risk-free government bond of similar maturity. Higher spreads indicate greater credit risk. For instance, high-yield bonds generally have wider spreads than investment-grade bonds.

- Factors Influencing Credit Risk: Credit risk assessment considers factors such as the issuer’s financial health, cash flow stability, industry risks, and macroeconomic conditions. Companies with stable cash flows and low debt levels typically have lower credit risk and narrower spreads.

4. Liquidity Risk

- Definition: Liquidity risk in corporate bonds refers to the risk of not being able to buy or sell the bond without significantly impacting its price, especially during market stress.

- Influence on Yield: Less liquid bonds tend to offer higher yields to compensate investors for the added risk of holding a bond that may be difficult to sell quickly.

- Key Considerations: Bond liquidity can vary by issuer, bond issue size, and market conditions. For example, investment-grade corporate bonds from well-known companies are generally more liquid, while high-yield or small-issue bonds may have higher liquidity risk.

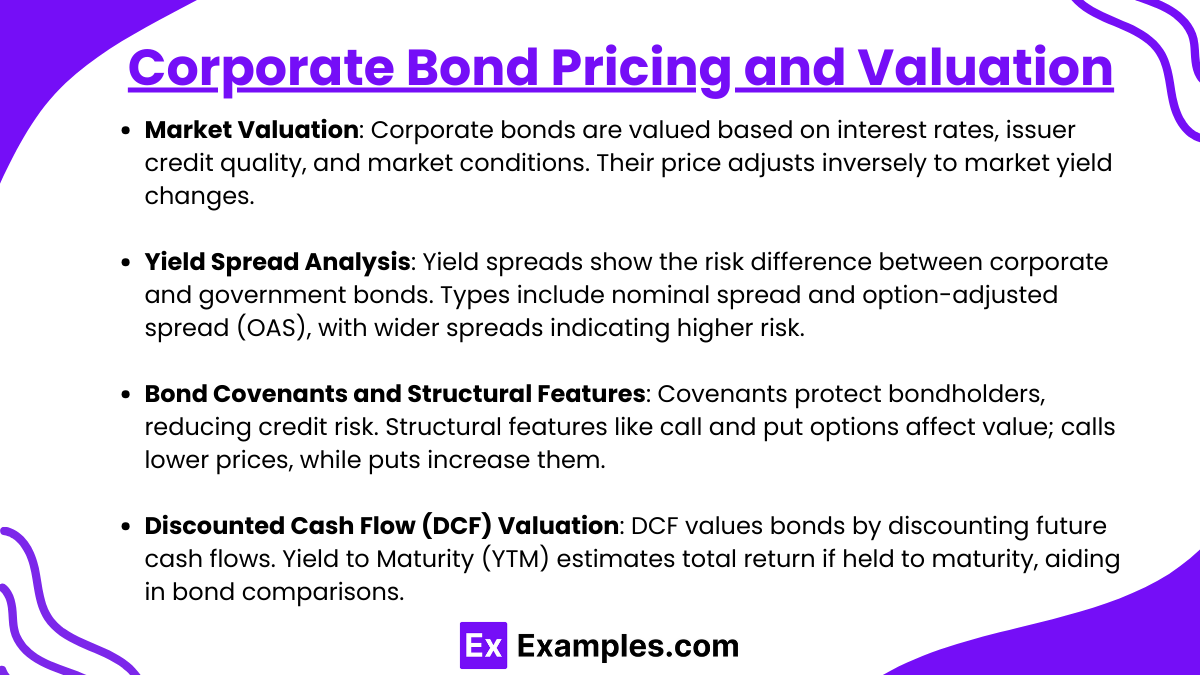

Corporate Bond Pricing and Valuation

- Market Valuation

- Corporate bonds are valued based on prevailing market interest rates, the issuer’s credit quality, and overall market conditions. Market valuation relies on the bond’s expected cash flows (coupon payments and principal repayment) discounted at an appropriate discount rate, typically the yield that reflects the bond’s risk level.

- Price-Yield Relationship: As market yields fluctuate, the bond price adjusts inversely. If yields rise, bond prices decrease; if yields fall, bond prices increase. This relationship is critical for understanding bond price volatility.

- Yield Spread Analysis

- Yield spreads are the differences in yields between corporate bonds and government securities of similar maturity. The spread reflects the credit and liquidity risks of the corporate bond relative to a government bond.

- Types of Spreads: The main types include the nominal spread, which is the simple difference in yields, and the option-adjusted spread (OAS), which accounts for embedded options, like calls or puts, in the bond. Wider spreads indicate higher risk levels, while narrower spreads suggest lower relative risk.

- Bond Covenants and Structural Features

- Bond covenants are provisions in the bond contract that protect the interests of bondholders. These can be affirmative covenants (actions the issuer agrees to take) or restrictive covenants (limitations placed on the issuer’s actions). Covenants impact bond valuation by reducing credit risk, which can lead to narrower spreads.

- Embedded Options: Bonds may have structural features such as call or put options. Callable bonds allow issuers to redeem before maturity, generally lowering bond prices due to the reinvestment risk for investors. Putable bonds, allowing investors to sell back to the issuer, may increase the bond’s value since they provide an exit option.

- Discounted Cash Flow (DCF) Valuation

- DCF is a common valuation approach for corporate bonds, involving the discounting of future cash flows (coupon payments and principal) to the present at a discount rate reflecting the bond’s risk profile.

- Present Value of Cash Flows: The bond’s value is calculated as the sum of the present values of its expected cash flows. A higher discount rate (yield) results in a lower bond price and vice versa.

- Yield to Maturity (YTM): YTM is the total return anticipated on a bond if held to maturity, assuming all payments are made as scheduled. It serves as the internal rate of return (IRR) for the bond, helping investors compare potential returns across bonds with different structures and maturities.

Credit Ratings and Creditworthiness Evaluation

- Credit Rating Agencies

- Credit rating agencies, such as Standard & Poor’s (S&P), Moody’s, and Fitch, assess the creditworthiness of corporate bond issuers and assign ratings that reflect their likelihood of meeting debt obligations. These ratings range from high-grade (AAA or Aaa) to speculative or junk status (BB or Ba and below).

- Role in Market Perception: Credit ratings provide investors with insights into the issuer’s financial stability and risk profile, influencing the demand and yield of corporate bonds. Higher ratings typically lead to lower yields due to perceived lower risk, while lower ratings command higher yields.

- Rating Criteria

- Rating agencies use a range of quantitative and qualitative factors to assess creditworthiness. Key factors include the issuer’s financial position, cash flow stability, capital structure, and competitive position within the industry.

- Industry-Specific Considerations: Certain industries have unique risk factors that impact credit ratings. For instance, cyclical industries may see ratings fluctuate with economic cycles, while regulated industries, like utilities, may have more stable ratings due to predictable cash flows.

- Financial Ratios and Analysis

- Financial ratios are essential in evaluating an issuer’s ability to meet its debt obligations. Commonly analyzed ratios include:

- Liquidity Ratios: Measures such as the current ratio and quick ratio assess the issuer’s ability to cover short-term liabilities with liquid assets.

- Leverage Ratios: Ratios like the debt-to-equity ratio and debt-to-assets ratio indicate the extent of a company’s reliance on borrowed funds.

- Coverage Ratios: The interest coverage ratio (EBIT/interest expense) shows how comfortably a company can service its debt, with higher ratios indicating stronger creditworthiness.

- Financial ratios are essential in evaluating an issuer’s ability to meet its debt obligations. Commonly analyzed ratios include:

- Credit Spread Analysis

- The credit spread is the difference between the yield on a corporate bond and a risk-free government bond of similar maturity. It reflects the additional risk premium required by investors to compensate for credit risk.

- Impact of Rating Changes on Spreads: A downgrade in credit rating often results in a wider spread, as investors demand a higher yield to compensate for increased risk. Conversely, upgrades can narrow the spread, lowering the issuer’s borrowing costs.

Examples

Example 1

A technology company with a high credit rating issues a 10-year investment-grade bond with a fixed coupon rate of 4%. Given its strong financial position, the company receives a high rating of A+ from S&P, resulting in a relatively low yield. This makes the bond attractive to conservative investors seeking steady income with minimal credit risk. The stable rating and predictable cash flows make it a core addition to many institutional portfolios.

Example 2

A telecommunications firm issues a 7-year high-yield (junk) bond with a 7% coupon rate. Due to its recent expansion and high debt levels, the company’s bonds are rated BB, which places them in the speculative category. The high yield compensates investors for the increased credit risk, appealing to those with a higher risk tolerance who seek greater returns. The company’s credit spread relative to government bonds reflects its speculative grade, as investors require a premium for the default risk.

Example 3

A pharmaceutical corporation issues convertible bonds, allowing investors to convert the bonds into shares if the company’s stock price reaches a certain level. The bonds have a lower coupon rate of 3%, reflecting the added equity option for investors. These bonds are appealing to investors looking for a combination of fixed-income security and potential equity upside, especially if they believe the company’s stock price will rise significantly. The convertible feature creates potential future dilution for the company but provides flexibility in attracting diverse investors.

Example 4

An energy company issues callable bonds with a 5% coupon rate, which the company can redeem after five years if interest rates fall. Investors are compensated for this call risk through a slightly higher yield than similar non-callable bonds. This feature provides the issuer with refinancing flexibility, enabling them to reduce debt costs if market rates decline. However, it creates reinvestment risk for investors, who may have to accept lower yields if the bond is called and they reinvest in a lower-rate environment.

Example 5

A large retail company’s bond rating is downgraded from BBB to BB following a period of declining sales and increased competition. This downgrade moves the bond from investment-grade to high-yield status, leading to a wider credit spread and higher yield as investors demand greater compensation for the increased risk. The downgrade affects the company’s future borrowing costs and could deter risk-averse investors, while attracting those looking to benefit from potential price recovery if the company’s financial position improves

Practice Questions

Question 1

Which of the following features typically results in a corporate bond offering a higher yield to compensate investors?

A) Investment-grade rating

B) Convertible feature

C) Callability feature

D) Government backing

Answer: C) Callability feature

Explanation: Callable bonds give the issuer the right to redeem the bond before its maturity, usually when interest rates decline. This feature introduces reinvestment risk for investors, as they may need to reinvest the returned principal at lower rates if the bond is called. To compensate for this risk, callable bonds generally offer a higher yield than similar non-callable bonds. Investment-grade ratings and government backing reduce credit risk, leading to lower yields, while a convertible feature often results in lower yields due to the potential for equity upside.

Question 2

A bond issued by a corporation that is rated BB by S&P and has a high coupon rate is classified as:

A) Investment-grade bond

B) High-yield (junk) bond

C) Government bond

D) Convertible bond

Answer: B) High-yield (junk) bond

Explanation: A bond rated BB by S&P falls below the investment-grade threshold, classifying it as a high-yield, or “junk,” bond. These bonds are typically issued by companies with higher credit risk and offer higher coupon rates to attract investors who are willing to take on additional risk for potentially greater returns. Investment-grade bonds have ratings of BBB or higher, while government bonds are issued by governments, not corporations. Convertible bonds may have high or low ratings depending on the issuer but are primarily characterized by their convertibility to equity.

Question 3

If a company issues a bond that allows the investor to convert it into a predetermined number of the company’s common shares, this bond is known as a:

A) Callable bond

B) Convertible bond

C) Putable bond

D) Zero-coupon bond

Answer: B) Convertible bond

Explanation: A convertible bond provides investors with the option to convert the bond into a set number of the issuer’s common shares at a specified price, offering potential equity upside if the company’s stock price appreciates. Callable bonds allow the issuer to redeem the bond before maturity, while putable bonds allow the investor to sell the bond back to the issuer. A zero-coupon bond does not offer regular interest payments and is issued at a discount to par value, with repayment at face value at maturity