Fixed-Income Securitization

Preparing for the CFA Exam necessitates a solid grasp of Fixed-Income Securitization, a vital part of the Fixed Income topic. Mastery of securitization processes, asset-backed securities, and risk considerations is essential. This knowledge enables insights into bond markets, credit risk assessment, and structured finance, crucial for achieving a high CFA score

Learning Objective

In studying "Fixed-Income Securitization" for the CFA Exam, you should aim to understand the structure and function of securitized financial instruments, including mortgage-backed securities, asset-backed securities, and collateralized debt obligations. Analyze the benefits and risks associated with securitization, particularly in transforming illiquid assets into tradable securities. Evaluate the securitization process, from asset pooling to tranche structuring, and how credit enhancement and risk mitigation are applied. Additionally, explore the regulatory framework governing securitized assets and the impact of securitization on financial markets. Apply this understanding to evaluate case studies and structured finance problems typical of CFA exam scenarios.

Introduction to Securitization

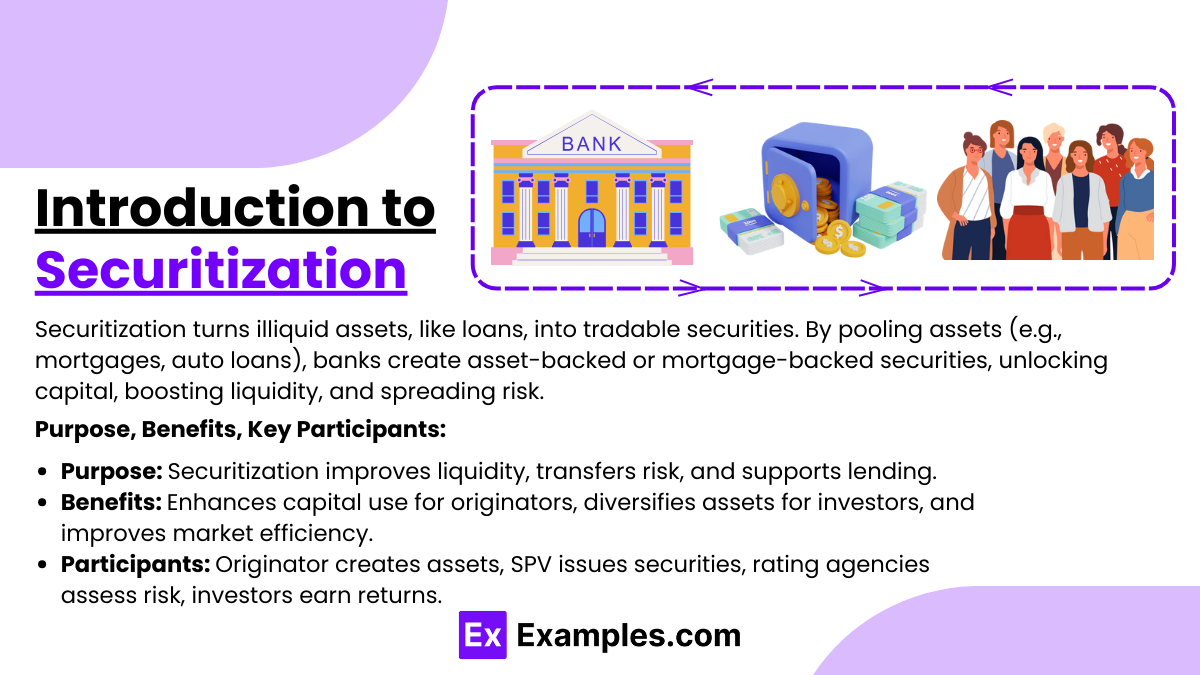

Securitization is a financial process that transforms illiquid assets, such as loans or receivables, into tradable securities, making them accessible to a broader range of investors. This process involves pooling these financial assets, such as mortgages, auto loans, credit card receivables, or other cash-generating assets, and then selling them as asset-backed securities (ABS) or mortgage-backed securities (MBS) to investors. By converting these assets into securities, originators (like banks or financial institutions) can unlock capital, improve liquidity, and redistribute risk.

Purpose of Securitization: The primary goal of securitization is to enhance liquidity and access to capital. Through securitization, financial institutions can transfer the risk associated with the underlying assets to investors, effectively reducing the risk exposure on their balance sheets. This process also allows institutions to raise funds to support additional lending activities, promoting credit growth.

Benefits of Securitization: Securitization provides multiple benefits for different participants. For originators, it enables efficient capital utilization and risk management. For investors, it offers access to a diversified portfolio of assets with varying levels of risk and return. Additionally, securitization can contribute to market efficiency by making illiquid assets more accessible and tradable, thus promoting better price discovery and risk allocation in financial markets.

Key Participants in the Securitization Process: Several key players are involved in securitization. The originator creates the underlying assets and initiates the securitization. The special purpose vehicle (SPV) is established to hold the assets and issue securities, shielding the assets from the originator’s liabilities. Rating agencies evaluate the securities' risk to guide potential investors. Finally, investors purchase the issued securities, earning returns based on the cash flows generated by the pooled assets.

Structure and Types of Securitized Products

The structure of securitized products is based on transforming pools of underlying assets into securities that investors can purchase. This process involves creating a legal entity, known as a special purpose vehicle (SPV), which isolates the assets from the originator’s balance sheet, ensuring that investors are protected from the originator's credit risk. The SPV issues securities backed by the pooled assets, which are then divided into tranches with varying levels of risk and return to meet diverse investor preferences. Each tranche has its own cash flow priority and risk exposure, typically categorized as senior, mezzanine, or junior.

The types of securitized products primarily include Mortgage-Backed Securities (MBS), Asset-Backed Securities (ABS), and Collateralized Debt Obligations (CDOs). Each type has unique features based on the underlying assets, cash flow structure, and risk profile.

1. Mortgage-Backed Securities (MBS):

Residential MBS (RMBS): These are securities backed by pools of residential mortgages, such as home loans. Investors receive cash flows based on homeowners' mortgage payments, including principal and interest.

Commercial MBS (CMBS): CMBS are backed by commercial real estate mortgages on properties like office buildings, shopping centers, or hotels. They generally have more complex structures due to the varied nature of commercial properties and often involve additional layers of risk and credit enhancement.

Prepayment Risk and Interest Rate Sensitivity: MBS are particularly sensitive to prepayment risk, as borrowers may pay off loans early, impacting cash flows. This is often influenced by interest rate changes, making MBS complex and requiring detailed analysis of market conditions.

2. Asset-Backed Securities (ABS):

Types of Assets: ABS are backed by various consumer and business-related assets such as auto loans, credit card receivables, student loans, and equipment leases. Each type of ABS is structured to align with the cash flow characteristics and risk profile of the underlying assets.

Cash Flow and Risk Diversification: Since ABS are backed by a pool of assets, the risk of individual asset default is minimized. Investors receive cash flows generated by the asset pool, typically structured to offer regular payments based on the assets’ performance.

Credit Enhancement: ABS structures often include credit enhancements, such as overcollateralization or reserve accounts, to protect investors from default risk. This added security can make ABS attractive to risk-sensitive investors.

3. Collateralized Debt Obligations (CDOs):

Structure of CDOs: CDOs are backed by a diversified pool of assets, such as loans, bonds, or other debt instruments, rather than a single asset type. They are commonly divided into tranches, which provide varying levels of risk and return, ranging from senior tranches with low risk to equity tranches with higher risk and potential returns.

Collateralized Loan Obligations (CLOs): A specific type of CDO, CLOs are backed primarily by pools of corporate loans, often issued to companies with lower credit ratings. CLOs provide investors access to high-yield debt instruments while mitigating risk through diversification and tranching.

Investor Appeal and Complexity: CDOs offer high yield potential but require in-depth analysis due to their complex structures. These products were involved in the 2008 financial crisis, highlighting the importance of understanding underlying risks and market impacts.

Key Differences Among Securitized Products: Each securitized product type has unique characteristics that cater to various investor needs:

MBS typically appeals to investors seeking exposure to the real estate market, although these securities carry interest rate and prepayment risks.

ABS provides diversification and risk management, making it suitable for those looking to invest in consumer or business-related debt.

CDOs cater to investors seeking higher yields with an understanding of structured products, often involving more sophisticated risk assessment and management

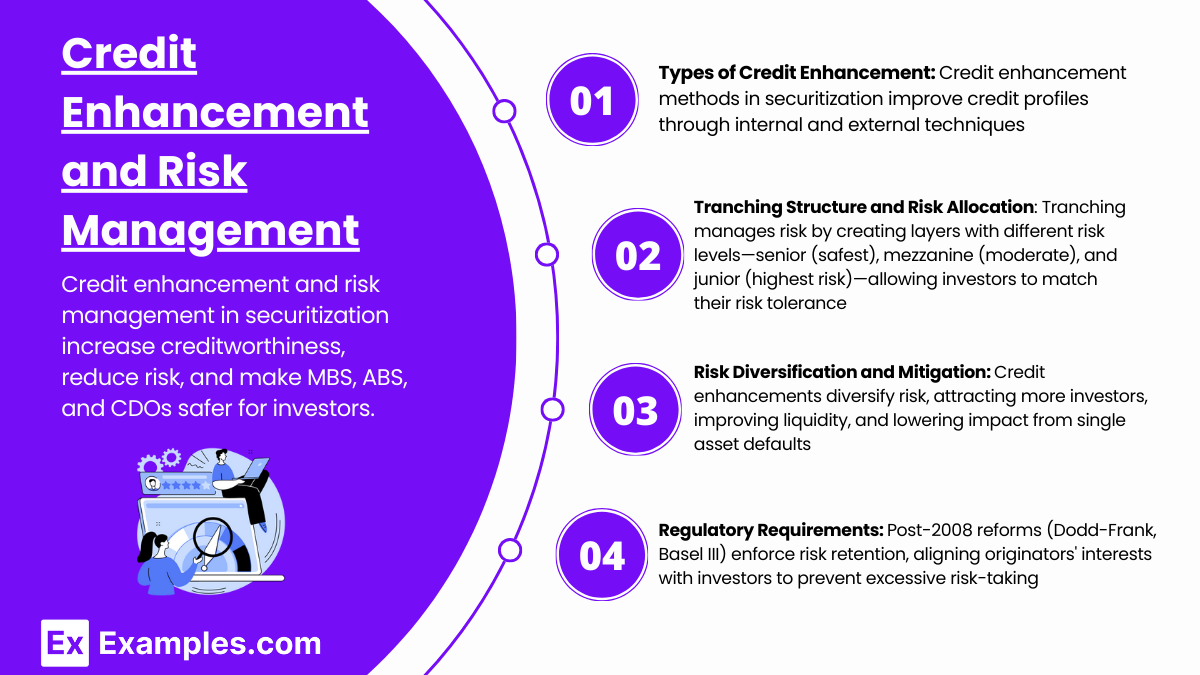

Credit Enhancement and Risk Management

Credit enhancement and risk management are key components in the securitization process, designed to increase the creditworthiness of securitized products and protect investors from default risk. Through various forms of credit enhancement, securitization structures can reduce risk, improve credit ratings, and make these products more appealing to investors. These mechanisms are particularly important in complex products like mortgage-backed securities (MBS), asset-backed securities (ABS), and collateralized debt obligations (CDOs).

Types of Credit Enhancement:

Credit enhancement techniques are generally classified into internal and external methods. Each approach offers distinct ways to improve the credit profile of securitized assets.

Internal Credit Enhancement:

Overcollateralization: In this approach, the value of the underlying asset pool exceeds the face value of the securities issued. This extra collateral serves as a cushion to cover potential losses, increasing investor protection.

Tranching: Securitized products are divided into multiple tranches with different risk and return profiles. Senior tranches have the first claim on cash flows, making them less risky, while mezzanine and junior tranches absorb more risk. This layering of risk helps distribute potential losses across different tranches.

Reserve Accounts (or Cash Reserve Funds): A portion of the cash flow from the underlying assets is set aside in a reserve account to cover future losses. This reserve acts as a buffer, reducing the likelihood of default on payments to investors.

External Credit Enhancement:

Third-Party Guarantees and Insurance: A guarantor, such as a bond insurer or a bank, may provide a guarantee to cover payments if the underlying assets default. This can significantly reduce risk for investors, as the insurer or guarantor bears the default risk.

Letters of Credit: A letter of credit from a financial institution provides a promise to cover potential shortfalls in the asset pool, thereby enhancing the security's credit quality.

Tranching Structure and Risk Allocation:

In securitization, tranching is a powerful tool for managing risk and enhancing credit. The tranches are divided into senior, mezzanine, and junior (or equity) layers, each with distinct risk and cash flow priorities:

Senior Tranche: This tranche has the highest priority for receiving payments and is considered the safest. Because it is backed by additional credit enhancements, it typically receives the highest credit rating.

Mezzanine Tranche: This middle layer bears more risk than the senior tranche and thus offers a higher yield. However, it only receives payments after senior obligations are met.

Junior (Equity) Tranche: This tranche absorbs the most risk and is the last to receive payments, often carrying no credit rating. It provides the highest potential return to compensate for the increased risk exposure.

This layered structure allows investors to choose tranches that match their risk tolerance and investment objectives, creating a diverse market for securitized products.

Importance of Risk Diversification and Mitigation:

Credit enhancement is a form of risk management that allows originators to reduce exposure on their balance sheets while providing investors with structured products suited to varying risk appetites. By diversifying underlying assets across a range of securities, securitized products reduce the impact of any single asset’s default. Furthermore, these enhancements can attract a wider pool of investors, leading to increased liquidity and market efficiency.

Regulatory Requirements and Risk Factors:

Following the 2008 financial crisis, regulatory oversight increased significantly to prevent excessive risk-taking in securitization. Dodd-Frank Act in the U.S. and Basel III globally introduced measures such as risk retention rules, requiring originators to retain a portion of the risk to align interests with investors. This regulatory framework helps mitigate moral hazard and ensures that originators maintain a stake in the quality of the assets they securitize.

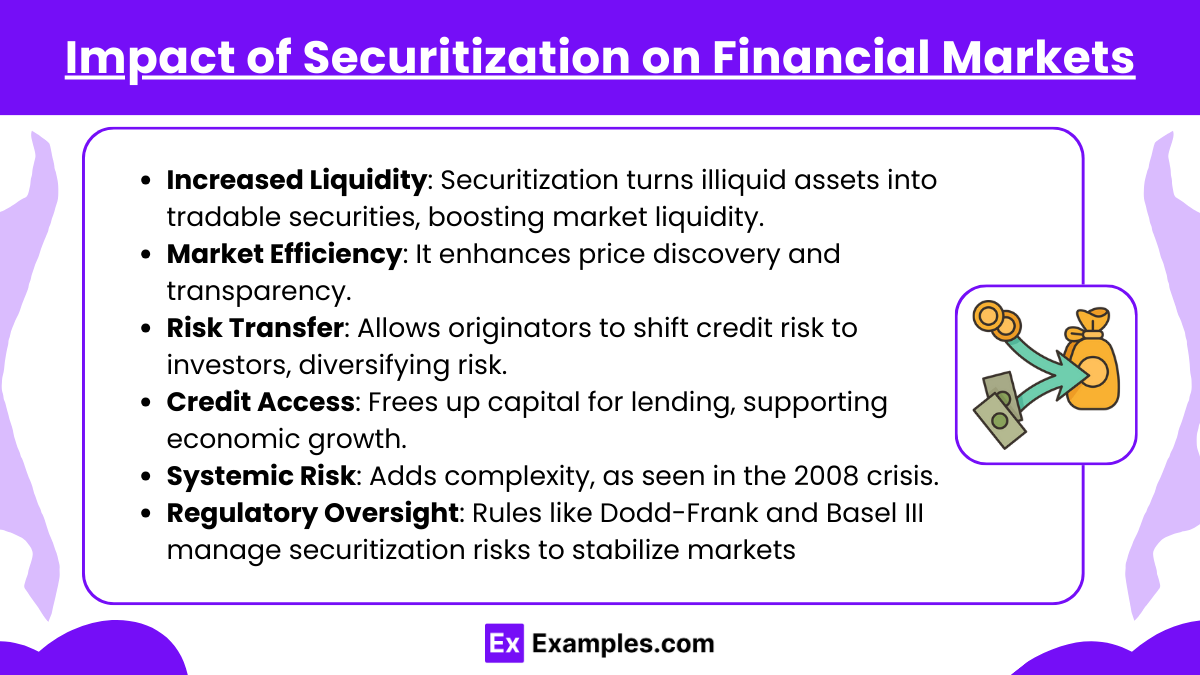

Impact of Securitization on Financial Markets

Increased Liquidity: Securitization transforms illiquid assets into tradable securities, enhancing overall market liquidity and enabling more active trading.

Market Efficiency: By creating standardized and tradable instruments, securitization improves price discovery and allows investors to assess asset values more transparently.

Risk Transfer and Diversification: Securitization allows originators to transfer credit risk to investors, diversifying risk across different market participants.

Credit Availability and Economic Growth: It frees up capital for lenders, promoting additional lending and contributing to economic growth through greater credit access.

Potential for Systemic Risk: Securitization can introduce complexity and interconnected risks, as seen in the 2008 financial crisis, where excessive risk in mortgage-backed securities affected global markets.

Regulatory Implications: Increased regulatory oversight, such as the Dodd-Frank Act and Basel III, aims to manage risks associated with securitization and prevent market instability

Examples

Example 1

A bank pools residential mortgages and sells them as Mortgage-Backed Securities (MBS) to investors. The bank receives funds from the sale, enabling it to make additional loans, while investors receive cash flows based on the mortgage payments from homeowners.

Example 2

An auto loan company securitizes its portfolio of car loans by creating Asset-Backed Securities (ABS). Investors in these securities receive interest payments derived from the monthly car loan payments, with the risk spread across the diversified pool of loans.

Example 3

A financial institution bundles corporate loans into Collateralized Loan Obligations (CLOs) and issues them in tranches. Senior tranches receive priority in payments, making them lower-risk, while junior tranches have higher risk but offer greater return potential.

Example 4

A credit card company pools credit card receivables to create ABS. The receivables' future cash flows, generated by credit card payments, are passed on to investors, with additional credit enhancement provided through reserve funds to protect against potential defaults.

Example 5

A commercial bank securitizes loans issued to small businesses by structuring them into a Collateralized Debt Obligation (CDO). This allows the bank to distribute credit risk to investors, diversify its portfolio, and raise capital for new lending activities

Practice Questions

Question 1

Which of the following best describes the purpose of securitization in the fixed-income market?

A) To increase a bank's loan portfolio size

B) To transform illiquid assets into tradable securities

C) To directly increase a bank’s interest income

D) To reduce investor risk through diversification

Answer: B

Explanation: Securitization is primarily used to convert illiquid assets, like loans or receivables, into securities that can be sold and traded in financial markets. This process enables greater liquidity and accessibility for these assets.

Question 2

In a securitization structure, what is the role of a Special Purpose Vehicle (SPV)?

A) To manage the cash flows from the securitized assets

B) To increase the credit rating of the securitized product

C) To isolate the assets from the originator’s balance sheet

D) To guarantee payment to investors

Answer: C

Explanation: An SPV is created to hold the securitized assets separately from the originator, ensuring that these assets are isolated and that investors are protected from the originator's credit risk. This isolation is essential for the securitization process.

Question 3

Which of the following is a key difference between Asset-Backed Securities (ABS) and Mortgage-Backed Securities (MBS)?

A) ABS are backed by residential mortgages, while MBS are backed by credit card receivables.

B) ABS are generally backed by non-mortgage consumer loans, while MBS are specifically backed by pools of mortgages.

C) ABS typically carry higher credit ratings than MBS.

D) ABS are only offered to institutional investors, whereas MBS are available to retail investors.

Answer: B

Explanation: ABS are backed by consumer loans such as auto loans, credit card receivables, and other non-mortgage debt, while MBS are specifically backed by residential or commercial mortgages. This distinction is foundational in fixed-income securitization