Introduction to Commodities & Commodity Derivatives

Commodities are tangible assets like metals, energy, and agricultural products, serving as a core part of alternative investments. Commodity derivatives, such as futures, options, and swaps, allow investors to gain exposure to commodity price movements without holding the physical assets. These instruments enable portfolio diversification, inflation hedging, and effective risk management. Commodities are often volatile, driven by factors like supply and demand shifts, economic conditions, and geopolitical events, making them unique compared to traditional securities like stocks and bonds in investment portfolios.

Learning Objectives

In studying “Alternative Investments: Introduction to Commodities & Commodity Derivatives” for the CFA Exam, you should learn to understand the unique characteristics and categories of commodities, including metals, energy, agriculture, and livestock. Analyze how commodity derivatives, such as futures, options, and swaps, are used for hedging, speculation, and price discovery. Evaluate key concepts like contango, backwardation, and basis risk, and their impact on pricing. Additionally, explore the role of commodities as a diversification tool and inflation hedge within portfolios, and apply your understanding to assess the risks, return drivers, and investment vehicles involved in commodity markets.

1. Understanding Commodities and Their Unique Characteristics

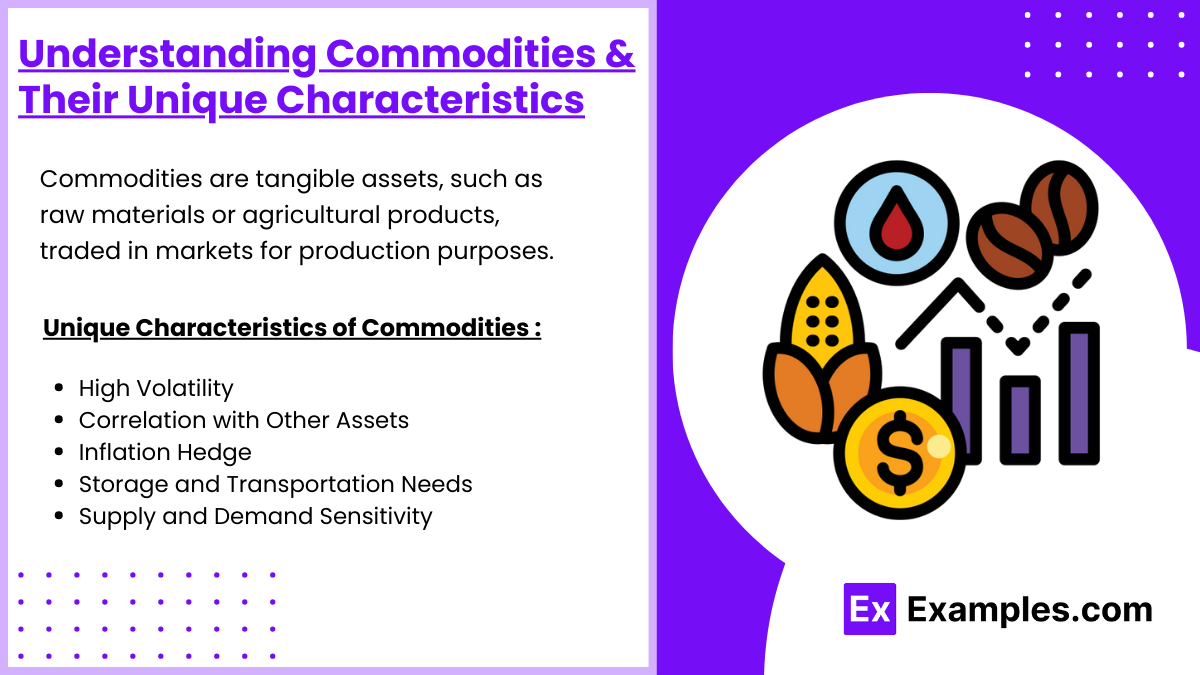

Commodities are raw materials or primary agricultural products that can be bought, sold, and traded. Unlike traditional financial assets like stocks and bonds, commodities are physical, tangible goods used primarily in production or consumption.

Unique Characteristics of Commodities

- High Volatility: Commodity prices can fluctuate sharply due to supply and demand dynamics, weather events, geopolitical tensions, and production disruptions. This volatility makes commodities both risky and potentially rewarding investments.

- Correlation with Other Assets: Commodities generally exhibit low or even negative correlation with traditional financial assets like stocks and bonds. This makes them attractive for portfolio diversification, as they can help reduce overall risk.

- Inflation Hedge: Commodities often rise in value during inflationary periods. As the cost of goods and services increases, commodity prices tend to follow suit, which can help preserve purchasing power.

- Storage and Transportation Needs: Unlike financial assets, commodities require physical storage and transportation. This adds to their carrying costs and impacts futures pricing, particularly for physical commodities that are costly to store (e.g., oil or grains).

- Supply and Demand Sensitivity: Commodities are deeply influenced by supply chain constraints and demand cycles. For example, energy demand can surge during winter, increasing prices for heating oil. Similarly, agricultural commodities may see demand fluctuations based on harvest cycles.

2. Commodity Derivatives: Overview and Functions

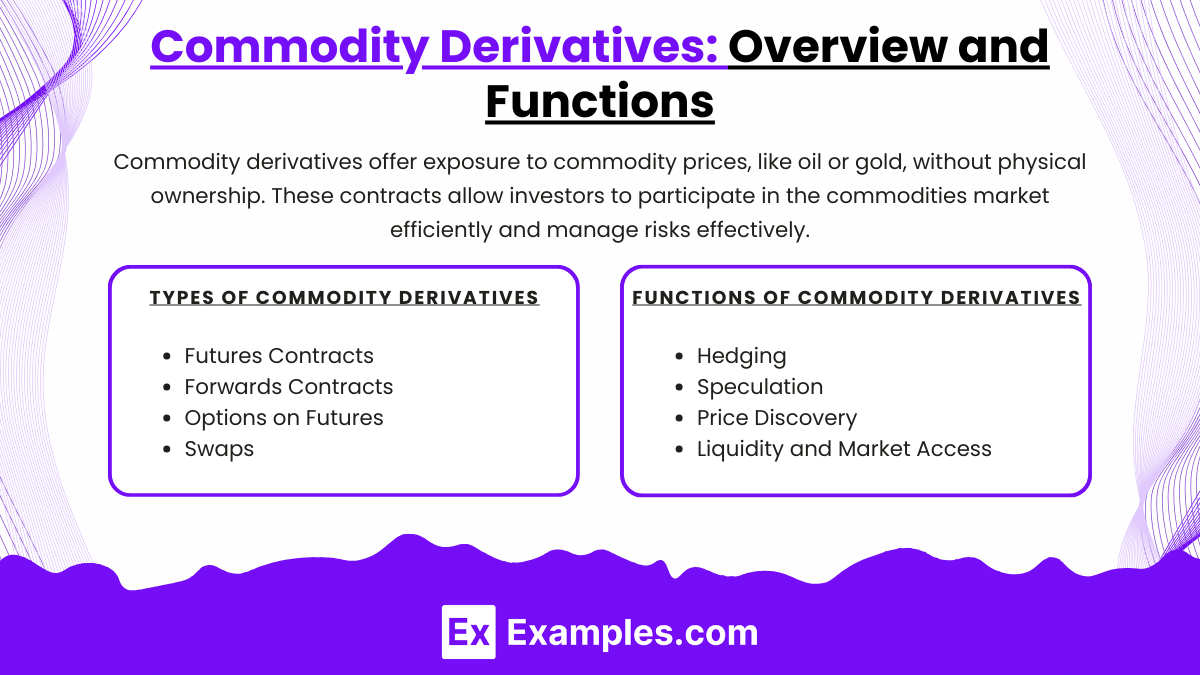

Commodity derivatives are financial instruments whose value is based on the price of an underlying commodity, such as oil, gold, or wheat. Unlike direct ownership of the physical commodity, these derivatives provide exposure to commodity prices through contracts, allowing investors to participate in the commodities market without needing to handle the physical asset.

Types of Commodity Derivatives

- Futures Contracts: A standardized agreement to buy or sell a specific quantity of a commodity at a predetermined price on a specified future date. Futures contracts are traded on exchanges, such as the CME (Chicago Mercantile Exchange), offering transparency and liquidity.

- Forwards Contracts: Similar to futures but traded over-the-counter (OTC), allowing for customization in terms of contract size, expiration date, and other specifics. Forwards carry higher counterparty risk compared to exchange-traded futures.

- Options on Futures: Provide the right, but not the obligation, to buy (call option) or sell (put option) a commodity futures contract at a predetermined strike price before or on the option’s expiration date. Options are used to limit downside risk while still offering the potential for profit if the commodity price moves favorably.

- Swaps: Typically used by institutional investors, swaps involve exchanging cash flows based on commodity price movements. For example, an airline may enter into an oil price swap to stabilize fuel costs, exchanging a fixed payment for one based on oil’s price.

Functions of Commodity Derivatives

- Hedging: Commodity derivatives allow companies and producers to protect themselves against adverse price movements. For instance, an agricultural producer can use futures contracts to lock in a sale price for their crop, reducing the risk of price drops at harvest time.

- Speculation: Traders and investors can speculate on commodity price movements by taking long (buy) or short (sell) positions in derivatives. If they anticipate rising oil prices, for example, they can buy oil futures or call options, potentially profiting if prices increase.

- Price Discovery: Futures markets provide a transparent and regulated platform where commodity prices are determined through the interaction of buyers and sellers. This results in the discovery of fair market prices, benefiting both producers and consumers by providing price benchmarks for their transactions.

- Liquidity and Market Access: Commodity derivatives provide liquidity, allowing participants to enter or exit positions easily. They also enable investors to gain exposure to commodities without needing to hold the physical assets, which may be costly or impractical to store and transport.

3. Commodity Markets and Pricing Dynamics

Commodity Markets

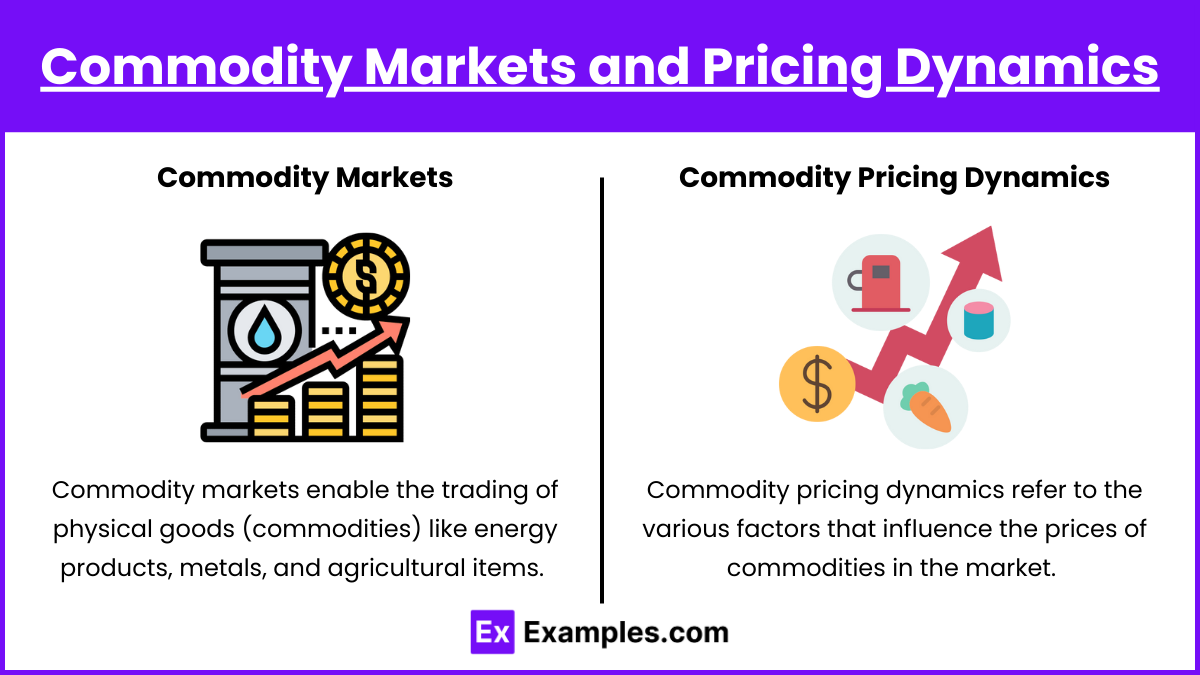

Commodity markets enable the trading of physical goods (commodities) like energy products, metals, and agricultural items. These markets are structured to facilitate both the immediate exchange of commodities (spot markets) and the setting of future prices (futures markets). Pricing in commodity markets is dynamic and influenced by a mix of supply-demand forces, geopolitical events, and economic cycles.

Key Types of Commodity Markets

- Spot Market: The spot market, also known as the cash market, involves the buying and selling of commodities for immediate delivery. Prices in the spot market reflect current supply and demand and are often volatile, responding quickly to real-time changes, such as weather events, production shifts, and geopolitical issues.

- Futures Market: The futures market allows buyers and sellers to enter contracts to trade a commodity at a predetermined price on a specified future date. These standardized contracts are traded on exchanges like the Chicago Mercantile Exchange (CME) and the London Metal Exchange (LME). Futures markets provide price stability for commodities by setting prices in advance, helping producers and consumers plan around potential price fluctuations.

- Over-the-Counter (OTC) Market: In the OTC market, commodities are traded directly between two parties without a centralized exchange. This market offers more customized contracts tailored to specific hedging needs, but it carries additional credit risk due to the lack of centralized clearing.

Commodity Pricing Dynamics

Commodity pricing dynamics refer to the various factors that influence the prices of commodities in the market. Understanding these dynamics is essential for investors and traders, as it enables them to anticipate price movements and make informed decisions. Commodity pricing is complex and impacted by multiple factors:

- Supply and Demand Fundamentals: Prices are directly influenced by the balance of supply and demand. For example, if oil production decreases due to geopolitical tensions, supply is constrained, and prices generally increase. Conversely, if there is a surplus in production or lower demand, prices may fall.

- Geopolitical Events: Commodities like oil and gas are especially sensitive to geopolitical events, such as conflicts in oil-producing regions or trade sanctions. These events can lead to sudden supply disruptions, resulting in rapid price changes.

- Economic Conditions: Economic growth drives demand for commodities, especially in industries like construction and manufacturing. When economies expand, demand for metals, energy, and other raw materials increases, driving prices higher. During economic slowdowns, demand and prices typically decrease.

4. Investment Characteristics of Commodities

- Diversification: Commodities often have low or negative correlations with traditional asset classes like stocks and bonds, making them valuable for portfolio diversification.

- Inflation Hedge: Commodities are generally viewed as effective inflation hedges since their prices tend to rise with inflation.

- Volatility: Commodity prices can be highly volatile due to factors like geopolitical events, supply chain disruptions, and weather conditions.

- Risk and Return Profile: While commodities can provide substantial returns during certain economic periods, they also carry unique risks (e.g., storage, transportation, spoilage).

5. Commodity Indices and Investment Vehicles

- Commodity Indices: Indices such as the Bloomberg Commodity Index (BCOM) or the S&P GSCI track the price performance of a basket of commodities, enabling investors to gain exposure to the commodity market.

- Exchange-Traded Funds (ETFs): Commodity ETFs provide a way for investors to gain exposure to commodities without directly investing in futures. Some ETFs invest in the physical commodity, while others invest in futures contracts.

- Mutual Funds : Commodity-focused mutual funds and managed futures funds also offer exposure, typically with professional management.

Examples

Example 1: Crude Oil Futures

Crude oil futures are standardized contracts traded on exchanges like the NYMEX, allowing investors to gain exposure to oil prices without handling the physical commodity. This derivative serves as a powerful hedging tool for companies reliant on oil prices, such as airlines, helping to stabilize costs. Investors and speculators also use crude oil futures to profit from anticipated price movements driven by global demand, geopolitical risks, and supply disruptions.

Example 2: Gold ETFs

Gold Exchange-Traded Funds (ETFs) provide a way for investors to gain exposure to gold without purchasing or storing the physical metal. Gold is often seen as a safe-haven asset and an inflation hedge, making it an attractive component for portfolio diversification. Gold ETFs, like SPDR Gold Shares (GLD), track the price of gold, allowing investors to easily buy and sell shares that reflect the performance of this precious metal on major stock exchanges.

Example 3: Agricultural Commodity Index Funds

These funds track indices that represent a basket of agricultural commodities, such as corn, wheat, soybeans, and cotton. Agricultural commodities are essential for food production, and their prices fluctuate based on factors like weather, seasonal cycles, and global supply and demand. Index funds in agriculture allow investors to diversify across various agricultural products, providing a broad-based exposure to price changes in this sector and reducing the risks associated with single-commodity investments.

Example 4: Natural Gas Options

Natural gas options provide the right, but not the obligation, to buy (call option) or sell (put option) natural gas futures at a specified price. This derivative instrument is widely used by energy companies to hedge against the volatility of natural gas prices, which are influenced by factors such as seasonal demand, production levels, and geopolitical tensions. For investors, natural gas options offer flexibility in managing risk and can be used to speculate on future price movements with limited downside.

Example 5: Commodity Swaps

Commodity swaps are OTC contracts in which two parties exchange cash flows based on the price movements of a specific commodity, such as oil, copper, or grain. Commonly used by large corporations and financial institutions, commodity swaps help hedge against adverse price changes in underlying commodities, often aligning with production or consumption needs. For example, an airline might enter a swap to manage exposure to fluctuating jet fuel prices, creating more predictable budgeting and cost management.

Practice Questions

Question 1

Which of the following is a primary reason investors might include commodities in their portfolios?

A) Commodities tend to have high correlations with equities and bonds.

B) Commodities generally provide a hedge against inflation.

C) Commodities are highly stable and offer consistent returns.

D) Commodity investments have limited liquidity and are rarely traded.

Answer: B) Commodities generally provide a hedge against inflation.

Explanation: Commodities are often considered an effective hedge against inflation. This is because, as inflation rises, the prices of raw materials like oil, metals, and agricultural products tend to increase, preserving the purchasing power of investments in these assets. This relationship contrasts with bonds and equities, which may not perform as well during inflationary periods. Commodities usually have low to moderate correlations with traditional asset classes, such as equities and bonds, providing diversification benefits rather than the high correlation mentioned in option A. Option C is incorrect because commodities are inherently volatile, with prices impacted by various factors, such as supply disruptions and economic demand. Lastly, option D is incorrect as many commodities (like crude oil and gold) are highly liquid and traded on major exchanges.

Question 2

A wheat farmer wants to protect themselves from potential losses due to falling wheat prices at the time of harvest. Which derivative instrument would most likely be appropriate for hedging this risk?

A) Buying wheat futures

B) Selling wheat futures

C) Buying a call option on wheat

D) Selling a put option on wheat

Answer: B) Selling wheat futures

Explanation: To hedge against the risk of falling wheat prices, the farmer should sell wheat futures. By doing so, the farmer locks in a price for their wheat at harvest time, ensuring they can sell at a predetermined price even if market prices decline. This is a common hedging strategy for producers of commodities. Buying wheat futures (option A) would be inappropriate for the farmer’s goal, as it would increase exposure to price increases rather than protect against declines. Option C (buying a call option on wheat) would give the farmer the right to buy wheat, which is not helpful, as they are a seller of the commodity. Selling a put option (option D) would expose the farmer to additional risk, as they might be obligated to buy wheat if the option were exercised by the buyer.

Question 3

Which of the following statements is correct regarding the term “contango” in commodity markets?

A) Contango occurs when the spot price is higher than the futures price.

B) Contango is generally caused by high convenience yields.

C) In a contango market, futures prices are higher than the spot price.

D) Contango indicates an excess supply of the commodity.

Answer: C) In a contango market, futures prices are higher than the spot price.

Explanation: Contango occurs when futures prices are higher than the current spot price. This situation usually arises when storage costs and interest costs associated with holding the commodity exceed the convenience yield (the benefit of holding the physical asset). Contango markets often happen in stable, non-perishable commodities like gold, where there are storage costs but no significant urgency to hold the commodity itself. Option A is incorrect, as it describes “backwardation,” where the spot price is higher than the futures price. Option B is also incorrect; high convenience yields are more associated with backwardation. Option D is a misconception, as contango doesn’t necessarily indicate excess supply but rather reflects the cost of carry involved in holding the assets.