Mortgage-Backed Security

Preparing for the CFA Exam involves a thorough understanding of Mortgage-Backed Securities (MBS), a key component of fixed-income investments. Mastery of MBS structures, underlying mortgage pools, and the factors influencing their value is essential. This knowledge provides insights into risk assessment, yield considerations, and portfolio impact, critical for achieving a high CFA score.

Learning Objective

In studying “Mortgage-Backed Securities” (MBS) for the CFA Exam, you should learn to understand the structure and characteristics of MBS, including pass-through securities, collateralized mortgage obligations (CMOs), and stripped mortgage-backed securities. Analyze the credit risk, prepayment risk, and interest rate risk associated with MBS investments. Evaluate how different types of mortgage pools, loan amortization schedules, and borrower behavior impact MBS performance. Additionally, explore valuation techniques, yield measures, and the role of MBS in diversified portfolios. Apply your knowledge to assessing MBS cash flow structures and determining appropriate strategies for MBS investment in various market conditions.

Introduction to Mortgage-Backed Securities (MBS)

Mortgage-Backed Securities (MBS) are a type of fixed-income investment that represents claims on the cash flows generated by pools of residential or commercial mortgages. Essentially, MBS allows investors to invest in real estate mortgages without directly lending to homeowners or property buyers. These securities were created to provide liquidity to the mortgage market by bundling individual loans from banks or financial institutions into a pool, which is then sold as a security to investors.

The process begins with mortgage originators, like banks, that issue mortgages to borrowers. These loans are then sold to a government agency or private entity, which pools them together and issues MBS. Investors in MBS receive periodic payments from the underlying pool, typically consisting of both principal and interest. MBS types include pass-through securities, where payments are directly passed on to investors, and more structured forms like collateralized mortgage obligations (CMOs), which divide cash flows into different tranches based on varying levels of risk and maturity.

MBS offers attractive returns but carries unique risks, such as prepayment risk (when borrowers pay off loans early) and interest rate risk. It has played a significant role in financial markets, especially in providing opportunities for institutional investors to diversify portfolios and manage interest rate exposure.

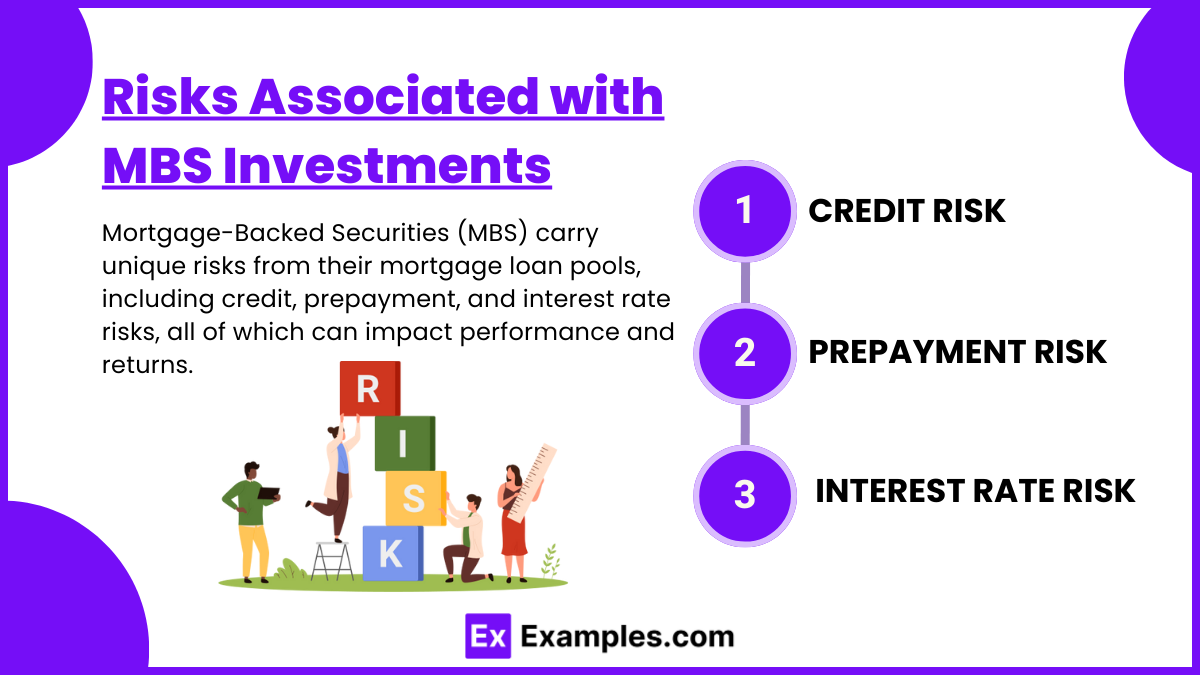

Risks Associated with MBS Investments

Investing in Mortgage-Backed Securities (MBS) comes with several unique risks that stem from the underlying pool of mortgage loans. Key risks associated with MBS investments include credit risk, prepayment risk, and interest rate risk, each of which can significantly impact the security’s performance and returns.

1. Credit Risk

Credit risk in MBS arises from the possibility that borrowers in the mortgage pool may default on their loans, impacting the cash flows to investors. If enough borrowers default, the income generated by the MBS can be reduced, leading to losses for investors. Credit risk is particularly important in non-agency MBS, which are not guaranteed by government entities (like Fannie Mae or Freddie Mac) and rely solely on the quality of the underlying mortgages. To mitigate credit risk, investors often assess the creditworthiness of borrowers, loan-to-value ratios, and the underwriting standards used when the mortgages were issued.

2. Prepayment Risk

Prepayment risk is the risk that mortgage borrowers will pay off their loans earlier than expected, often due to refinancing when interest rates fall or through early principal repayments. Prepayments reduce the overall cash flow to MBS investors, as the outstanding loan balance decreases faster than initially projected. This early return of principal can reduce the expected yield, especially for investors who planned to hold the MBS long-term for its interest payments. When rates fall, prepayments can increase, forcing investors to reinvest the returned principal at a lower yield, a phenomenon known as reinvestment risk.

3. Interest Rate Risk

Interest rate risk is another key consideration for MBS investors. As interest rates rise or fall, the market value of MBS fluctuates. When rates rise, MBS prices generally fall, as newer securities may offer higher returns, making existing MBS less attractive. Additionally, interest rate changes can amplify prepayment risk. For example, when rates decrease, more homeowners may refinance, leading to higher prepayments, while rising rates may slow down prepayments. This variable prepayment rate tied to interest rate changes is often referred to as extension risk, as it may extend the life of the MBS, keeping investors locked into lower-yielding investments as rates rise

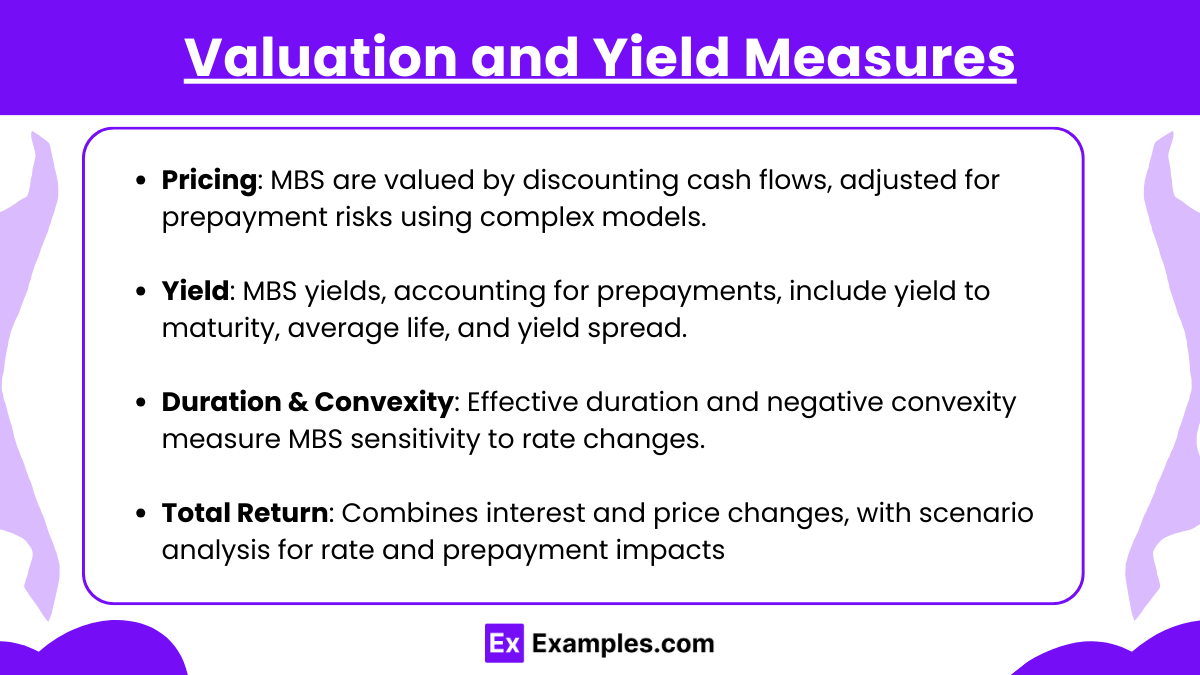

Valuation and Yield Measures

Valuation and yield measures are crucial components in assessing the value and profitability of Mortgage-Backed Securities (MBS). Given the unique cash flow characteristics of MBS, evaluating their worth and expected returns involves specialized techniques that account for factors like prepayment rates, interest rates, and market conditions. Here’s a look at the key methods and concepts in MBS valuation and yield analysis:

1. Pricing MBS

The value of an MBS is calculated by discounting the expected future cash flows from the underlying mortgage pool. Unlike traditional bonds with fixed coupon payments, MBS cash flows are variable due to the potential for prepayments by borrowers. To price MBS accurately, investors often rely on complex models that factor in expected prepayment rates, which are influenced by factors like current interest rates and borrower behavior. Pricing models may use historical prepayment data and predictive algorithms to estimate the likelihood of early loan payoffs, which impacts the security’s cash flow and, ultimately, its price.

2. Yield Analysis

Yield measures for MBS are more complex than those for standard bonds, as they must account for the impact of prepayments on cash flow. The primary yield measure used in MBS analysis is the yield to maturity (YTM), which assumes the security is held until its final maturity date. However, because MBS cash flows can vary, the yield to average life is often used instead, which calculates yield based on the anticipated average life of the MBS, factoring in prepayment assumptions. Another common measure is the yield spread, which compares the MBS yield to a risk-free benchmark (like Treasury yields), helping investors assess the risk premium associated with MBS.

3. Duration and Convexity

Duration and convexity are metrics used to evaluate the sensitivity of MBS prices to interest rate changes. However, because MBS cash flows fluctuate with prepayments, duration for MBS—referred to as effective duration—is adjusted to consider the expected rate of prepayments. Effective duration helps investors understand how much the MBS price might change with a 1% shift in interest rates. Convexity measures the rate of change in duration as interest rates move. MBS often have negative convexity, meaning their prices increase less when interest rates fall (due to prepayments) and decrease more when rates rise, creating asymmetric risk for investors.

4. Total Return

The total return on an MBS includes both the periodic interest payments and the capital gains or losses from changes in the security’s value. Given the unpredictable cash flow of MBS, investors often use scenario analysis to estimate potential total returns under varying interest rate and prepayment scenarios. Scenario analysis helps investors anticipate how different market conditions might impact cash flows and yields, providing a clearer picture of potential returns. This is particularly valuable for MBS since interest rate shifts can significantly affect prepayment rates, cash flow timing, and reinvestment opportunities

Examples

Example 1

An investor purchases a pass-through MBS backed by residential mortgages. The investor receives monthly payments that include both interest and principal, with the cash flows directly “passing through” from the underlying mortgage borrowers. As homeowners make their mortgage payments, the investor benefits from a steady stream of income.

Example 2

A portfolio manager adds a collateralized mortgage obligation (CMO) to their portfolio. This CMO is divided into different tranches with varying maturities and risk levels. The manager selects a specific tranche based on the desired level of risk and return, knowing that higher-risk tranches may offer higher yields but come with more exposure to prepayment risk.

Example 3

A real estate investment trust (REIT) specializing in mortgage-backed securities invests in agency MBS, which are guaranteed by government-sponsored enterprises like Fannie Mae or Freddie Mac. This REIT benefits from the credit backing of the U.S. government, which makes agency MBS generally lower in credit risk, although they still carry interest rate and prepayment risks.

Example 4

An institutional investor includes commercial mortgage-backed securities (CMBS) in their fixed-income portfolio. These CMBS are backed by a pool of commercial mortgages, such as loans for office buildings and retail spaces. CMBS provide the investor with exposure to the commercial real estate market and are structured to minimize prepayment risk, as commercial loans often have longer lock-in periods than residential mortgages.

Example 5

A hedge fund manager uses MBS as part of a bond ladder strategy. They invest in a variety of MBS with staggered maturities to manage cash flows over time and hedge against interest rate changes. By adjusting MBS investments within the ladder, the manager aims to optimize yield and minimize reinvestment risk, benefiting from cash flows that are reinvested at different interest rates

Practice Questions

Question 1

What is a primary risk associated with investing in Mortgage-Backed Securities (MBS)?

A) Liquidity risk

B) Currency risk

C) Prepayment risk

D) Inflation risk

Answer: C) Prepayment risk

Explanation: Prepayment risk is a significant concern for MBS investors because borrowers may repay their mortgages early, particularly when interest rates fall. This early payoff reduces the expected cash flow, forcing investors to reinvest at potentially lower rates. Liquidity and currency risks are generally less associated with MBS, and inflation risk is more relevant to purchasing power rather than specific to MBS.

Question 2

Which type of MBS is divided into tranches with varying levels of risk and maturity?

A) Agency MBS

B) Pass-through MBS

C) Collateralized Mortgage Obligation (CMO)

D) Stripped MBS

Answer: C) Collateralized Mortgage Obligation (CMO)

Explanation: A CMO is an MBS structure where the underlying mortgage pool is divided into different tranches. Each tranche has specific risk, maturity, and cash flow characteristics, allowing investors to select the tranche that best aligns with their risk tolerance and investment goals. Pass-through and agency MBS are not divided into tranches, and stripped MBS involve separating principal and interest payments rather than risk levels.

Question 3

Which of the following best describes a benefit of including MBS in a diversified investment portfolio?

A) MBS offer guaranteed returns

B) MBS help reduce exposure to equity market risk

C) MBS are immune to interest rate fluctuations

D) MBS eliminate prepayment risk

Answer: B) MBS help reduce exposure to equity market risk

Explanation: MBS provide diversification in a fixed-income portfolio and are typically less correlated with equity markets. This can help reduce overall portfolio volatility. However, MBS returns are not guaranteed and are affected by interest rate changes and prepayment risk.