Overview of Private Wealth Management

Private Wealth Management (PWM) involves the provision of personalized financial services to high-net-worth individuals (HNWIs), typically those with significant investable assets. The goal is to address the unique financial needs of clients by offering a comprehensive suite of services, such as investment management, estate planning, tax optimization, retirement planning, and risk management. This area requires a deep understanding of both financial markets and the client’s personal circumstances, including their objectives, risk tolerance, and family dynamics. PWM professionals must also navigate legal, tax, and regulatory complexities to ensure that clients’ wealth is efficiently managed across generations.

Learning Objectives

In studying “Overview of Private Wealth Management” for the CFA, you should learn to understand the key aspects of managing the financial resources of high-net-worth individuals, including the unique goals, constraints, and risk tolerance levels that distinguish private wealth clients from institutional investors. Recognize the impact of factors such as taxation, estate planning, and behavioral biases on wealth management strategies. Analyze the roles of investment advisors and wealth managers in providing personalized financial solutions that address clients’ short-term needs and long-term goals. Evaluate asset allocation, risk management, and portfolio customization techniques in the context of private wealth. Additionally, gain insight into the importance of relationship management and client communication in delivering effective wealth management services.

Understanding the Key Aspects of Private Wealth Management

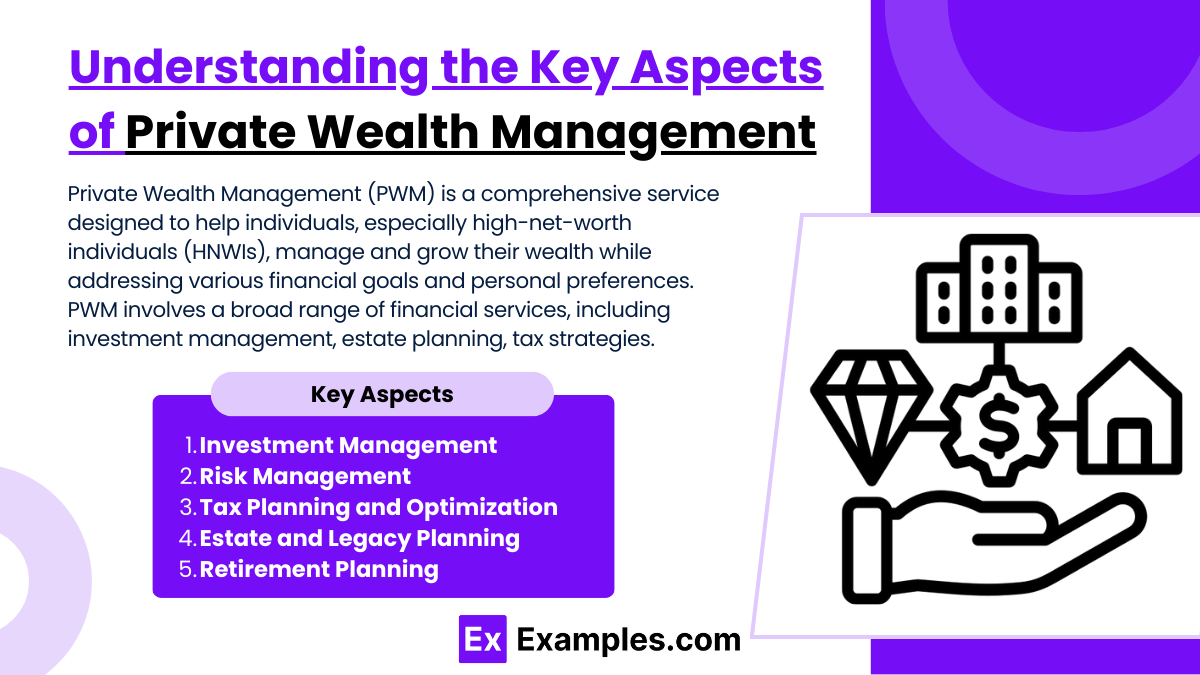

Private Wealth Management (PWM) is a comprehensive service designed to help individuals, especially high-net-worth individuals (HNWIs), manage and grow their wealth while addressing various financial goals and personal preferences. PWM involves a broad range of financial services, including investment management, estate planning, tax strategies, and risk management, tailored to meet each client’s unique needs. Here are the key aspects that define private wealth management and its role in supporting financial well-being.

1. Investment Management

Investment management is the cornerstone of private wealth management, focusing on building and managing a diversified portfolio to meet the client’s risk tolerance, time horizon, and financial goals.

- Asset Allocation: PWM professionals develop a customized asset allocation strategy that aligns with the client’s risk profile and investment objectives, often balancing growth assets (e.g., equities) with income or conservative assets (e.g., bonds).

- Portfolio Optimization: Portfolios are structured to maximize returns for a given level of risk, often incorporating a mix of traditional investments (stocks, bonds) and alternative investments (private equity, real estate).

- Regular Monitoring and Rebalancing: Ongoing monitoring ensures that the portfolio remains aligned with market conditions and client goals, with periodic rebalancing to adjust for asset performance and market changes.

Example: A PWM advisor may create a balanced portfolio for a client nearing retirement, allocating 60% to income-generating bonds and 40% to growth-oriented stocks, rebalancing periodically to maintain this balance.

2. Risk Management

Risk management in PWM involves identifying, assessing, and mitigating risks that could impact the client’s financial security, such as market volatility, economic downturns, or unforeseen personal events.

- Diversification: Diversifying assets across different sectors, regions, and asset classes helps mitigate portfolio risk by reducing reliance on any one investment.

- Insurance Solutions: PWM advisors often recommend life insurance, health insurance, and liability insurance to protect against personal risks and provide financial security to the client’s family.

- Alternative Investments: For clients with a high-risk tolerance, PWM may include alternative assets such as hedge funds, commodities, or private equity, which can offer uncorrelated returns and further diversify the portfolio.

Example: An HNWI concerned about market downturns may be advised to allocate a portion of their portfolio to real assets like real estate or commodities, which may hold value during stock market volatility.

3. Tax Planning and Optimization

Tax planning aims to maximize after-tax returns by leveraging tax-efficient strategies. This is especially important for HNWIs, who may face higher tax liabilities on their investments, income, and estates.

- Tax-Efficient Investments: PWM advisors may recommend municipal bonds, which offer tax-free income, or tax-efficient ETFs and index funds, which minimize capital gains taxes.

- Asset Location: Placing tax-inefficient assets (e.g., bonds, REITs) in tax-advantaged accounts (IRAs, 401(k)s) and tax-efficient assets in taxable accounts to reduce overall tax exposure.

- Tax-Loss Harvesting: Selling underperforming investments to offset capital gains taxes on other investments, thus reducing the overall tax burden.

Example: A PWM advisor might recommend holding dividend-paying stocks in a tax-advantaged retirement account to avoid dividend taxes, while placing index funds in a taxable account due to their tax efficiency.

4. Estate and Legacy Planning

Estate and legacy planning ensures that a client’s wealth is preserved, protected, and transferred according to their wishes, benefiting future generations and supporting charitable causes if desired.

- Trusts and Wills: Setting up trusts, wills, and other legal documents helps structure asset distribution, minimize estate taxes, and protect assets from legal claims.

- Gifting Strategies: Advisors may suggest gifting strategies, such as annual exclusion gifts or charitable donations, to reduce the taxable estate while fulfilling philanthropic goals.

- Succession Planning: For clients with family businesses, PWM often includes succession planning to ensure the seamless transition of business assets to the next generation.

Example: A high-net-worth client may set up a family trust to transfer assets to heirs with minimal tax liability while ensuring that certain assets remain under family control.

5. Retirement Planning

Retirement planning is a key focus in private wealth management, helping clients maintain their desired lifestyle during retirement by ensuring sufficient income and financial security.

- Income Projections: PWM professionals create projections based on current assets, expected growth, and estimated expenses to determine if the client’s retirement goals are achievable.

- Tax-Advantaged Accounts: Advisors recommend using retirement accounts like IRAs, 401(k)s, or Roth IRAs to maximize tax benefits and growth potential over time.

- Withdrawal Strategies: Effective withdrawal strategies, such as the “bucket” approach or the 4% rule, help ensure that clients have a steady income stream throughout retirement without depleting their savings too quickly.

Example: A PWM advisor may recommend a combination of taxable and tax-deferred accounts for a client to draw from during retirement, minimizing taxes and maximizing after-tax income.

Recognizing the Impact of Taxation, Estate Planning, and Behavioral Biases

In wealth management, understanding the impact of taxation, estate planning, and behavioral biases is crucial to effectively building and preserving wealth. These elements influence decisions on asset allocation, risk management, and long-term financial planning. Here’s how each of these factors affects wealth management strategies and why they are essential in helping clients achieve financial goals.

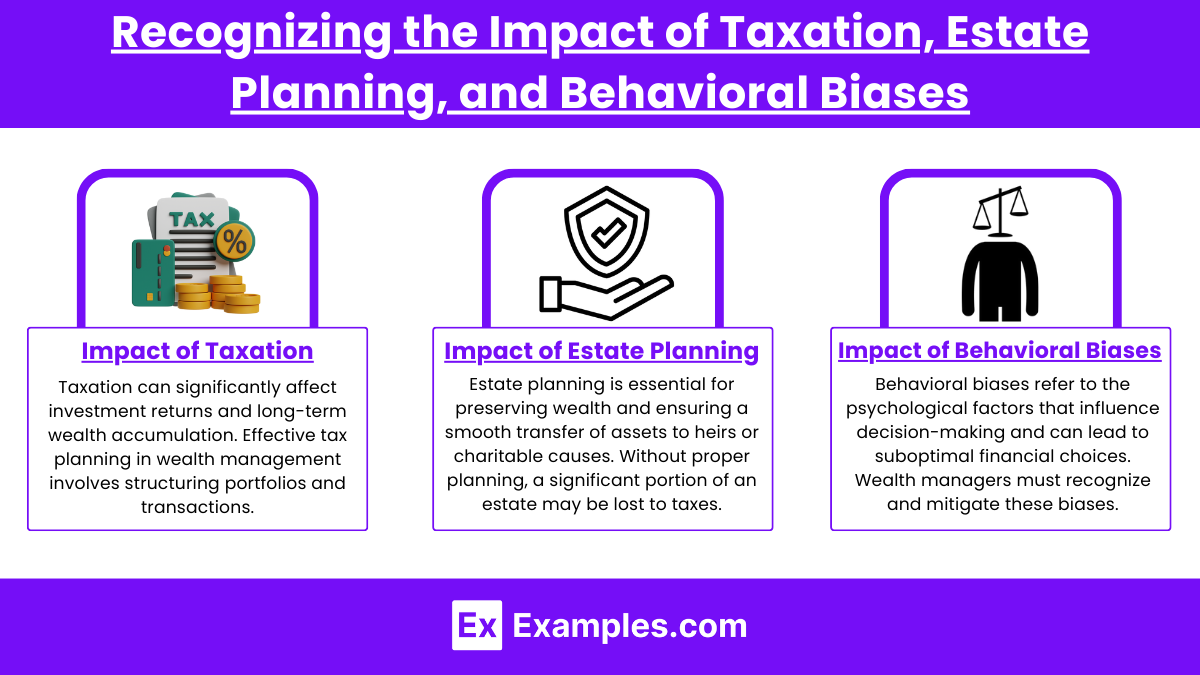

1. Impact of Taxation

Taxation can significantly affect investment returns and long-term wealth accumulation. Effective tax planning in wealth management involves structuring portfolios and transactions to minimize tax liabilities, maximizing after-tax returns.

- Income Tax Management: Taxation on interest, dividends, and capital gains can erode investment returns, particularly for high-net-worth individuals (HNWIs) in higher tax brackets. Managing income taxes may involve selecting tax-efficient investments, such as municipal bonds, and placing tax-inefficient assets, like bonds and REITs, in tax-deferred accounts.

- Capital Gains Tax: Realizing gains on investments can trigger capital gains taxes, which can be managed through strategies like tax-loss harvesting, where underperforming assets are sold to offset gains. Wealth managers often consider the holding period (short-term vs. long-term gains) to reduce taxes, as long-term capital gains are generally taxed at a lower rate.

- Tax-Efficient Asset Location: Structuring portfolios with tax efficiency involves placing tax-efficient investments (e.g., ETFs, index funds) in taxable accounts and tax-inefficient investments in tax-advantaged accounts like IRAs. This strategy helps optimize after-tax returns.

Example: An HNWI with a mix of equities, bonds, and real estate might keep dividend-paying stocks in a retirement account to defer taxes, while holding tax-efficient index funds in a taxable account to reduce tax liabilities.

2. Impact of Estate Planning

Estate planning is essential for preserving wealth and ensuring a smooth transfer of assets to heirs or charitable causes. Without proper planning, a significant portion of an estate may be lost to taxes and probate, reducing the amount passed on to future generations.

- Reducing Estate Taxes: Estate taxes can significantly reduce the value of an inheritance. Estate planning tools, such as irrevocable trusts and gifting strategies, help reduce the taxable estate by transferring assets during the client’s lifetime, allowing more wealth to pass to beneficiaries with minimal tax impact.

- Trusts and Wills: Setting up trusts can provide control over asset distribution, ensuring that wealth is managed according to the client’s wishes. Trusts can also protect assets from creditors and legal claims, and they help avoid probate, which can be time-consuming and costly.

- Legacy and Charitable Planning: For clients interested in philanthropy, estate planning can include charitable trusts, donor-advised funds, or direct gifts to charities. These strategies provide tax benefits and allow clients to leave a lasting impact on causes they care about, while also reducing the taxable estate.

Example: A client with substantial assets may set up a family trust to transfer wealth to heirs while minimizing estate taxes. They might also establish a charitable trust to support a favorite cause, creating both a legacy and a tax-efficient structure.

3. Impact of Behavioral Biases

Behavioral biases refer to the psychological factors that influence decision-making and can lead to suboptimal financial choices. Wealth managers must recognize and mitigate these biases to help clients stay on track with their long-term goals.

- Loss Aversion: Clients may feel the pain of losses more acutely than the pleasure of gains, leading them to avoid risks even when potential rewards are high. This bias can result in overly conservative portfolios that don’t align with long-term growth goals.

- Overconfidence: Overconfident clients may believe they can “time” the market or make superior stock picks, leading to excessive trading and high transaction costs. Overconfidence can also result in concentrated investments in familiar or popular stocks, increasing risk.

- Herding Behavior: Clients may follow market trends or popular investments due to fear of missing out (FOMO), leading to impulsive decisions. This often results in buying high and selling low, which can reduce returns over time.

- Home Bias: Home bias is the tendency to favor domestic investments over international ones, often due to familiarity. This can limit diversification, exposing the portfolio to local economic risks.

Example: A wealth manager might work with a client exhibiting loss aversion by constructing a diversified portfolio that includes conservative assets for stability and higher-growth assets for long-term growth. This approach balances risk and return, helping the client feel more comfortable with potential market fluctuations.

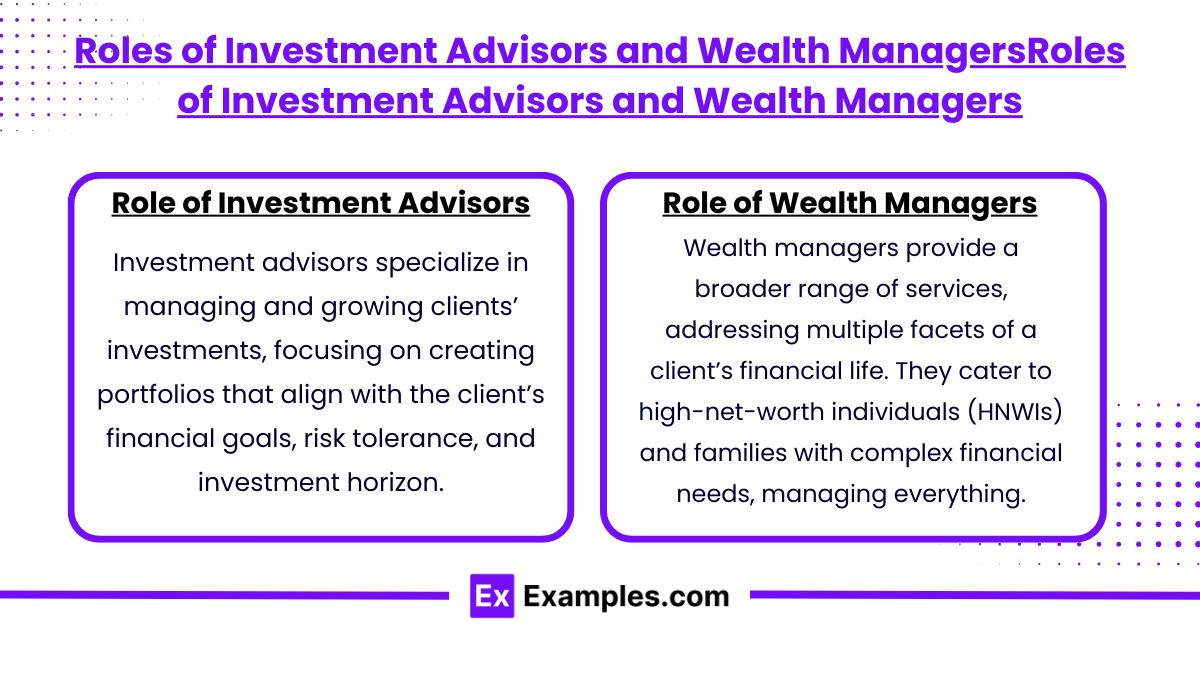

Roles of Investment Advisors and Wealth ManagersRoles of Investment Advisors and Wealth Managers

Investment Advisors and Wealth Managers both play essential roles in guiding clients through financial decisions, but they focus on different aspects of a client’s financial life. Investment advisors primarily focus on managing and growing investment portfolios, while wealth managers take a more comprehensive approach, overseeing all aspects of a client’s financial situation, from estate planning to tax strategies. Here’s a closer look at the roles, responsibilities, and differences between these two professionals.

1. Role of Investment Advisors

Investment advisors specialize in managing and growing clients’ investments, focusing on creating portfolios that align with the client’s financial goals, risk tolerance, and investment horizon.

- Portfolio Management: Investment advisors design, implement, and manage portfolios tailored to each client’s specific needs, balancing asset allocation across stocks, bonds, and other securities based on risk tolerance and financial objectives.

- Investment Strategy and Analysis: Advisors conduct in-depth research to identify investment opportunities, analyze market trends, and make informed decisions on which securities to buy, hold, or sell. They may employ strategies like growth investing, value investing, or income-focused strategies depending on the client’s goals.

- Risk Assessment and Management: Investment advisors evaluate clients’ risk tolerance and use techniques such as diversification and rebalancing to manage risk within the portfolio. They adjust asset allocation as market conditions change to maintain alignment with clients’ risk profiles.

- Regular Reporting and Communication: Advisors provide clients with regular performance updates, explaining portfolio changes and reviewing progress toward investment goals. Transparency and effective communication are crucial, as they build client trust and confidence in the advisor’s decisions.

- Financial Planning (Limited Scope): While their primary focus is on investments, some investment advisors may offer limited financial planning services, such as retirement planning or goal-based investing, to complement the portfolio management.

Example: An investment advisor may construct a diversified portfolio for a client focused on long-term growth, allocating a mix of large-cap stocks, international equities, and bonds. They would monitor and adjust the portfolio as market conditions change to optimize performance within the client’s risk tolerance.

2. Role of Wealth Managers

Wealth managers provide a broader range of services, addressing multiple facets of a client’s financial life. They cater to high-net-worth individuals (HNWIs) and families with complex financial needs, managing everything from investment strategies to estate planning, tax strategies, and more.

- Comprehensive Financial Planning: Wealth managers develop a holistic financial plan that covers short-term and long-term goals, including retirement planning, college savings, major purchases, and more. This plan forms the foundation for all financial decisions, ensuring that each aspect supports the client’s overall objectives.

- Investment Management: Similar to investment advisors, wealth managers also manage clients’ investments. However, their investment strategies are often part of a larger financial plan, and they may coordinate with other aspects, like tax strategies or estate plans, to maximize overall wealth.

- Tax Planning and Optimization: Wealth managers work with tax professionals to develop tax-efficient strategies, such as tax-loss harvesting, asset location strategies, and minimizing capital gains. They help clients structure investments to optimize after-tax returns and reduce overall tax burdens.

- Estate and Legacy Planning: Estate planning is a major component of wealth management, focusing on preserving wealth across generations. Wealth managers work with estate attorneys to structure wills, trusts, and other legal tools to ensure a smooth transfer of assets while minimizing estate taxes.

- Risk and Insurance Planning: Wealth managers assess potential financial risks, such as health issues, liability, or market downturns, and may recommend insurance solutions, such as life, health, and liability insurance, to protect the client’s wealth.

- Philanthropic and Charitable Planning: For clients interested in philanthropy, wealth managers provide strategies to structure charitable contributions efficiently, such as setting up charitable trusts or donor-advised funds. They help clients fulfill philanthropic goals while maximizing tax benefits.

- Behavioral Coaching and Education: Wealth managers help clients navigate financial decisions, managing emotional biases like loss aversion or overconfidence. They educate clients about long-term strategies and guide them through market fluctuations, helping to ensure rational decision-making.

Example: A wealth manager may work with a client on a retirement plan, setting up an investment strategy that aligns with tax and estate planning. They may advise the client on setting up a trust to pass assets on to heirs, ensuring tax efficiency and minimizing probate, all while maintaining the client’s desired lifestyle.

Evaluating Asset Allocation, Risk Management, and Portfolio Customization

Asset allocation, risk management, and portfolio customization are foundational aspects of effective portfolio management. Together, these practices ensure that portfolios are aligned with clients’ financial goals, risk tolerance, and investment preferences. Evaluating each of these areas helps create a balanced, personalized strategy that maximizes returns while managing risks.

1. Asset Allocation

Asset allocation is the process of distributing investments across different asset classes (e.g., equities, bonds, real estate, and cash) to achieve the desired risk-return balance for a portfolio. It is often considered the most important factor in determining portfolio performance and is tailored to each investor’s financial goals, time horizon, and risk tolerance.

- Strategic Asset Allocation: This long-term approach establishes target allocations for each asset class based on the client’s objectives and risk tolerance. Once set, these allocations remain relatively stable, with periodic rebalancing to maintain target weights. Strategic allocation suits investors with well-defined, long-term goals.

- Tactical Asset Allocation: This more dynamic approach allows for adjustments in asset allocation based on short-term market conditions and economic forecasts. Tactical allocation aims to capitalize on market opportunities, adjusting allocations to improve returns or manage risks. This approach suits investors who are more flexible and willing to respond to market changes.

- Core-Satellite Approach: This hybrid strategy combines a stable core portfolio (strategically allocated across asset classes) with satellite positions in more opportunistic investments. The core portion maintains consistency, while the satellite portion allows for tactical moves to boost returns or hedge against specific risks.

Example: An investor with a high tolerance for risk and a long time horizon might adopt an 80% equity, 20% bond allocation to maximize growth. A conservative investor close to retirement, however, might hold 40% equities and 60% bonds, prioritizing stability and income.

Evaluation: The asset allocation process involves regular reviews to ensure it aligns with changing market conditions and the client’s evolving needs. Rebalancing is essential to maintain the intended risk-return profile as markets fluctuate.

2. Risk Management

Risk management in portfolio management aims to identify, measure, and control the level of risk within a portfolio to protect against losses and support long-term investment objectives. Effective risk management balances risk and return to ensure clients are not exposed to unnecessary volatility.

- Diversification: Diversification spreads investments across asset classes, sectors, and geographic regions to reduce unsystematic risk. By holding a mix of uncorrelated assets, the portfolio becomes less vulnerable to the poor performance of any single asset or sector.

- Asset Allocation as Risk Management: Asset allocation itself is a form of risk management. Higher-risk assets (like equities) are balanced with lower-risk assets (like bonds) based on the client’s risk tolerance. Adjusting asset allocation during periods of market volatility can also mitigate risk.

- Hedging Strategies: For portfolios that require additional protection, managers may use hedging techniques, such as options, futures, or inverse ETFs. These instruments can help guard against market declines or currency fluctuations, particularly in portfolios exposed to specific risks.

- Risk Measurement Tools: Tools like Value at Risk (VaR), standard deviation, and beta measure and monitor portfolio risk. VaR estimates the potential loss over a set period, while standard deviation measures volatility, and beta assesses how a portfolio moves in relation to the overall market.

Example: A client nearing retirement might have a diversified portfolio of 50% bonds, 30% equities, and 20% in alternative investments like real estate. To protect against interest rate risk, the portfolio manager could use interest rate swaps or keep the bond duration short.

Evaluation: Risk management requires continuous monitoring, as risk exposure can change with market conditions. Regular risk assessments ensure that the portfolio remains within the client’s risk tolerance, with adjustments made as needed.

3. Portfolio Customization

Portfolio customization tailors investment strategies to meet specific client needs and preferences. This personalized approach ensures that the portfolio aligns with the client’s financial goals, tax situation, ethical considerations, and lifestyle factors.

- Goal-Based Customization: Portfolios are customized based on specific financial goals, such as retirement, education funding, or wealth preservation. Each goal has its own time horizon and risk tolerance, influencing the asset allocation and investment strategy. For example, retirement-focused portfolios prioritize income generation and capital preservation as the client nears retirement.

- Tax Efficiency: High-net-worth clients or those in high tax brackets often require tax-efficient portfolio management. Customizing portfolios to reduce tax liabilities may involve tax-advantaged accounts, tax-efficient investments, and tax-loss harvesting to maximize after-tax returns.

- ESG and Ethical Preferences: Clients who prioritize environmental, social, and governance (ESG) criteria or have ethical preferences may avoid certain industries (e.g., fossil fuels) and favor companies with positive social or environmental practices. Customization allows portfolios to reflect these preferences without sacrificing performance.

- Income Needs and Liquidity: For clients with income needs, the portfolio can be structured to generate regular cash flow through dividend stocks, bonds, or real estate investments. For clients who require liquidity, assets with low lock-in periods or high tradability are prioritized.

Example: A client with a high income might prefer a tax-efficient portfolio with a focus on low-turnover index funds and municipal bonds. Another client interested in socially responsible investing could have a portfolio overweighted in renewable energy and technology sectors.

Evaluation: Portfolio customization is an ongoing process. As clients’ financial situations and goals evolve, their portfolios need to be adjusted accordingly, ensuring they continue to reflect personal preferences and changing financial circumstances.

Examples

Example 1: Personalized Financial Planning

Private wealth management involves creating tailored financial plans that align with an individual’s specific goals, risk tolerance, and time horizon. Wealth managers assess a client’s current financial situation, future aspirations, and investment preferences to design a comprehensive strategy. This personalized approach ensures that clients receive advice and solutions that fit their unique financial circumstances.

Example 2: Investment Management

A core component of private wealth management is the management of investment portfolios. Wealth managers analyze market conditions, asset classes, and investment opportunities to construct a diversified portfolio aimed at maximizing returns while managing risk. They regularly review and adjust the portfolio to adapt to changes in the market and the client’s financial goals, ensuring that the investment strategy remains aligned with their objectives.

Example 3: Tax Optimization Strategies

Wealth management services often include tax planning and optimization to enhance a client’s after-tax returns. Wealth managers work with tax advisors to implement strategies that minimize tax liabilities, such as utilizing tax-efficient investment vehicles, tax-loss harvesting, and estate planning techniques. This focus on tax efficiency can significantly impact a client’s overall financial success and net worth.

Example 4: Estate Planning

Private wealth management encompasses comprehensive estate planning to ensure that clients’ assets are distributed according to their wishes after their passing. Wealth managers help clients establish wills, trusts, and other legal instruments that facilitate a smooth transfer of wealth to beneficiaries while minimizing estate taxes. This aspect of wealth management is critical for preserving family legacies and ensuring that clients’ financial goals are met in the long term.

Example 5: Philanthropic Advisory Services

Many wealthy individuals seek to incorporate philanthropy into their wealth management strategies. Private wealth managers offer philanthropic advisory services to help clients identify charitable causes that align with their values and financial goals. They assist in structuring charitable donations, setting up foundations, and planning for impactful giving, ensuring that clients can make a meaningful difference while also considering the financial implications of their philanthropic activities.

Practice Questions

Question 1

What is the primary goal of private wealth management?

A) To maximize short-term trading profits

B) To provide personalized financial strategies that meet clients’ long-term financial goals

C) To focus solely on tax minimization

D) To manage corporate investment portfolios

Correct Answer: B) To provide personalized financial strategies that meet clients’ long-term financial goals.

Explanation: The primary goal of private wealth management is to create tailored financial strategies that align with the individual goals and objectives of clients. This includes long-term financial planning, investment management, tax optimization, estate planning, and more. Unlike other areas of finance that may focus on short-term gains or specific tax strategies, private wealth management emphasizes a comprehensive approach to help clients achieve their financial aspirations over time.

Question 2

Which of the following services is typically included in private wealth management?

A) Retail banking services

B) Estate planning and asset protection

C) Corporate financial analysis

D) Mortgage lending

Correct Answer: B) Estate planning and asset protection.

Explanation: Estate planning and asset protection are essential components of private wealth management. Wealth managers help clients develop strategies to ensure their assets are managed according to their wishes after their death while minimizing taxes and legal complications. This often involves creating wills, trusts, and other legal documents. Options A, C, and D are not typically associated with private wealth management, as they pertain to different areas of finance.

Question 3

How does private wealth management differ from traditional investment management?

A) It focuses only on stocks and bonds.

B) It offers a more comprehensive approach that includes personal financial planning and wealth preservation strategies.

C) It is exclusively for high-net-worth individuals.

D) It requires clients to make frequent trades.

Correct Answer: B) It offers a more comprehensive approach that includes personal financial planning and wealth preservation strategies.

Explanation: Private wealth management distinguishes itself from traditional investment management by taking a holistic approach that goes beyond just managing investment portfolios. It incorporates various aspects of financial planning, including tax strategies, retirement planning, estate planning, and risk management, tailored to the unique needs of high-net-worth individuals. While traditional investment management focuses primarily on asset allocation and investment performance, private wealth management encompasses a broader range of financial services and long-term strategies.