Pricing and Valuation of Forward Contracts and Forwards

Preparing for the CFA Exam requires a comprehensive understanding of "Pricing and Valuation of Forward Contracts and Forwards," a crucial component of derivatives markets. Mastery of the mechanisms and determinants of forward prices and valuations is essential. This knowledge provides insights into hedging strategies, risk management, and speculative opportunities, critical for achieving a high CFA score.

Learning Objective

In studying "Pricing and Valuation of Forward Contracts and Forwards" for the CFA Exam, you should learn to understand the mechanisms and models used to price and value forward contracts. Analyze how interest rates, spot prices, and storage costs influence forward prices. Evaluate the principles behind the no-arbitrage condition and the cost-of-carry model. Additionally, explore how these financial instruments are utilized in both hedging and speculation, and their implications for risk management. Apply your understanding by calculating forward prices and valuations and interpreting the outcomes in the context of market scenarios and investment strategies, enhancing your proficiency in financial derivatives.

Introduction to Forward Contracts

Forward contracts are financial agreements between two parties to buy or sell an asset at a predetermined price on a specified future date. These contracts are used primarily to hedge against price fluctuations or to speculate on future price movements.

Key Features of Forward Contracts:

Customization: Forward contracts are over-the-counter (OTC) instruments, meaning they can be tailored to fit the specific needs of the buyer and seller in terms of contract size, asset type, and maturity date.

Underlying Assets: Common underlying assets include currencies, commodities, stocks, and bonds.

Settlement: At the maturity date, the contract can be settled either through physical delivery of the asset or cash settlement, depending on the terms agreed upon.

Pricing Mechanisms for Forward Contracts

Pricing mechanisms for forward contracts are critical for determining the fair value at which the contract is established. The pricing depends on the cost of carrying the underlying asset until the contract's maturity date. Here’s a breakdown of how forward contract pricing works:

1. Basic Pricing Formula

The forward price (F0) for an asset can be determined using the following formula:

S0: Current spot price of the underlying asset.

r: Risk-free interest rate (annualized, continuously compounded).

T: Time to maturity in years.

e: The mathematical constant (approximately 2.71828).

2. Cost of Carry Model

The forward price reflects the “cost of carry,” which includes costs incurred for holding the underlying asset until the contract's maturity. These costs can include:

Storage Costs: Applicable to physical commodities like oil or grain.

Financing Costs: The cost of borrowing funds to purchase the asset.

Dividend or Yield Adjustments: For assets like stocks or bonds, expected dividends or coupon payments are subtracted from the carrying cost.

3. Forward Pricing for Currency Contracts

For currency forwards, the pricing mechanism incorporates the interest rate differential between the two currencies. The formula is:

rd: Domestic risk-free interest rate.

rf: Foreign risk-free interest rate.

T: Time to maturity in years.

4. Interest Rate Forwards

For forward rate agreements (FRAs), the forward price can be derived from the difference between two future interest rates and adjusted for the contract’s notional amount and duration.

5. No-Arbitrage Condition

The concept of arbitrage ensures that the forward price must be set in a way that prevents risk-free profit opportunities. If the forward price deviates significantly from the no-arbitrage price, traders will buy or sell the asset and the forward contract to lock in a risk-free gain, driving the prices back into alignment.

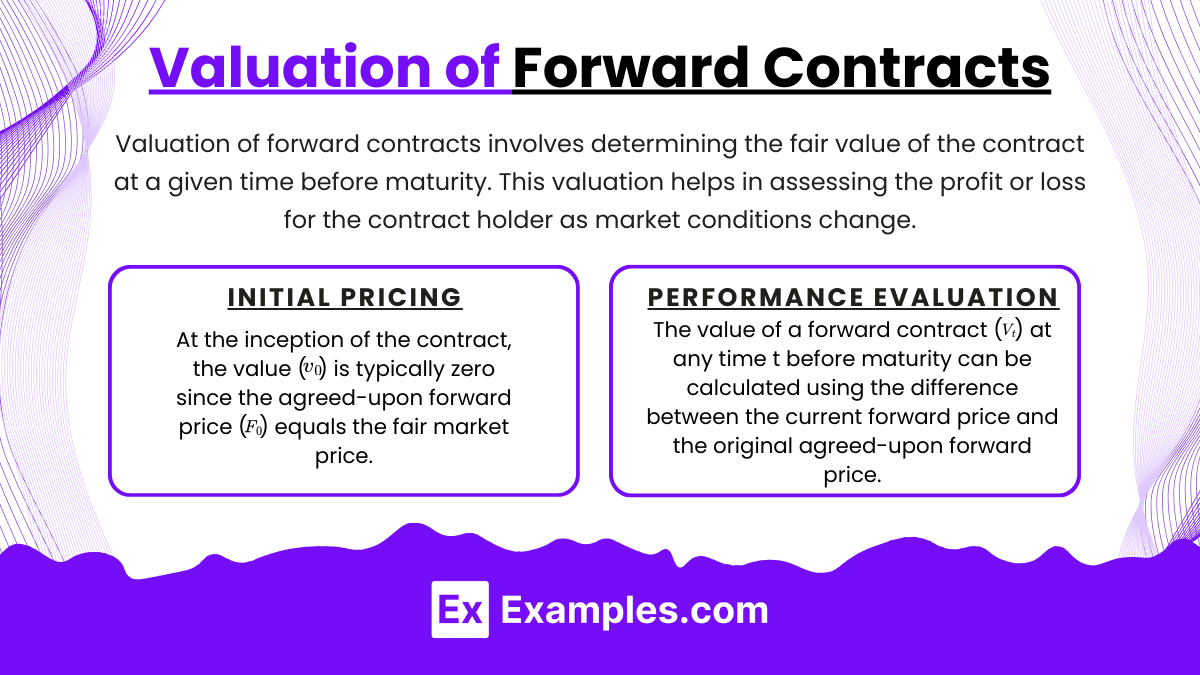

Valuation of Forward Contracts

Valuation of forward contracts involves determining the fair value of the contract at a given time before maturity. This valuation helps in assessing the profit or loss for the contract holder as market conditions change.

Key Concepts in Forward Contract Valuation:

Initial Pricing:

At the inception of the contract, the value (V0) is typically zero since the agreed-upon forward price (F0) equals the fair market price.

Valuation Before Maturity:

The value of a forward contract (Vt) at any time t before maturity can be calculated using the difference between the current forward price and the original agreed-upon forward price.

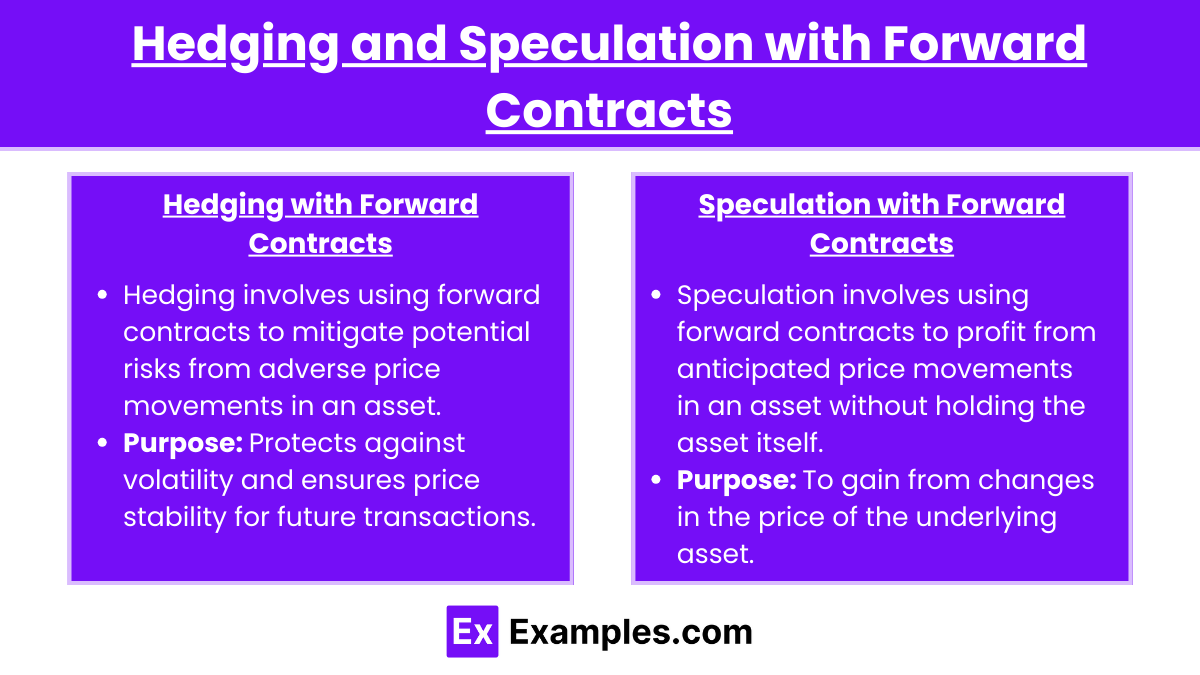

Hedging and Speculation with Forward Contracts

Forward contracts are commonly used for both hedging and speculation in financial markets. Here’s an overview of how these strategies work with forward contracts:

1. Hedging with Forward Contracts

Hedging involves using forward contracts to mitigate potential risks from adverse price movements in an asset.

Purpose: Protects against volatility and ensures price stability for future transactions.

How It Works:

Example: A U.S. company expecting to receive payment in euros in 6 months can enter a forward contract to sell euros at a fixed exchange rate. This locks in the rate, protecting the company from potential depreciation in the euro.

Outcome: If the euro depreciates at maturity, the company avoids losses by selling at the pre-agreed rate. If the euro appreciates, the company does not benefit from the favorable change but is protected against losses.

Benefits:

Reduces uncertainty and stabilizes cash flows.

Protects profit margins from adverse price changes.

Drawbacks:

Limited upside potential; if prices move favorably, the hedger doesn’t benefit beyond the agreed rate.

2. Speculation with Forward Contracts

Speculation involves using forward contracts to profit from anticipated price movements in an asset without holding the asset itself.

Purpose: To gain from changes in the price of the underlying asset.

How It Works:

Example: A trader anticipates that the price of a commodity will increase in 3 months. They enter a forward contract to buy the commodity at a set price. If the price rises as expected, the trader profits by purchasing at the lower, pre-agreed price and selling at the higher market price.

Outcome: If the price moves in the opposite direction, the speculator incurs a loss, as they are obligated to buy or sell at the agreed-upon price.

Benefits:

Potential for significant profits if the market moves in the trader’s favor.

Leverages forecasts and market trends to capitalize on price movements.

Drawbacks:

High risk of losses if market prices move against the trader.

Requires careful market analysis and forecasting to succeed.

Examples

Example 1: Commodity Price Hedging

A coffee manufacturer enters into a forward contract to buy 10,000 pounds of coffee beans at a set price of $1.50 per pound in six months to hedge against potential price increases. This helps the manufacturer stabilize production costs despite fluctuations in commodity markets.

Example 2: Foreign Currency Exposure

A U.S.-based exporter expects to receive €1 million in three months for goods sold to a European client. To hedge against the risk of the euro depreciating against the U.S. dollar, the exporter enters into a forward contract to sell euros and buy U.S. dollars at the current forward exchange rate.

Example 3: Interest Rate Management

A real estate development firm with an upcoming debt obligation of $10 million in one year uses an interest rate forward contract to lock in today's low interest rates. This action protects the firm against the risk of rising interest rates increasing their future debt repayment costs.

Example 4: Equity Forward Contracts for Mergers and Acquisitions

During a merger transaction, a company agrees to buy another firm’s shares at a future date using a forward contract. The agreed price is based on the current stock price plus an agreed-upon return, which helps both parties lock in expectations and reduce uncertainty in the deal.

Example 5: Speculation on Currency Movements

A currency trader anticipates that the Japanese yen will strengthen against the U.S. dollar based on geopolitical events. The trader enters into a forward contract to buy yen and sell dollars at a future date, speculating on this expected movement to realize a profit from exchange rate differences.

Practice Questions

Question 1

What is a primary factor that influences the forward price of a commodity?

A. The dividend yield of the underlying asset

B. The volatility of the underlying asset

C. The storage costs associated with the underlying commodity

D. The credit rating of the issuing company

Answer:

C. The storage costs associated with the underlying commodity

Explanation:

The forward price of a commodity is significantly influenced by the storage costs associated with holding the commodity until the delivery date. This is part of the cost-of-carry model, which includes storage costs, insurance, and any other costs (minus any income earned during the holding period, such as convenience yields) to derive the forward price. Volatility and dividends are more pertinent to options pricing, and credit ratings do not directly affect commodity forward prices.

Question 2

How does the no-arbitrage principle apply to the pricing of forward contracts?

A. It ensures that forward contracts provide higher returns than the risk-free rate.

B. It prevents simultaneous buying and selling of a contract to yield a guaranteed profit.

C. It guarantees that the forward price will match the spot price at contract expiration.

D. It ensures that forward prices are set so that no profit can be made by arbitrage between the spot market and the forward market.

Answer:

D. It ensures that forward prices are set so that no profit can be made by arbitrage between the spot market and the forward market.

Explanation:

The no-arbitrage principle states that the forward price must be set in such a way that it is impossible to make a risk-free profit by entering into simultaneous transactions in the spot market and the forward market. This helps maintain market equilibrium by ensuring that the forward price equals the spot price compounded at the risk-free rate plus any costs or minus any benefits (like yields) associated with holding the asset.

Question 3

What role does the risk-free rate play in the valuation of a currency forward contract?

A. It determines the transaction costs involved in the contract.

B. It affects the future value of the currencies involved in the contract.

C. It indicates the credit risk associated with the counterparty.

D. It influences the convenience yield of the currency.

Answer:

B. It affects the future value of the currencies involved in the contract.

Explanation:

In the valuation of a currency forward contract, the risk-free rate of the currencies involved plays a crucial role. According to interest rate parity, the difference between the risk-free interest rates of two currencies affects the forward exchange rate. The currency of the country with a higher risk-free rate will typically be at a forward discount relative to the currency of the country with a lower risk-free rate, reflecting the interest differential.