Share :

Pricing & Valuation of Forward Commitments

- Notes

Understanding the pricing and valuation of forward commitments, such as forward contracts and futures, is crucial for CFA Level 2 candidates. These derivatives are fundamental tools for risk management, speculative activities, and hedging strategies across various financial markets, including commodities, currencies, and interest rates. Mastery of these concepts is essential for the Derivatives section of the exam.

Learning Objectives

In studying Pricing & Valuation of Forward Commitments for the CFA exam, candidates will thoroughly grasp how forward contracts and futures are priced and valued within financial markets. They will apply key theoretical models, such as the cost of carry model and no-arbitrage pricing, to calculate the fair value and final settlement values of forward commitments. Additionally, candidates will examine how market factors like interest rates, storage costs, and convenience yields influence pricing and valuation.

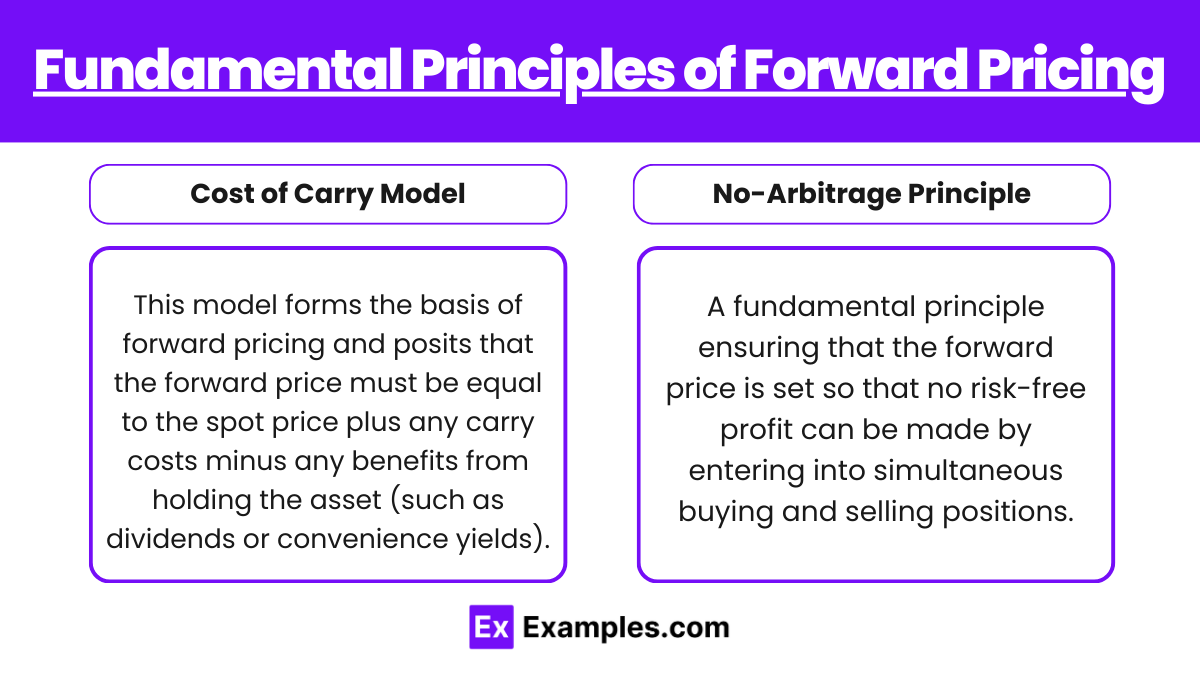

1. Fundamental Principles of Forward Pricing

- Cost of Carry Model: This model forms the basis of forward pricing and posits that the forward price must be equal to the spot price plus any carry costs minus any benefits from holding the asset (such as dividends or convenience yields).

- No-Arbitrage Principle: A fundamental principle ensuring that the forward price is set so that no risk-free profit can be made by entering into simultaneous buying and selling positions.

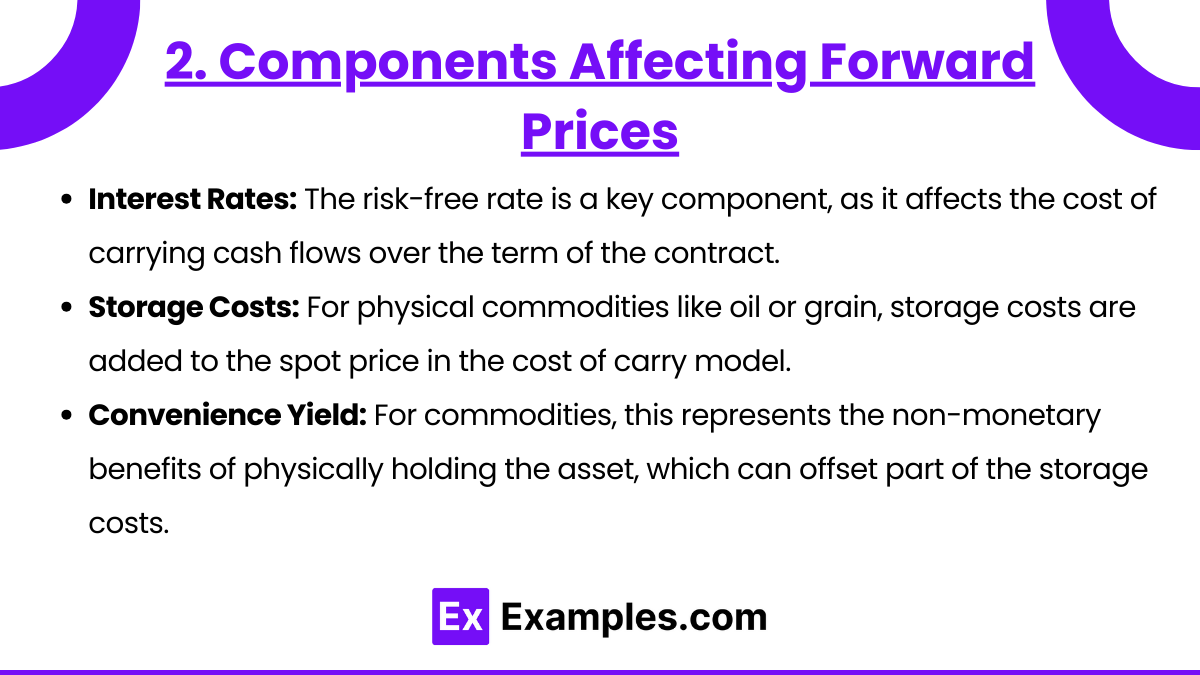

2. Components Affecting Forward Prices

- Interest Rates: The risk-free rate is a key component, as it affects the cost of carrying cash flows over the term of the contract.

- Storage Costs: For physical commodities like oil or grain, storage costs are added to the spot price in the cost of carry model.

- Convenience Yield: For commodities, this represents the non-monetary benefits of physically holding the asset, which can offset part of the storage costs.

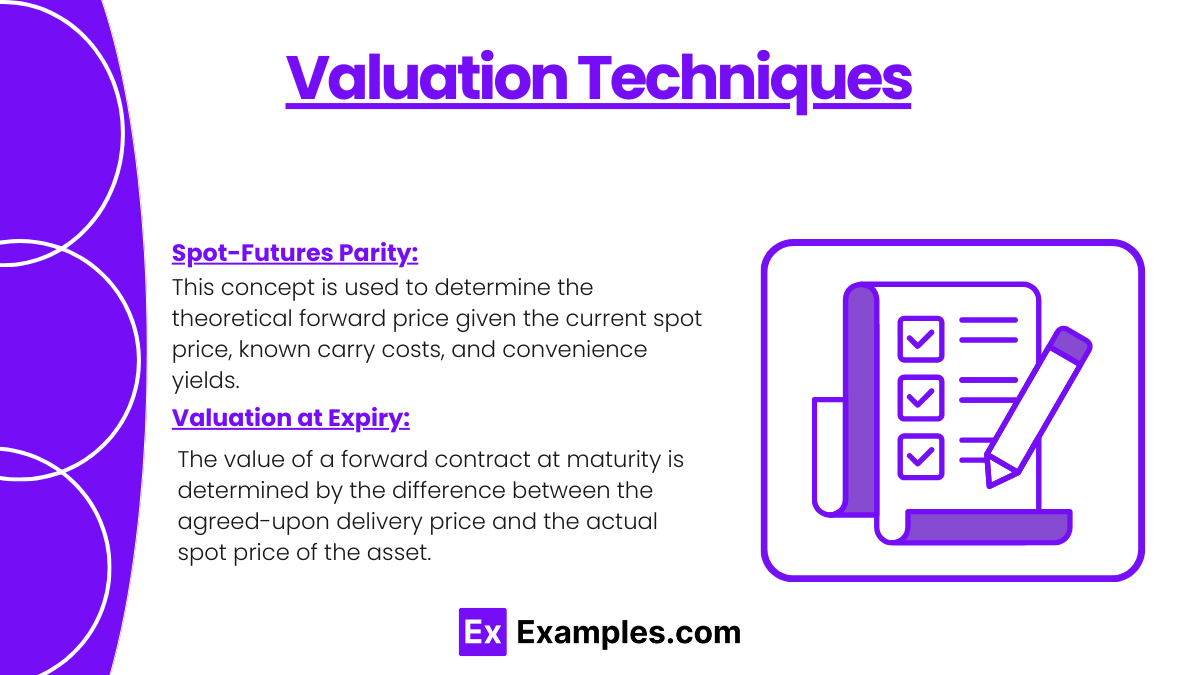

3. Valuation Techniques

- Spot-Futures Parity: This concept is used to determine the theoretical forward price given the current spot price, known carry costs, and convenience yields.

- Valuation at Expiry: The value of a forward contract at maturity is determined by the difference between the agreed-upon delivery price and the actual spot price of the asset.

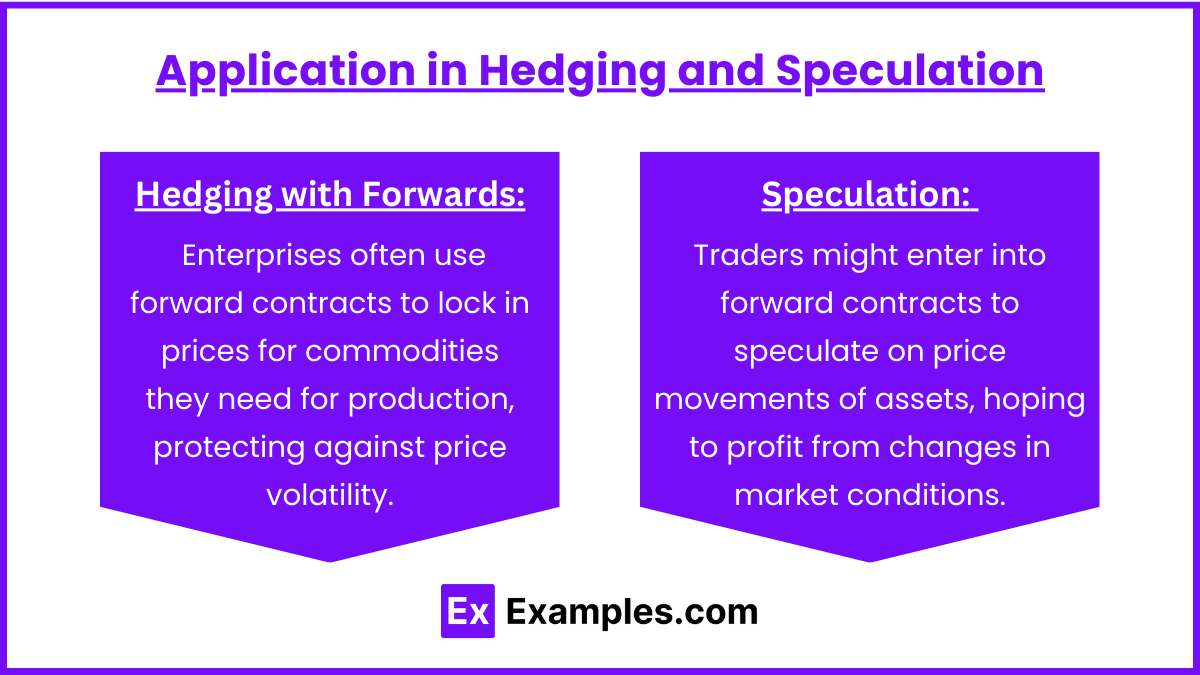

4. Application in Hedging and Speculation

- Hedging with Forwards: Enterprises often use forward contracts to lock in prices for commodities they need for production, protecting against price volatility.

- Speculation: Traders might enter into forward contracts to speculate on price movements of assets, hoping to profit from changes in market conditions.

Examples

Example 1: Hedging Fuel Prices

- An airline uses forward contracts to lock in jet fuel prices for the next year, hedging against potential price increases which could impact operational costs.

Example 2: Agricultural Producer Locking in Prices

- A farmer enters a forward contract to sell a specified amount of grain at a set price at harvest time, reducing the risk of price drops during the growing season.

Example 3: Currency Forward for International Trade

- A U.S. based exporter enters into a forward contract to sell euros it will receive from European customers, locking in the exchange rate to hedge against the euro depreciation.

Example 4: Commodity Trading

- A commodity trader buys a forward contract for gold, speculating that gold prices will rise due to market instability.

Example 5: Valuing Forwards at Maturity

- On the contract’s settlement date, the value of a forward contract in gold is calculated by comparing the market’s current spot price to the contracted forward price.

Practical Questions

Question 1:

What is the primary reason an airline company might use forward contracts?

A) To speculate on fuel prices.

B) To hedge against the risk of rising fuel prices.

C) To invest in fuel commodities.

D) To trade fuel derivatives for profits.

Answer: B) To hedge against the risk of rising fuel prices.

Explanation: Airlines use forward contracts primarily to hedge against the volatility in fuel prices, ensuring budget stability and operational cost management.

Question 2:

Which factor is subtracted from the spot price in the cost of carry model when calculating the forward price?

A) Interest rates

B) Storage costs

C) Convenience yields

D) Inflation rates

Answer: C) Convenience yields

Explanation: In the cost of carry model, convenience yields are subtracted from the spot price because they represent the benefits obtained from physically holding the commodity, which can offset part of the carrying costs.

Question 3:

How is the final settlement value of a forward contract determined at maturity?

A) The difference between the spot price and the forward price.

B) The sum of the spot price and the forward price.

C) The average of the spot price over the life of the contract.

D) The initial forward price adjusted for inflation.

Answer: A) The difference between the spot price and the forward price.

Explanation: At maturity, the value of a forward contract is determined by the difference between the agreed-upon forward price and the actual spot price of the asset, which represents the contract’s payoff or settlement amount.