The Arbitrage Free Valuation Framework

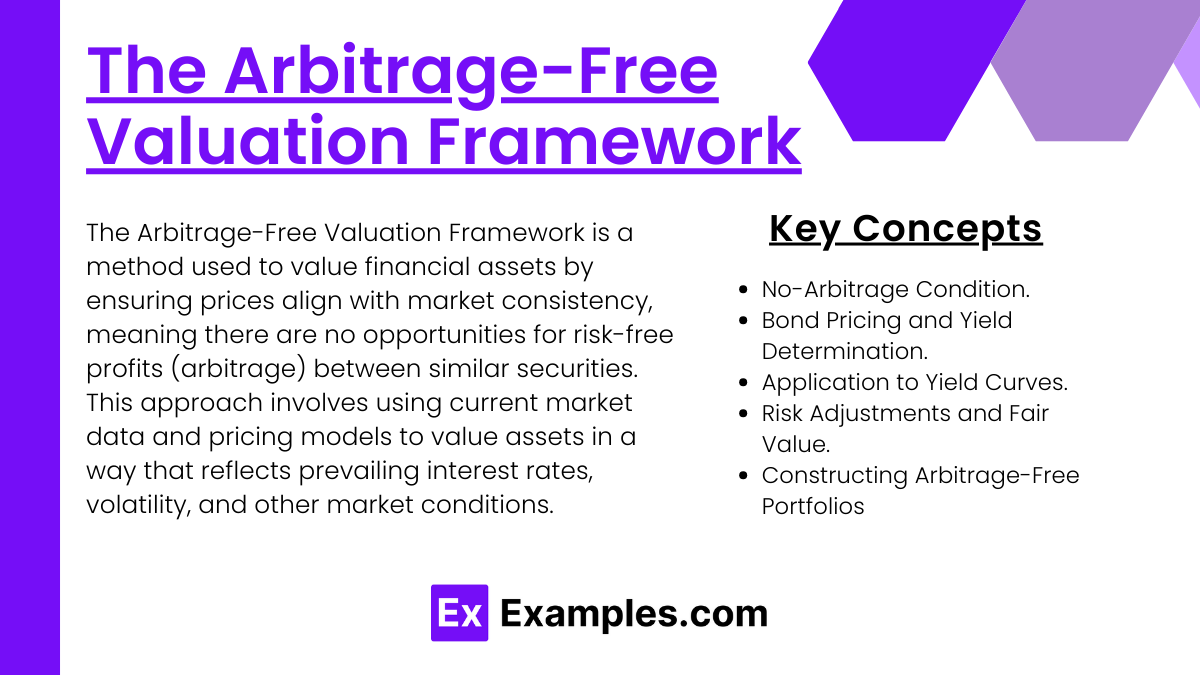

Preparing for the CFA Exam necessitates a thorough grasp of “The Arbitrage-Free Valuation Framework,” a foundational concept in fixed income and bond pricing. This principle ensures that securities are priced in a way that prevents arbitrage opportunities, allowing for fair valuation in efficient markets. Knowledge of this framework, which applies no-arbitrage conditions to the pricing of fixed-income securities, enables candidates to understand and apply valuation techniques that are consistent with market expectations. Mastery of this area empowers candidates to assess bond prices accurately, evaluate yield curves, and incorporate risk adjustments without mispricing. This essential understanding supports the CFA exam goal of analyzing bonds within a consistent valuation model to achieve a high score.

Learning Objectives

In studying “The Arbitrage-Free Valuation Framework” for the CFA, you should aim to understand the essential concepts that ensure securities are valued consistently with market efficiency, leaving no room for arbitrage opportunities. This framework involves applying no-arbitrage conditions to bond pricing, which allows for accurate valuation aligned with fair market expectations. Understanding the arbitrage-free framework enables you to determine bond prices and yields effectively, without mispricing and potential arbitrage exploitation. Mastery of this area allows you to evaluate yield curves, apply risk adjustments, and construct portfolios that align with theoretical valuations, which is crucial for informed and strategic decision-making in investment management.

Key Concepts of “The Arbitrage-Free Valuation Framework”

- No-Arbitrage Condition

- The foundation of the arbitrage-free framework is the no-arbitrage condition. This principle ensures that securities are priced in such a way that no risk-free profits can be earned by exploiting price differences. In a perfectly efficient market, securities that have similar risk and return profiles should be priced similarly, eliminating any arbitrage opportunities.

- In bond pricing, the no-arbitrage condition is enforced by creating replicating portfolios. These portfolios consist of assets or cash flows that match the bond’s cash flows, thereby ensuring that the bond is valued consistently with similar securities.

- Bond Pricing and Yield Determination

- One of the most crucial applications of the arbitrage-free framework is in bond pricing. By using no-arbitrage conditions, investors and analysts can determine bond prices that reflect fair market expectations. This approach prevents bonds from being mispriced, which could lead to arbitrage opportunities.

- The arbitrage-free framework allows for accurate determination of yields by considering the present value of expected cash flows. Yield, a critical measure for investors, indicates the bond’s return, and the framework helps ensure that it reflects the true value of the bond under current market conditions.

- Application to Yield Curves

- The yield curve, which represents the yields of bonds with varying maturities, plays an essential role in bond valuation. The arbitrage-free framework helps in constructing and interpreting yield curves accurately, aligning them with the underlying interest rate environment.

- By ensuring that each point on the yield curve follows the no-arbitrage principle, the framework aids in establishing an accurate yield structure. This approach is fundamental for pricing fixed-income securities and for making comparisons across different bonds and maturities.

- Risk Adjustments and Fair Value

- The arbitrage-free framework also incorporates risk adjustments, aligning bond pricing with the risk level associated with the bond’s cash flows. These adjustments ensure that the valuation reflects not only the cash flows but also the potential risks investors are exposed to.

- Fair value pricing, a result of applying the arbitrage-free principle, allows investors to assess securities based on their intrinsic value, eliminating any discrepancies due to market inefficiencies. This approach is critical for effective portfolio management, as it provides a consistent method for comparing investments.

- Constructing Arbitrage-Free Portfolios

- A fundamental application of the arbitrage-free framework is in portfolio construction. By ensuring that each security within a portfolio adheres to the no-arbitrage condition, investors can create portfolios that align with theoretical valuations, enhancing their strategic investment approach.

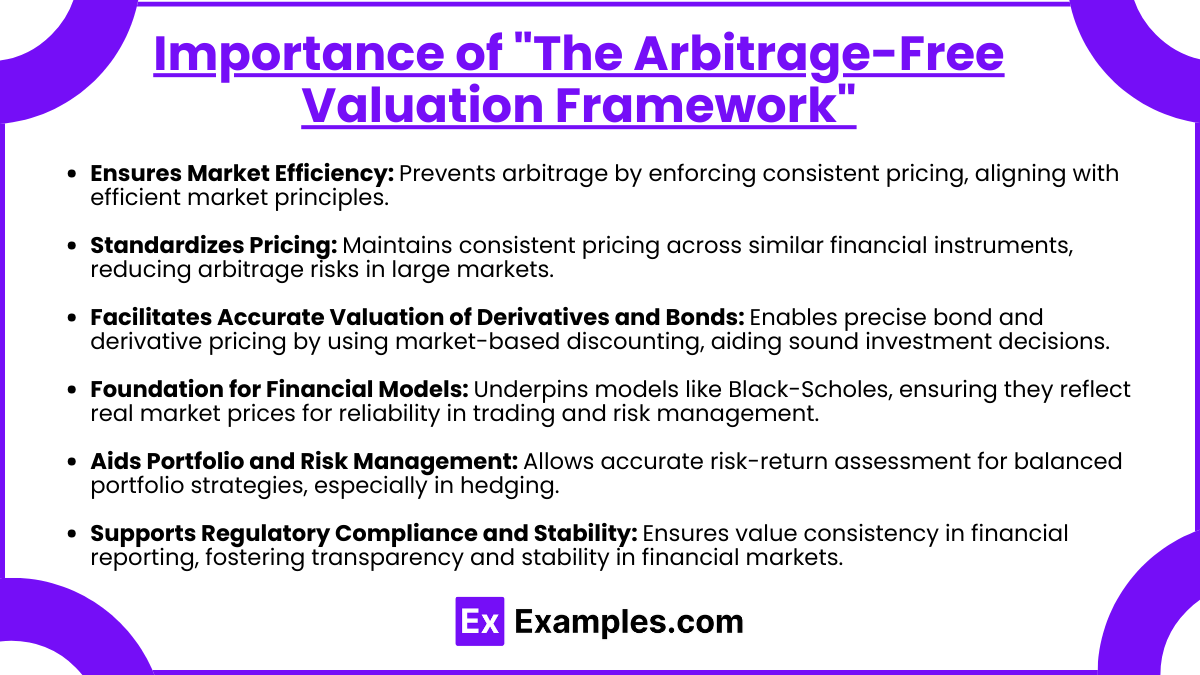

Importance of “The Arbitrage-Free Valuation Framework”

The Arbitrage-Free Valuation Framework is a fundamental concept in finance, particularly in fixed-income and derivatives markets. Its importance lies in providing a consistent method to value financial instruments, ensuring no arbitrage opportunities exist. Here’s an overview of why this framework is essential:

1. Ensures Market Efficiency

- The Arbitrage-Free Valuation Framework upholds market efficiency by eliminating arbitrage opportunities, where risk-free profits could be made from price discrepancies. By enforcing a consistent pricing structure, it prevents the possibility of “free money,” which aligns with efficient market theories and aids in fair market practices.

2. Standardizes Pricing

- This framework helps maintain consistent pricing across financial instruments with similar risk profiles, regardless of differences in maturity, liquidity, or structure. This consistency is vital in large markets, like bond or derivatives markets, where even minor pricing inconsistencies could lead to substantial arbitrage opportunities.

3. Facilitates Accurate Valuation of Derivatives and Bonds

- In fixed-income markets, especially with bonds, the Arbitrage-Free Framework allows for the precise valuation of bonds by discounting future cash flows based on market yields. This prevents pricing distortions, allowing investors to make sound investment decisions.

4. Provides a Foundation for Complex Financial Models

- The framework serves as the foundation for financial models like the Black-Scholes model for options pricing and term structure models for interest rates. It ensures these models remain consistent with real market prices, enhancing their reliability and usefulness for risk management and trading strategies.

5. Aids in Portfolio and Risk Management

- By ensuring consistent valuations, the Arbitrage-Free Framework helps investors accurately assess the risks and returns of their portfolios. It’s essential for strategies that aim to balance returns against risks, particularly in hedging and risk management practices.

6. Supports Regulatory Compliance and Financial Stability

- Many regulatory frameworks use arbitrage-free principles as part of their guidelines for financial reporting, ensuring accurate representation of value across financial statements. This contributes to the broader stability and transparency of financial markets, which is crucial for investor confidence and economic stability.

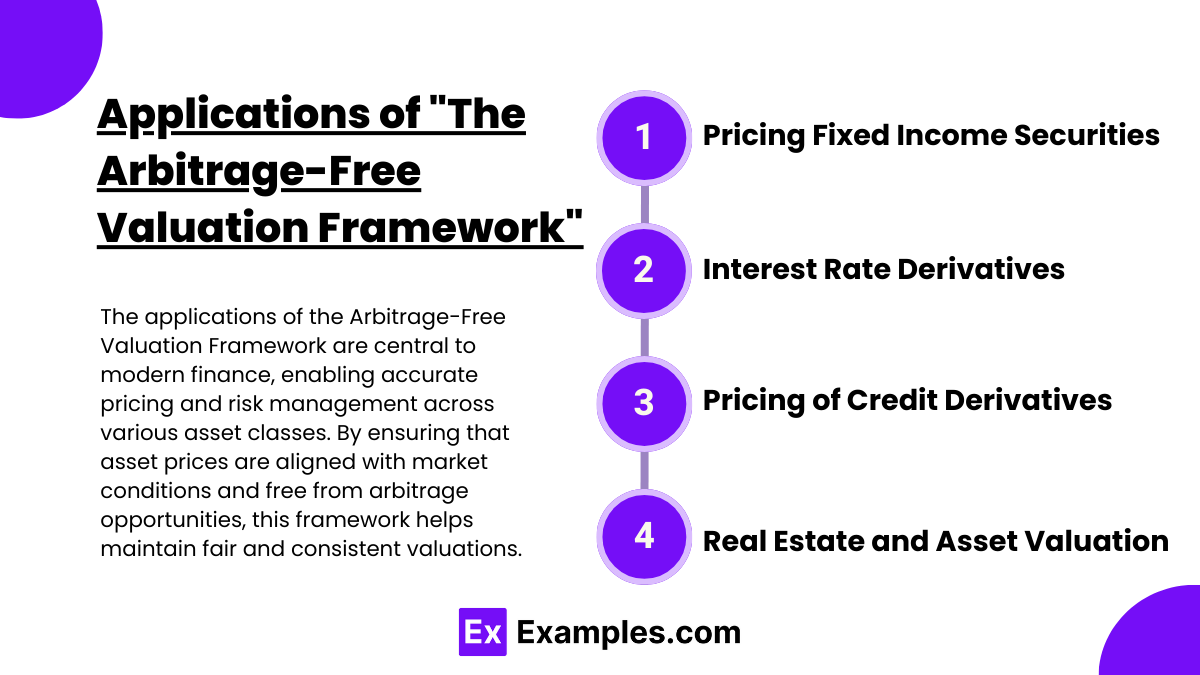

Applications of “The Arbitrage-Free Valuation Framework”

The Arbitrage-Free Valuation Framework is widely used in finance to value assets, especially in fixed income and derivatives markets, ensuring that no arbitrage opportunities (risk-free profit) exist. Below are some applications of this framework:

1. Pricing Fixed Income Securities

- Bonds and Structured Products: Arbitrage-free valuation is fundamental in pricing bonds, bond options, and structured fixed-income products like mortgage-backed securities (MBS) and asset-backed securities (ABS).

- Yield Curve Construction: Using arbitrage-free valuation, market participants can construct yield curves, such as the spot and forward yield curves, to value bonds and interest rate derivatives accurately.

2. Interest Rate Derivatives

- Swaps and Options: For instruments like interest rate swaps, swaptions, caps, and floors, the arbitrage-free valuation framework is essential. It ensures that these products are priced based on the yield curve, with no opportunity for arbitrage.

- Libor Market Models and HJM Framework: Models like the Heath-Jarrow-Morton (HJM) framework use arbitrage-free principles to model interest rate movements and derivatives pricing based on these rates.

3. Pricing of Credit Derivatives

- Credit Default Swaps (CDS): The arbitrage-free framework allows for the fair valuation of CDS by discounting cash flows with credit-adjusted discount rates.

- Credit Spread Curves: Arbitrage-free principles are used to derive credit spread curves that investors use to assess the risk and value of corporate bonds, high-yield bonds, and credit derivatives.

4. Real Estate and Asset Valuation

- Risk-Neutral Valuation: By applying arbitrage-free principles to real estate valuation, cash flows can be discounted with risk-neutral rates, ensuring fair pricing for real estate-backed securities and REITs.

- Project and Asset Appraisal: Arbitrage-free valuation is also used in asset valuation for corporate finance, where it helps assess the present value of future cash flows for various investment projects.

Examples

Example 1. Pricing Fixed-Income Securities

The arbitrage-free valuation framework is essential for pricing fixed-income securities like bonds, where it’s crucial to ensure that prices reflect current market rates and prevent any arbitrage opportunities. By using this framework, investors can determine fair prices for bonds based on yield curves and spot rates, creating consistency across the pricing of similar securities. This method helps maintain the integrity of bond markets, ensuring that no bond can be overpriced or underpriced without creating potential arbitrage opportunities.

Example 2. Valuing Derivatives

In the derivatives market, the arbitrage-free valuation framework helps in pricing options and other derivatives by relying on market conditions and avoiding arbitrage. For instance, by using tools such as binomial trees or Black-Scholes models, this framework ensures that the price of a derivative is based on underlying asset prices, risk-free rates, and other factors. This valuation ensures that investors cannot exploit differences in the price of the derivative versus the underlying asset, keeping the market balanced and fair.

Example 3. Mortgage-Backed Securities (MBS)

When valuing complex instruments like mortgage-backed securities, the arbitrage-free valuation framework provides a way to price these assets in line with market dynamics, taking into account prepayment risks and interest rate changes. By discounting future cash flows based on the current risk-free rate curve, investors ensure that MBS prices accurately reflect their inherent risks. This approach helps avoid pricing inconsistencies and enables investors to make informed decisions without the risk of arbitrage.

Example 4. Asset-Backed Securities (ABS)

For asset-backed securities, the framework is instrumental in valuing cash flows from assets such as loans, credit card receivables, or other collateral pools. The arbitrage-free valuation framework uses a discounting approach based on market interest rates, ensuring that each security reflects the true economic value of its future cash flows. This prevents arbitrage opportunities by ensuring that similar assets are priced consistently with prevailing interest rates, improving transparency and stability in the ABS market.

Example 5. Interest Rate Swaps

In the interest rate swap market, the arbitrage-free valuation framework is used to determine the fair value of a swap contract, where one party exchanges a fixed interest rate payment for a floating rate payment. By applying this framework, investors use the yield curve to value the present value of each leg of the swap. This ensures that the swap’s pricing does not create arbitrage opportunities by aligning it with the expected future rates, making the contract fair for both parties involved.

Practice Questions

Question 1

Which of the following best describes the purpose of the arbitrage-free valuation framework?

A) To determine the exact future prices of securities

B) To ensure that all securities are priced based on intrinsic value only

C) To prevent the existence of risk-free profit opportunities through arbitrage

D) To maximize the profits of institutional investors

Answer: C) To prevent the existence of risk-free profit opportunities through arbitrage

Explanation:

The main purpose of the arbitrage-free valuation framework is to ensure that prices in financial markets do not allow for arbitrage opportunities, which are scenarios where an investor can make a risk-free profit by exploiting price differences. This framework helps ensure that securities are priced based on prevailing market conditions and that no asset or derivative is mispriced in a way that would allow investors to gain without taking on risk. Options A and B are incorrect because the framework does not guarantee future prices or focus solely on intrinsic value. Option D is incorrect because the framework is not designed to maximize profits but rather to maintain fair pricing and market stability.

Question 2

In the arbitrage-free valuation framework, how is the present value of a bond’s cash flows typically determined?

A) By discounting cash flows using a single fixed discount rate

B) By discounting cash flows using the yield curve or spot rates at each cash flow date

C) By using an average of historical interest rates

D) By applying the same discount rate to all bonds, regardless of risk level

Answer: B) By discounting cash flows using the yield curve or spot rates at each cash flow date

Explanation:

The arbitrage-free valuation framework calculates the present value of a bond’s cash flows by using the yield curve or spot rates corresponding to each cash flow date. This approach ensures that the bond is priced according to current market rates at each payment point, preventing arbitrage opportunities. Option A is incorrect because a single fixed rate does not reflect changing market conditions across time. Option C is incorrect because historical rates do not represent current market conditions, and Option D is incorrect because the framework accounts for the unique characteristics of each bond, not a single discount rate.

Question 3

Which of the following is a key assumption underlying the arbitrage-free valuation framework?

A) Market prices are driven solely by supply and demand

B) There is no transaction cost or credit risk in trading financial instruments

C) All investors have the same risk preferences

D) The value of a derivative is independent of the underlying asset’s price

Answer: B) There is no transaction cost or credit risk in trading financial instruments

Explanation:

A key assumption of the arbitrage-free valuation framework is that there are no transaction costs or credit risks in trading. This assumption is necessary for arbitrage opportunities to be purely based on price discrepancies rather than affected by other market frictions. Option A is incorrect as the framework focuses on price consistency rather than market supply and demand alone. Option C is incorrect because investors can have different risk preferences, and Option D is incorrect because the value of a derivative is closely tied to the underlying asset’s price, which directly impacts arbitrage-free valuation.