Topics in Private Wealth Management

Private Wealth Management (PWM) focuses on providing comprehensive financial services to high-net-worth individuals (HNWIs), including investment advice, financial planning, and asset management. The goal of PWM is to meet the unique financial objectives and life goals of these individuals, while addressing concerns related to risk management, tax efficiency, estate planning, and retirement strategies. PWM strategies often involve customized portfolio solutions, estate planning, and integration of client-specific preferences, such as socially responsible investing (SRI) or impact investing. Understanding the intricacies of PWM is essential for managing large portfolios, ensuring effective wealth preservation, and aligning financial strategies with long-term family objectives. This topic also examines regulatory considerations and the role of financial advisors in navigating complex client needs.

Learning Objectives

In studying “Topics in Private Wealth Management” for the CFA, you should learn to assess the unique financial needs and objectives of private clients, including risk tolerance, return expectations, and investment time horizons. Understand the impact of behavioral biases on private wealth management decisions and how to mitigate them. Explore tax implications, estate planning, and philanthropic strategies that align with client goals. Analyze how liquidity constraints, legal considerations, and regulatory issues affect portfolio construction. Evaluate strategies for managing concentrated holdings and succession planning. Additionally, develop proficiency in tailoring asset allocation and investment strategies to meet the individualized goals of private clients, considering factors such as family dynamics and wealth preservation across generations.

Assessing Unique Financial Needs and Objectives of Private Clients

Private clients, particularly high-net-worth individuals (HNWIs), have distinct and often complex financial goals. To create effective wealth management strategies, advisors must gain a thorough understanding of each client’s unique financial needs, risk tolerance, and long-term objectives. Here are the key considerations when assessing these unique financial needs and objectives.

1. Wealth Accumulation and Growth

For many private clients, growing their wealth is a primary objective. This involves not only increasing assets but doing so in a manner aligned with their risk tolerance and investment goals.

- Growth-Oriented Investments: Identifying investments with high growth potential, such as equities, private equity, and venture capital, may suit clients willing to accept higher risk for potential long-term gains.

- Time Horizon: Younger clients or those with a longer investment horizon may prioritize aggressive growth, while clients nearing retirement may opt for more stable growth options.

- Risk Tolerance: Clients with higher risk tolerance may explore diversified growth opportunities, including emerging markets and alternative investments.

Example: A client in their 30s aiming to double their portfolio in 20 years might focus on a portfolio weighted heavily in growth stocks and alternative investments, balanced with some risk management strategies.

2. Wealth Preservation and Capital Protection

Many clients prioritize preserving the wealth they have accumulated, especially as they approach retirement or after they have achieved a certain level of wealth.

- Conservative Allocation: A focus on low-volatility assets such as bonds, dividend-paying stocks, and real estate can help protect capital.

- Inflation Protection: Strategies such as incorporating Treasury Inflation-Protected Securities (TIPS) or real assets like real estate can preserve purchasing power.

- Diversification: By spreading investments across asset classes and geographic regions, clients can reduce exposure to market-specific risks.

Example: A retired client may hold a portfolio with 40% in bonds, 30% in dividend stocks, and 30% in real estate to protect capital while generating stable income.

3. Tax Efficiency and Minimization

Efficient tax planning is essential for HNWIs who often face higher tax burdens. Managing tax obligations allows clients to retain more of their wealth and maximize returns.

- Tax-Advantaged Accounts: Placing tax-inefficient assets in tax-deferred accounts (IRAs, 401(k)s) and tax-efficient assets in taxable accounts optimizes tax treatment.

- Tax-Loss Harvesting: Selling underperforming investments to offset capital gains helps reduce overall tax liability.

- Gifting and Charitable Contributions: Clients with philanthropic goals can reduce taxable income through charitable donations or setting up donor-advised funds.

Example: A high-income client may place dividend-paying stocks in a retirement account to defer taxes, while holding tax-efficient index funds in a taxable account to reduce tax exposure.

4. Estate and Legacy Planning

Many private clients wish to create a legacy, ensuring their wealth benefits future generations or supports charitable causes.

- Trusts and Wills: Establishing trusts allows clients to control the distribution of their assets, protect against estate taxes, and ensure smooth asset transfer to heirs.

- Philanthropy: For clients interested in charitable giving, options such as donor-advised funds, charitable trusts, or private foundations offer tax benefits and support personal values.

- Succession Planning: Business owners may require succession planning to ensure their business is managed or transferred according to their wishes.

Example: A client with substantial assets may set up a trust to pass wealth to heirs while minimizing estate taxes and creating a charitable fund for ongoing giving.

5. Retirement and Lifestyle Planning

Maintaining a desired lifestyle in retirement requires careful planning, especially for clients with specific lifestyle goals.

- Income Generation: Creating a portfolio of income-generating assets like bonds, dividend stocks, and annuities ensures a steady income stream in retirement.

- Longevity Planning: Ensuring assets last throughout retirement may involve balancing growth investments with income stability, addressing longevity risks.

- Withdrawal Strategy: Strategies such as the “4% rule” or “bucket approach” help manage withdrawals to sustain the client’s lifestyle without depleting savings.

Example: A client who wants to retire comfortably may prioritize a balanced portfolio of bonds and income-generating assets that provides regular income while preserving capital.

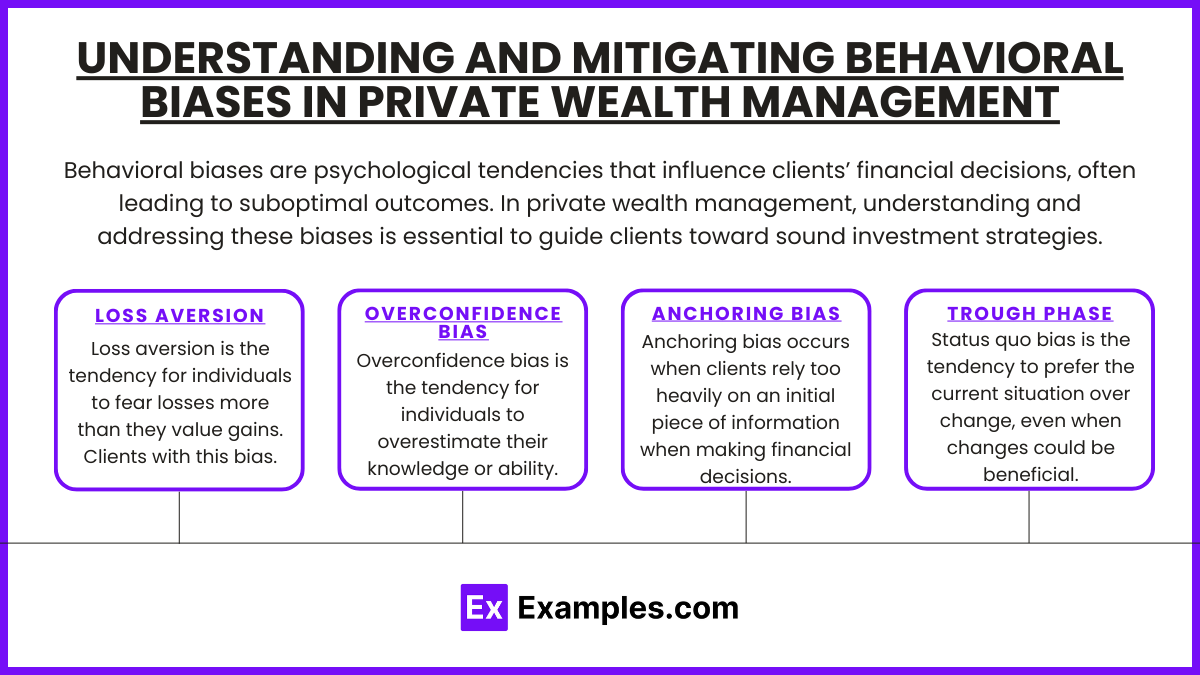

Understanding and Mitigating Behavioral Biases in Private Wealth Management

Behavioral biases are psychological tendencies that influence clients’ financial decisions, often leading to suboptimal outcomes. In private wealth management, understanding and addressing these biases is essential to guide clients toward sound investment strategies, aligned with their long-term goals. By recognizing and mitigating behavioral biases, wealth managers help clients make rational, well-informed decisions, particularly during periods of market volatility or personal uncertainty. Here’s an overview of common behavioral biases and effective strategies to manage them.

1. Loss Aversion

Loss aversion is the tendency for individuals to fear losses more than they value gains. Clients with this bias often become overly cautious, avoiding necessary risks and missing out on potential growth opportunities.

- Impact: Loss aversion can lead clients to focus too heavily on short-term losses and become overly conservative, even when their investment strategy calls for higher-risk, higher-return assets. This often results in an under-diversified portfolio that doesn’t support long-term goals.

- Mitigation Strategy: Wealth managers can use scenario analysis to show clients the long-term impact of a balanced, diversified portfolio and how temporary losses are often offset by gains over time. Creating “mental accounts,” such as separating assets for short-term versus long-term goals, also helps clients compartmentalize risk in a way that feels safer.

Example: For a client overly worried about short-term losses, a wealth manager could allocate a conservative portion to cash or bonds for short-term needs, while investing the remainder in equities to support long-term growth.

2. Overconfidence Bias

Overconfidence bias is the tendency for individuals to overestimate their knowledge or ability to predict market movements. This often leads clients to make impulsive decisions, such as frequent trading or attempting to time the market.

- Impact: Overconfident clients may engage in excessive trading, leading to higher transaction costs, increased tax liabilities, and suboptimal returns due to impulsive decisions rather than following a well-thought-out strategy.

- Mitigation Strategy: Wealth managers can provide historical data showing the pitfalls of market timing and excessive trading, illustrating how a disciplined, long-term approach often yields better results. Setting clear, measurable goals helps overconfident clients stay committed to a structured plan and resist impulsive trading.

Example: A wealth manager might encourage an overconfident client to track the performance of hypothetical market timing decisions versus a buy-and-hold approach, highlighting the benefits of a consistent strategy.

3. Anchoring Bias

Anchoring bias occurs when clients rely too heavily on an initial piece of information (such as a stock’s previous high price) when making financial decisions. This can result in an unrealistic expectation of asset performance.

- Impact: Anchoring can lead clients to hold onto underperforming assets, hoping they’ll return to a specific “anchor” value, or cause them to set arbitrary goals based on past data rather than realistic projections.

- Mitigation Strategy: Wealth managers can help clients set realistic expectations by focusing on fundamental analysis rather than historical price levels. By regularly reviewing the portfolio’s current and future potential, wealth managers help clients adjust their perspective to align with changing market conditions.

Example: If a client is anchored to a stock’s previous high, a wealth manager might provide an analysis of the stock’s fundamentals, demonstrating why it may or may not reach that value again, encouraging rational decision-making.

4. Status Quo Bias

Status quo bias is the tendency to prefer the current situation over change, even when changes could be beneficial. Clients with this bias may resist rebalancing their portfolio or hesitate to adapt to changing market conditions.

- Impact: Status quo bias can result in an outdated asset allocation that doesn’t reflect the client’s evolving risk tolerance or market environment, potentially leading to missed opportunities or unnecessary risk.

- Mitigation Strategy: Wealth managers can review the portfolio regularly with the client, explaining how rebalancing aligns with their long-term goals. Visual tools that show the impact of rebalancing over time can help clients see the benefits of making necessary adjustments.

Example: For a client reluctant to rebalance, a wealth manager might use a hypothetical model to show how rebalancing would have improved performance in previous market cycles.

Exploring Tax Implications, Estate Planning, and Philanthropic Strategies

Effective private wealth management encompasses more than investment growth; it involves strategic planning in areas such as taxation, estate management, and philanthropic giving. Each of these areas requires a tailored approach to optimize wealth transfer, reduce tax burdens, and support personal values or legacy goals.

1. Tax Implications in Wealth Management

Understanding and managing tax implications are fundamental to preserving and maximizing wealth. Private wealth management includes strategies to reduce the impact of income taxes, capital gains taxes, and estate taxes.

- Tax-Efficient Investment Strategies: By carefully selecting the types of accounts (taxable vs. tax-deferred), wealth managers can structure portfolios to minimize taxes on interest, dividends, and capital gains. For example, holding tax-efficient investments like ETFs or index funds in taxable accounts, while placing tax-inefficient assets (e.g., bonds or REITs) in tax-advantaged accounts, can significantly reduce the tax burden.

- Capital Gains Management: To manage capital gains taxes, wealth managers employ tax-loss harvesting by offsetting gains with losses from other investments. They also consider holding periods, as long-term capital gains are typically taxed at lower rates than short-term gains.

- Wealth Transfer and Estate Tax Reduction: For high-net-worth individuals, estate taxes can significantly reduce the value of inherited assets. Wealth managers often use gifting strategies, trusts, and tax-efficient account structuring to lower the taxable estate, preserving wealth for future generations.

Example: A client with a high income may use a mix of tax-advantaged retirement accounts and taxable accounts. High-growth assets could be held in tax-deferred accounts to delay taxes, while tax-efficient funds are kept in taxable accounts to minimize capital gains taxes.

2. Estate Planning for Wealth Preservation and Transfer

Estate planning is essential for protecting assets, ensuring wealth is distributed according to the client’s wishes, and reducing taxes and legal expenses. Estate planning strategies involve structuring wealth transfers, setting up trusts, and implementing legal tools to meet long-term goals.

- Trusts: Trusts are effective tools for minimizing estate taxes, protecting assets, and managing wealth distribution. Revocable trusts allow clients to retain control over assets during their lifetime, while irrevocable trusts remove assets from the taxable estate, potentially reducing estate taxes. Other specialized trusts, like charitable trusts, support both philanthropic and tax-saving goals.

- Gifting Strategies: Lifetime gifting strategies allow clients to reduce their taxable estate by transferring wealth gradually over time. Annual gifts to family members, using the annual gift tax exclusion, help reduce estate size without incurring taxes.

- Family Business Succession Planning: For clients with family-owned businesses, succession planning is crucial to ensure the business can transition smoothly to the next generation. Wealth managers coordinate with legal and financial professionals to create a succession plan that minimizes taxes and ensures continuity.

Example: A client with substantial assets may set up an irrevocable trust to remove assets from their estate, reducing estate taxes, while still allowing the client to specify the terms of distribution to heirs.

3. Philanthropic Strategies and Charitable Giving

Philanthropy is often a significant goal for high-net-worth individuals, both as a way to support meaningful causes and as a strategy for reducing taxable income. Philanthropic planning in wealth management aligns charitable goals with financial strategies, optimizing tax benefits.

- Charitable Trusts: Trusts like charitable remainder trusts (CRTs) or charitable lead trusts (CLTs) allow clients to make a gift to charity, receive an income stream, and benefit from tax deductions. CRTs, for example, allow clients to donate assets to a trust that provides them with income for life, after which the remaining assets go to charity.

- Donor-Advised Funds (DAFs): A DAF allows clients to make a charitable contribution and receive an immediate tax deduction while retaining the flexibility to direct donations to specific charities over time. This provides control and flexibility, with the tax benefits of a charitable gift.

- Direct Charitable Contributions: Direct donations of appreciated securities or real estate are tax-efficient, as they allow clients to avoid capital gains taxes on the appreciated value. This strategy also enables clients to deduct the full fair market value of the assets, maximizing the tax benefit.

- Foundations: Some clients may establish a private foundation to support long-term philanthropic goals. Foundations provide control over charitable activities and allow families to create a legacy, though they come with administrative and regulatory requirements.

Example: A client interested in supporting education might set up a charitable remainder trust that provides income during their lifetime, with the remaining assets going to a scholarship fund after they pass.

Analyzing Liquidity Constraints, Legal Considerations, and Regulatory Issues

In private wealth management, understanding and addressing liquidity constraints, legal considerations, and regulatory issues are essential for creating effective financial strategies for clients. These factors can significantly impact investment decisions, portfolio structure, and the overall wealth management plan. Let’s delve into each of these areas to explore their implications and the strategies wealth managers use to address them.

1. Liquidity Constraints

Liquidity refers to the ease with which assets can be converted into cash without significantly impacting their value. Private clients, particularly high-net-worth individuals (HNWIs), may have complex liquidity needs that wealth managers must address carefully.

- Immediate Cash Flow Needs: Clients may need liquidity to cover regular expenses, taxes, or unforeseen financial obligations. Ensuring that a portion of the portfolio remains in liquid assets (e.g., cash, money market funds, short-term bonds) is crucial for meeting these needs without disrupting the broader investment strategy.

- Planned Major Purchases: For clients planning significant expenditures (e.g., buying property, business investments, or luxury purchases), wealth managers allocate sufficient liquid assets to avoid the need for sudden portfolio adjustments. Funds are typically placed in low-risk, highly liquid assets to ensure cash availability when needed.

- Illiquid Investments: Private clients often hold illiquid assets like real estate, private equity, and hedge funds, which may offer higher returns but are challenging to liquidate quickly. Wealth managers must balance these assets with liquid investments to provide flexibility while meeting the client’s risk tolerance and return objectives.

Strategy: Wealth managers use a “liquidity bucket” approach, categorizing assets based on liquidity levels. Short-term liquidity needs are covered by cash and near-cash assets, while long-term goals may involve illiquid assets to enhance returns.

Example: A client with significant real estate holdings may keep 20-30% of their portfolio in liquid assets, ensuring they can access funds for unexpected expenses or market opportunities without selling property assets.

2. Legal Considerations

Legal considerations play a significant role in wealth management, as clients must navigate complex issues related to estate planning, asset protection, and succession. Understanding these factors allows wealth managers to provide solutions that align with legal requirements and protect client assets.

- Estate Planning: Effective estate planning involves setting up wills, trusts, and other legal structures to ensure assets are distributed according to the client’s wishes. Trusts (e.g., revocable, irrevocable, family trusts) provide asset protection, minimize estate taxes, and help avoid probate.

- Asset Protection: Legal structures, such as family limited partnerships or LLCs, protect assets from potential creditors and lawsuits. These tools are crucial for clients in professions with high liability exposure or those with significant personal wealth at risk.

- Succession Planning: For business owners and clients with significant family assets, succession planning ensures a smooth transition of wealth or business interests to heirs. Legal considerations include structuring ownership transfers, establishing governance for family wealth, and minimizing taxes.

Strategy: Wealth managers collaborate with estate attorneys and tax advisors to design legally sound strategies that align with the client’s goals. Structuring assets through trusts, family partnerships, or LLCs provides control, tax efficiency, and asset protection.

Example: A business owner might establish a family trust to transfer business ownership to heirs gradually, ensuring continuity while minimizing estate taxes and protecting assets from potential liabilities.

3. Regulatory Issues

Regulatory issues are particularly relevant in private wealth management, as compliance with tax laws, securities regulations, and fiduciary standards is essential for both wealth managers and clients. Regulatory changes can affect everything from investment strategies to estate planning structures.

- Tax Compliance: For clients with complex portfolios or international assets, staying compliant with tax regulations is essential. Regulatory issues include managing capital gains taxes, understanding foreign income and asset reporting (e.g., FATCA, CRS), and navigating estate tax laws.

- Investment and Securities Regulations: Wealth managers must comply with regulations governing securities investments, such as those set by the SEC or FINRA. This compliance ensures transparency, fairness, and the protection of client assets. Wealth managers must also understand how these rules impact investment choices, particularly for alternative investments and international securities.

- Fiduciary Standards: Wealth managers often operate under fiduciary duty, meaning they must act in the client’s best interest. Regulatory standards define fiduciary responsibilities, requiring wealth managers to avoid conflicts of interest, disclose fees transparently, and prioritize clients’ needs in all recommendations.

Strategy: Wealth managers keep updated on regulatory changes and collaborate with legal and tax professionals to ensure compliance. Proactively adapting to changes in tax laws, securities regulations, and fiduciary standards helps protect clients and mitigate potential legal or financial risks.

Example: A client with overseas investments may work with a wealth manager to ensure all assets are reported under FATCA and CRS regulations, avoiding penalties while maintaining tax efficiency.

Examples

Example 1: Investment Strategy Development

Private wealth management involves creating personalized investment strategies tailored to the individual needs and goals of high-net-worth clients. This process includes assessing the client’s risk tolerance, financial objectives, and time horizon. Wealth managers often diversify investments across asset classes, such as equities, fixed income, real estate, and alternative investments, to optimize returns while managing risk.

Example 2: Tax Optimization and Estate Planning

Effective tax management is a critical component of private wealth management. Wealth managers help clients develop strategies to minimize tax liabilities through various methods, such as tax-efficient investment vehicles and charitable giving strategies. Additionally, estate planning ensures that clients’ wealth is transferred according to their wishes, minimizing estate taxes and facilitating a smooth transition of assets to heirs.

Example 3: Retirement Planning

Ensuring financial security during retirement is a key focus of private wealth management. Wealth managers assist clients in determining how much capital they need to sustain their lifestyle post-retirement, analyzing various income sources, such as pensions, Social Security, and investment returns. This includes developing a withdrawal strategy to maximize the longevity of retirement funds while considering healthcare costs and inflation.

Example 4: Risk Management and Insurance Solutions

Private wealth managers assess potential risks that could impact a client’s financial well-being and recommend appropriate insurance products to mitigate those risks. This may include life insurance, disability insurance, and long-term care insurance. By identifying and addressing these risks, wealth managers help clients protect their assets and ensure their financial stability over the long term.

Example 5: Philanthropic Planning

Many high-net-worth individuals seek to make a positive impact through philanthropy. Private wealth management encompasses developing philanthropic strategies that align with the client’s values and goals. Wealth managers may assist clients in establishing charitable foundations, donor-advised funds, or direct donations to nonprofit organizations. This planning ensures that philanthropic efforts are structured effectively to maximize impact while also considering tax benefits.

Practice Questions

Question 1

Which of the following is a primary objective in developing an investment strategy for a private wealth client?

A) Maximizing returns without regard to risk

B) Aligning investments with the client’s risk tolerance and financial goals

C) Avoiding diversification across asset classes

D) Minimizing the time spent on portfolio management

Correct Answer: B) Aligning investments with the client’s risk tolerance and financial goals.

Explanation: In private wealth management, the primary objective of an investment strategy is to align investments with the client’s specific risk tolerance, financial goals, and time horizon. This personalized approach ensures that the strategy meets the client’s long-term objectives. Options A, C, and D are incorrect as they overlook the importance of risk management, diversification, and a personalized approach in wealth management.

Question 2

Which of the following is a common approach to minimize tax liabilities in private wealth management?

A) Investing solely in high-growth stocks

B) Implementing tax-efficient investment vehicles

C) Avoiding any charitable giving

D) Focusing exclusively on short-term investments

Correct Answer: B) Implementing tax-efficient investment vehicles.

Explanation: Tax-efficient investment vehicles, such as municipal bonds, retirement accounts, and tax-deferred accounts, are commonly used in private wealth management to reduce tax liabilities. This allows clients to retain more of their investment returns. Options A, C, and D do not focus on tax efficiency, and short-term investments may increase taxable events due to capital gains tax.

Question 3

What is the purpose of estate planning in private wealth management?

A) To manage a client’s day-to-day expenses

B) To ensure assets are distributed according to the client’s wishes and to minimize estate taxes

C) To eliminate the need for insurance

D) To reduce the client’s investment portfolio size

Correct Answer: B) To ensure assets are distributed according to the client’s wishes and to minimize estate taxes.

Explanation: Estate planning in private wealth management aims to ensure that a client’s assets are distributed according to their wishes after their passing, while minimizing estate taxes and legal complications for heirs. This helps to preserve wealth for future generations. Options A, C, and D do not accurately reflect the goals of estate planning, which is focused on legacy and tax efficiency rather than daily expenses, insurance needs, or reducing portfolio size.