Using Multifactor Models

Preparing for the CFA exam requires a strong grasp of multifactor models, a key component of portfolio management and risk analysis. Mastery of these models, including the Capital Asset Pricing Model (CAPM) and Fama-French models, enables investors to identify risk factors, understand asset returns, and enhance diversification, crucial for optimizing investment performance.

Learning Objective

In studying "Using Multifactor Models" for the CFA exam, you should learn to understand the application of multifactor models to assess asset returns and risk exposures. Analyze various models, including the Capital Asset Pricing Model (CAPM), Arbitrage Pricing Theory (APT), and Fama-French factors, focusing on their use in identifying systematic risk drivers. Evaluate how these models explain return variability, capture market anomalies, and enhance portfolio diversification and optimization. Additionally, explore their practical applications in risk management, performance attribution, and investment decision-making, and apply your knowledge to interpret factor-based analyses and asset pricing within CFA practice scenarios.

Introduction to Multifactor Models

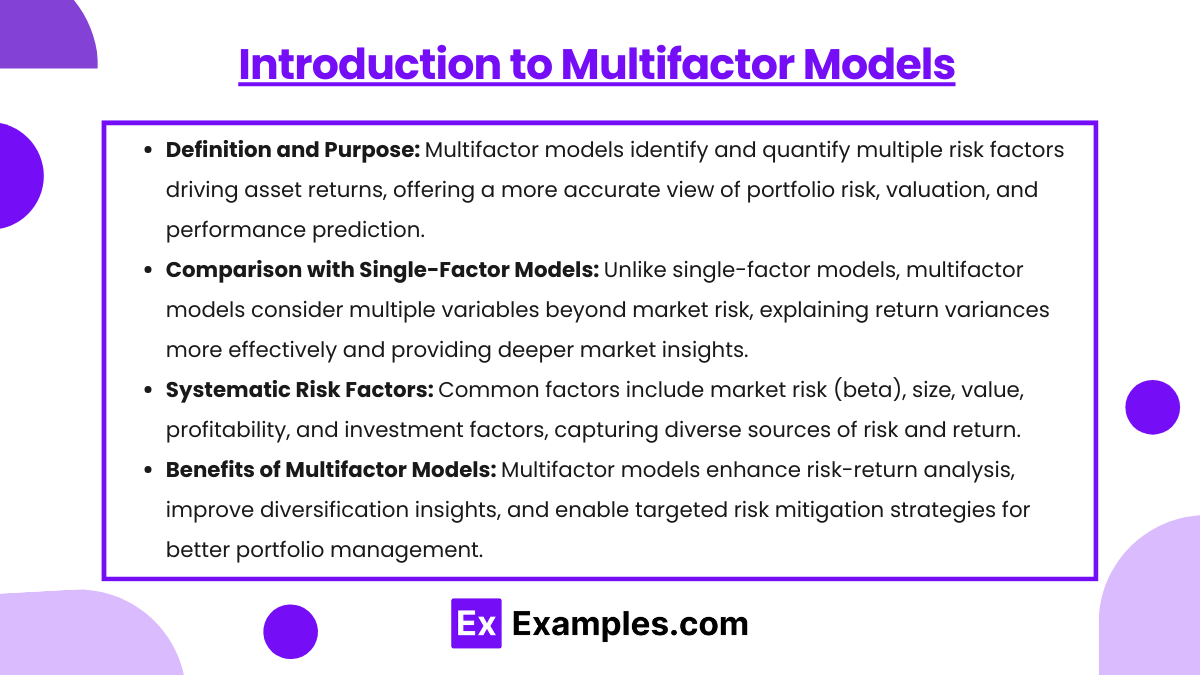

Multifactor models are financial tools designed to explain asset returns by considering multiple sources of risk and factors that influence market performance. Unlike single-factor models like the Capital Asset Pricing Model (CAPM), which only accounts for market risk (beta), multifactor models consider several systematic factors that impact asset returns and risk exposures.

Definition and Purpose

Multifactor models aim to capture the complex relationships that drive asset returns by identifying and quantifying various risk factors. This provides a more accurate and holistic understanding of portfolio risk and expected returns, enabling better asset valuation, risk management, and performance prediction.

Comparison with Single-Factor Models

While single-factor models focus solely on market risk and assume a linear relationship with returns, multifactor models address the limitations of single-factor approaches by including additional variables. These variables, or factors, can explain return variances and capture nuances in market behavior more effectively, making them valuable for understanding asset performance in a diverse market environment.

Systematic Risk Factors and Examples

Multifactor models often incorporate multiple systematic risk factors, such as:

Market Risk (Beta): Measures an asset’s sensitivity to overall market movements.

Size Factor: Reflects the tendency for smaller companies to outperform larger ones over time.

Value Factor: Captures the premium associated with undervalued stocks, typically represented by high book-to-market ratios.

Profitability and Investment Factors: Included in extended models like the Fama-French Five-Factor Model to capture additional sources of risk and return variance.

Benefits of Using Multifactor Models

Enhanced Risk-Return Analysis: Provides a deeper understanding of what drives portfolio performance.

Diversification Insights: Identifies how different factors contribute to portfolio diversification.

Risk Mitigation: Enables investors to manage exposure to specific risk factors through targeted strategies.

In summary, multifactor models provide a comprehensive approach to understanding and managing asset returns by incorporating a range of factors that affect market behavior, making them

Types of Multifactor Models

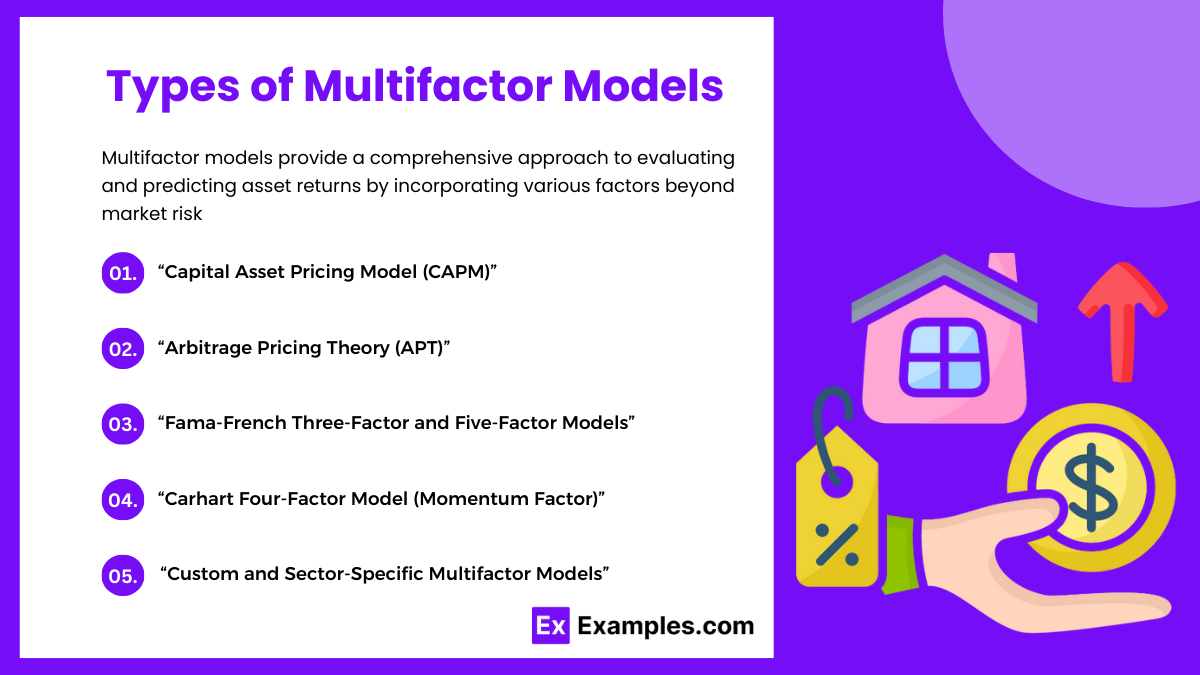

Multifactor models provide a comprehensive approach to evaluating and predicting asset returns by incorporating various factors beyond market risk. Each type of multifactor model has distinct characteristics, assumptions, and applications, making them useful for different investment objectives. Here is an explanation of some key types:

1. Capital Asset Pricing Model (CAPM)

Overview: CAPM is considered the simplest form of a multifactor model, though it technically involves only a single market risk factor. It establishes the relationship between expected return and market risk (beta).

Application: The model calculates the expected return of an asset based on its beta (systematic risk relative to the market) and the risk-free rate, plus a market risk premium. CAPM serves as a foundational tool for comparing multifactor approaches.

Limitations: CAPM assumes that only market risk influences asset returns, ignoring other significant factors like size and value.

2. Arbitrage Pricing Theory (APT)

Overview: Unlike CAPM, APT is a true multifactor model that does not rely on a single market index. Instead, it considers multiple macroeconomic factors or theoretical factors that affect asset returns.

Factors: Examples may include inflation, interest rates, GDP growth, and oil prices. APT assumes that any mispricing in securities will be corrected by arbitrage opportunities.

Application: APT is more flexible than CAPM, allowing for a broader and customizable approach to risk factors relevant to different assets or market conditions.

3. Fama-French Three-Factor and Five-Factor Models

Three-Factor Model: This model expands on CAPM by adding two additional factors—size (small-cap vs. large-cap) and value (high book-to-market ratio vs. low). The size premium suggests that smaller companies tend to outperform larger ones, while the value premium indicates that value stocks often outperform growth stocks.

Five-Factor Model: In addition to the market, size, and value factors, this model introduces profitability (robust vs. weak profitability) and investment (aggressive vs. conservative investment strategies) as factors that impact asset returns.

Application: These models are widely used for asset pricing and evaluating portfolio performance.

4. Carhart Four-Factor Model (Momentum Factor)

Overview: This model builds on the Fama-French Three-Factor Model by adding a momentum factor, which accounts for the tendency of stocks that have performed well in the past to continue to outperform.

Application: The Carhart model is useful for explaining performance variations related to price momentum, which can be a significant driver of returns in certain markets.

5. Custom and Sector-Specific Multifactor Models

Overview: Many investors and institutions develop custom models tailored to specific investment goals, sectors, or industries. These models may incorporate factors such as geopolitical risk, sector-specific drivers, or ESG (Environmental, Social, and Governance) factors.

Application: Custom models allow for a more nuanced analysis of risk and return factors that are unique to specific investment contexts.

In summary, multifactor models range from foundational models like CAPM to more sophisticated approaches like APT and the Fama-French models.

Application and Analysis of Multifactor Models

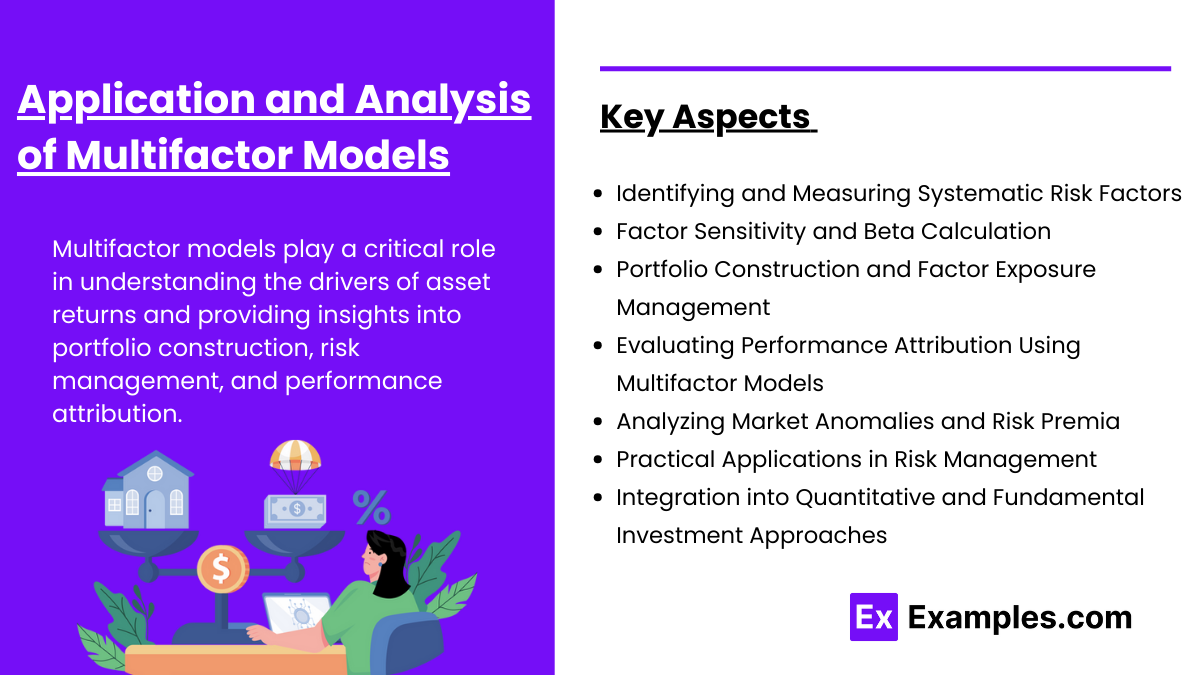

Multifactor models play a critical role in understanding the drivers of asset returns and providing insights into portfolio construction, risk management, and performance attribution. By analyzing the impact of multiple factors on an asset’s performance, investors and analysts can better assess risk exposure, optimize returns, and make more informed investment decisions.

1. Identifying and Measuring Systematic Risk Factors

Multifactor models help identify systematic risk factors that influence asset returns, such as market risk, size, value, profitability, momentum, and other macroeconomic variables. By measuring exposure to these factors, investors can better understand what drives the performance of an asset or portfolio.

For example, a portfolio with high exposure to the size factor may be more sensitive to movements in small-cap stocks, while exposure to value factors may indicate sensitivity to undervalued assets.

2. Factor Sensitivity and Beta Calculation

Multifactor models use betas to measure an asset’s sensitivity to specific factors. For example, in the Fama-French Three-Factor Model, betas are used to quantify the degree to which an asset is exposed to market risk, size (small-cap vs. large-cap), and value (high book-to-market ratio).

Understanding these sensitivities allows investors to adjust their portfolios based on expected factor movements and market conditions.

3. Portfolio Construction and Factor Exposure Management

Multifactor models are used to construct and optimize portfolios by aligning exposure to desired risk factors. For instance, an investor may build a portfolio with a tilt towards value and small-cap factors based on historical data suggesting strong risk-adjusted returns.

Diversifying exposure across multiple factors can reduce overall portfolio risk while improving expected returns. Multifactor models provide a framework for achieving a more balanced risk-return profile.

4. Evaluating Performance Attribution Using Multifactor Models

Performance attribution analysis helps determine the sources of a portfolio's returns relative to a benchmark. By comparing actual returns to predicted returns based on factor exposures, investors can assess whether performance was driven by market movements, specific factor bets, or active management decisions.

Multifactor performance attribution enables investors to separate skill from luck in portfolio management.

5. Analyzing Market Anomalies and Risk Premia

Multifactor models help explain and exploit market anomalies such as the value premium, size effect, and momentum effect. These models provide insight into why certain stocks or asset classes may outperform others based on risk premia associated with specific factors.

Investors can use this information to develop strategies that capture these premia, enhancing portfolio performance.

6. Practical Applications in Risk Management

Multifactor models allow for targeted risk management by isolating and managing exposures to specific factors. For example, an investor concerned about market downturns may hedge market risk while maintaining exposure to value or momentum factors that may perform differently.

By understanding the sources of risk and how they interact, investors can take proactive steps to mitigate unwanted risk while preserving upside potential.

7. Integration into Quantitative and Fundamental Investment Approaches

Multifactor models are widely used in both quantitative and fundamental strategies. Quantitative investors may rely on data-driven models to construct portfolios based on factor exposures, while fundamental analysts use multifactor models to gain a deeper understanding of a company's risk and expected return characteristics.

Practical Uses in Risk Management and Investment Decisions

Multifactor models have significant applications in risk management and investment decisions, allowing investors to enhance portfolio construction, optimize returns, and manage risks more effectively. By understanding and utilizing multiple factors that influence asset performance, investors can make better-informed decisions that align with their investment goals and risk tolerance. Here’s how multifactor models are practically used:

1. Risk Mitigation Strategies through Factor-Based Analysis

Multifactor models enable investors to isolate and manage exposure to specific risk factors. For instance, by identifying the factors driving portfolio volatility (e.g., market, size, value), investors can take measures to reduce unwanted risks through diversification, hedging strategies, or adjustments to asset allocation.

For example, if a portfolio is overexposed to market risk, investors may add assets that are less correlated with overall market movements to reduce total portfolio volatility.

2. Enhancing Portfolio Diversification Using Multifactor Insights

Multifactor models provide insights into how different risk factors interact within a portfolio. By diversifying exposure across multiple factors, such as size, value, momentum, and profitability, investors can achieve a more balanced risk-return profile.

This diversification helps minimize the impact of any single factor on portfolio performance, improving overall risk management and reducing vulnerability to market downturns.

3. Performance Attribution and Benchmarking Against Factor Models

Multifactor models are used to attribute portfolio performance to specific factors, distinguishing between returns generated by systematic factors and those driven by active management decisions. This enables investors to evaluate whether performance results from factor exposure or the manager's skill in security selection.

Benchmarking a portfolio against a multifactor model helps determine if the manager is providing value beyond what can be explained by broad market factors.

4. Tactical Asset Allocation and Market Timing

Multifactor models can guide tactical asset allocation decisions by highlighting changing factor dynamics. For example, if momentum factors are expected to outperform, an investor can adjust portfolio exposure accordingly.

This approach allows investors to position their portfolios based on anticipated market movements, economic changes, or shifts in investor sentiment.

5. Use of Leveraged and Inverse ETFs for Short-Term Hedging

Multifactor insights can inform the use of specific financial instruments, such as leveraged and inverse ETFs, to hedge against market risk or to gain amplified exposure to a factor temporarily. This can be particularly useful for tactical risk management during periods of market volatility.

6. Risk-Adjusted Return Optimization

By understanding the risk exposures of different factors, multifactor models help optimize portfolio risk-adjusted returns. For example, an investor may identify that adding exposure to small-cap stocks increases returns without proportionally increasing risk, improving the Sharpe ratio of the portfolio.

7. Integration into Quantitative and Fundamental Strategies

Multifactor models are used in quantitative strategies to build portfolios that systematically allocate based on factor exposures. In fundamental strategies, investors may assess a company's risk and expected return by examining its sensitivity to various factors, such as industry trends or macroeconomic changes.

This integration allows for a data-driven approach to security selection and risk management, complementing traditional analysis.

8. Stress Testing and Scenario Analysis

Multifactor models can be used to perform stress testing and scenario analysis, simulating how a portfolio might perform under different market conditions or changes in factor behavior. This helps investors prepare for adverse market movements and evaluate the robustness of their portfolios.

Examples

Example 1: Fama-French Three-Factor Model for Portfolio Construction

An investor seeks to outperform the market by building a portfolio with a tilt toward small-cap and value stocks, based on the Fama-French Three-Factor Model. By incorporating size and value factors, the investor aims to capture the historical premiums associated with these factors, enhancing long-term risk-adjusted returns.

Example 2: Arbitrage Pricing Theory (APT) for Macro Risk Management

A portfolio manager uses the Arbitrage Pricing Theory (APT) to model the impact of macroeconomic variables such as interest rates, inflation, and GDP growth on a bond portfolio. By analyzing these factors, the manager adjusts bond holdings to mitigate risks associated with economic shifts, reducing portfolio volatility.

Example 3: Momentum Factor for Active Trading Strategy

A hedge fund manager incorporates the momentum factor from the Carhart Four-Factor Model to identify stocks with strong past performance over recent months. By systematically investing in these stocks, the manager aims to capture short-term gains based on the trend-following behavior observed in the market.

Example 4: Custom Multifactor Model for ESG Investing

An investment firm develops a custom multifactor model that includes environmental, social, and governance (ESG) factors along with traditional market and value factors. This model helps the firm identify companies with strong ESG performance while achieving competitive risk-adjusted returns, aligning investments with the firm’s sustainability goals.

Example 5: Risk Mitigation through Factor Exposure Analysis

A diversified fund uses multifactor models to assess its exposure to various risk factors, such as market, size, and value. Upon discovering an overexposure to market risk, the fund adjusts its holdings by increasing allocations to defensive sectors, reducing overall market sensitivity while maintaining performance potential.

Practice Questions

Question 1:

Which of the following is a primary advantage of using multifactor models compared to single-factor models?

A) Simplifies the analysis by focusing solely on market risk.

B) Identifies multiple sources of systematic risk that impact returns.

C) Assumes that only one risk factor is relevant.

D) Limits portfolio diversification by concentrating on a single factor.

Answer: B) Identifies multiple sources of systematic risk that impact returns.

Explanation:

Multifactor models offer a significant advantage over single-factor models like CAPM by considering various systematic risk factors, such as size, value, and momentum, that can influence asset returns. This approach provides a more comprehensive view of risk and return dynamics. Option A and C are incorrect because they reflect single-factor limitations, while Option D is incorrect since multifactor models enhance diversification.

Question 2:

The Fama-French Three-Factor Model expands on the Capital Asset Pricing Model (CAPM) by adding which additional factors?

A) Momentum and market risk.

B) Value and size.

C) Growth and profitability.

D) Inflation and interest rates.

Answer: B) Value and size.

Explanation:

The Fama-French Three-Factor Model extends CAPM by incorporating value (book-to-market ratio) and size (small-cap vs. large-cap) factors, providing a more detailed explanation of stock returns beyond just market risk. Option A is incorrect as momentum is introduced in the Carhart Four-Factor Model. Options C and D are unrelated to the factors in the Three-Factor Model.

Question 3:

Which of the following multifactor models focuses on macroeconomic variables such as inflation and GDP growth to explain asset returns?

A) Capital Asset Pricing Model (CAPM)

B) Carhart Four-Factor Model

C) Arbitrage Pricing Theory (APT)

D) Fama-French Five-Factor Model

Answer: C) Arbitrage Pricing Theory (APT)

Explanation:

Arbitrage Pricing Theory (APT) incorporates multiple macroeconomic factors, such as inflation, GDP growth, and interest rates, to explain asset returns. Unlike CAPM, APT allows for a flexible number of factors based on market conditions. Options A, B, and D do not specifically focus on macroeconomic variables.