1.1 Foundations of Internal Auditing

On the Foundations of Internal Auditing are essential to understanding the role of internal auditing within organizations. You’ll explore the fundamental principles, including independence, objectivity, and professional standards. This area covers the core concepts of internal audit processes, risk management, and governance structures. Grasping these foundational principles is crucial for mastering the Internal Audit Basics section of the exam, as these concepts underpin the effectiveness and integrity of the internal audit function in supporting organizational goals and ensuring compliance.

Learning Objectives

In studying “1.1 Foundations of Internal Auditing” for the CIA exam, you should learn to understand the core principles and purposes of internal auditing, focusing on adding value and improving an organization’s operations. Familiarize yourself with the International Professional Practices Framework (IPPF) and its components, including the Code of Ethics and the Standards. Analyze the roles and responsibilities of internal auditors in promoting organizational governance, risk management, and control processes. Evaluate the importance of independence and objectivity, as well as how internal audit activities align with the organization’s objectives and support accountability. Additionally, understand the value of assurance and consulting services provided by internal auditors to enhance efficiency and effectiveness in achieving business goals.

Understanding the Core Principles and Purpose of Internal Auditing

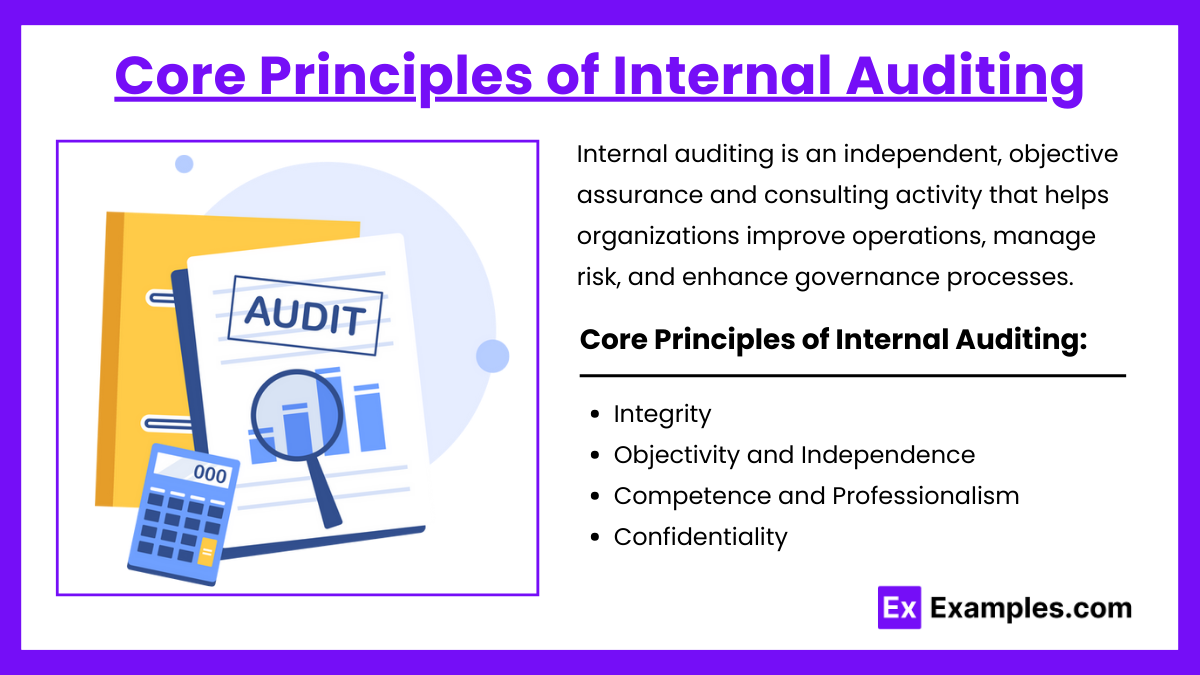

Internal auditing is an independent, objective assurance and consulting activity that helps organizations improve operations, manage risk, and enhance governance processes. The primary purpose of internal auditing is to add value by providing insights that support the organization in achieving its goals effectively, efficiently, and ethically. Let’s explore the core principles and purpose of internal auditing:

Core Principles of Internal Auditing

The core principles of internal auditing outline the essential qualities and actions that define a strong and effective internal audit function. These principles, as endorsed by the Institute of Internal Auditors (IIA), form the foundation of successful internal audit practices:

1. Integrity

Integrity is central to the role of internal auditors, requiring honesty, ethical behavior, and a commitment to transparency in all actions.

- Principle: Internal auditors must conduct their work with integrity, which fosters trust and confidence in the audit function.

- Application: Auditors report findings truthfully and avoid conflicts of interest to maintain credibility.

Example: An auditor identifies an instance of financial misstatement and reports it honestly to management, regardless of the potential impact on the organization’s reputation.

2. Objectivity and Independence

Objectivity means evaluating information fairly and without bias, while independence requires that internal auditors remain free from undue influence.

- Principle: Internal auditors should be independent of the processes they audit to maintain objectivity and provide unbiased recommendations.

- Application: Independence enables auditors to evaluate policies and procedures impartially, avoiding favoritism or external pressure.

Example: An internal auditor examining procurement processes avoids participating in the procurement function to ensure an unbiased review.

3. Competence and Professionalism

Internal auditors must possess the knowledge, skills, and experience required to perform audits effectively and provide accurate insights.

- Principle: Auditors should continuously improve their technical expertise and adhere to professional standards to enhance audit quality.

- Application: Staying updated with the latest industry practices ensures auditors can assess risks and controls accurately.

Example: A certified internal auditor attends training on cybersecurity to enhance the organization’s security assessment capabilities.

4. Confidentiality

Confidentiality is essential for maintaining trust, as auditors handle sensitive information about organizational processes and risks.

- Principle: Auditors must protect confidential information, using it only for audit purposes and disclosing it only when legally required.

- Application: Auditors should have processes in place to secure sensitive data and prevent unauthorized access.

Example: An auditor reviews sensitive payroll data but restricts access to authorized personnel only, protecting employee privacy.

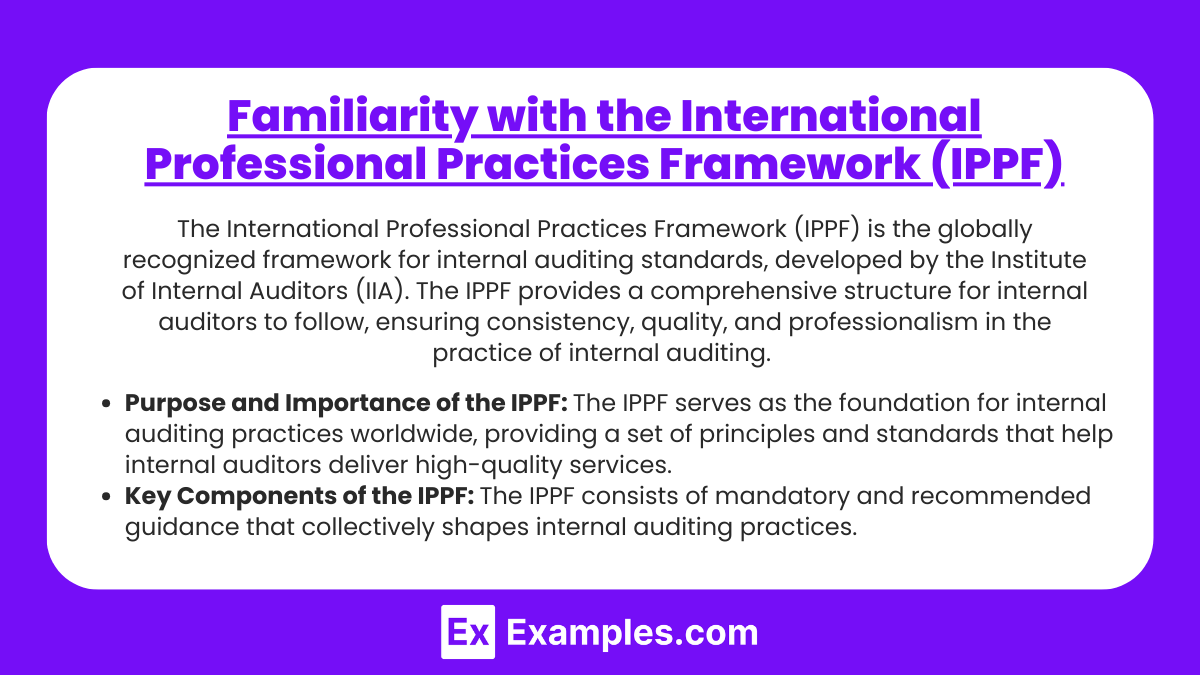

Familiarity with the International Professional Practices Framework (IPPF)

The International Professional Practices Framework (IPPF) is the globally recognized framework for internal auditing standards, developed by the Institute of Internal Auditors (IIA). The IPPF provides a comprehensive structure for internal auditors to follow, ensuring consistency, quality, and professionalism in the practice of internal auditing. It comprises principles, standards, and guidance that help internal auditors provide value to their organizations. Here’s an overview of the key components and purpose of the IPPF:

1. Purpose and Importance of the IPPF

The IPPF serves as the foundation for internal auditing practices worldwide, providing a set of principles and standards that help internal auditors deliver high-quality services.

- Consistency and Quality: By following the IPPF, internal auditors maintain consistent and high-quality practices across industries and geographic regions.

- Guidance and Professionalism: The IPPF upholds professional standards and ethical behavior, helping internal auditors meet the needs of stakeholders while adhering to best practices.

- Value Creation: The framework is designed to ensure that internal auditing adds value by improving governance, risk management, and control processes within organizations.

Example: An internal audit team uses IPPF standards as a guide to structure their audit approach, ensuring all audits are carried out with the same rigor and professionalism.

2. Key Components of the IPPF

The IPPF consists of mandatory and recommended guidance that collectively shapes internal auditing practices.

Mandatory Guidance

Mandatory guidance includes the core principles, the code of ethics, the standards, and the definition of internal auditing. It is essential for all internal auditors to adhere to this guidance, as it sets the foundational standards for the profession.

a. Core Principles for the Professional Practice of Internal Auditing

The core principles describe qualities that must be present for an effective internal audit function, such as integrity, objectivity, competence, and a commitment to adding value.

- Purpose: These principles outline the attributes internal auditors need to effectively support governance, risk management, and controls.

- Example: An internal auditor upholds integrity by avoiding conflicts of interest and ensuring objective reporting of findings.

b. Code of Ethics

The Code of Ethics establishes ethical standards for internal auditors, promoting integrity, confidentiality, objectivity, and competency.

- Purpose: It ensures that internal auditors adhere to the highest ethical standards, maintaining trust with stakeholders.

- Example: An internal auditor follows confidentiality guidelines by safeguarding sensitive financial information during an audit.

c. International Standards for the Professional Practice of Internal Auditing

The Standards are the foundation of the IPPF, providing guidance on audit performance and responsibilities. They include Attribute Standards (1000-1300) and Performance Standards (2000-2600).

- Purpose: The Standards provide a structured approach for conducting audits, setting expectations for planning, executing, and reporting.

- Example: Performance Standard 2000 requires internal auditors to develop an annual audit plan based on risk assessment, ensuring efficient resource allocation.

d. Definition of Internal Auditing

The definition describes internal auditing as an independent, objective assurance and consulting activity designed to add value and improve operations.

- Purpose: This definition guides internal auditors in understanding their role and the purpose of their work within the organization.

- Example: By identifying opportunities for process improvements, internal auditors contribute to operational efficiency, aligning with the IPPF definition.

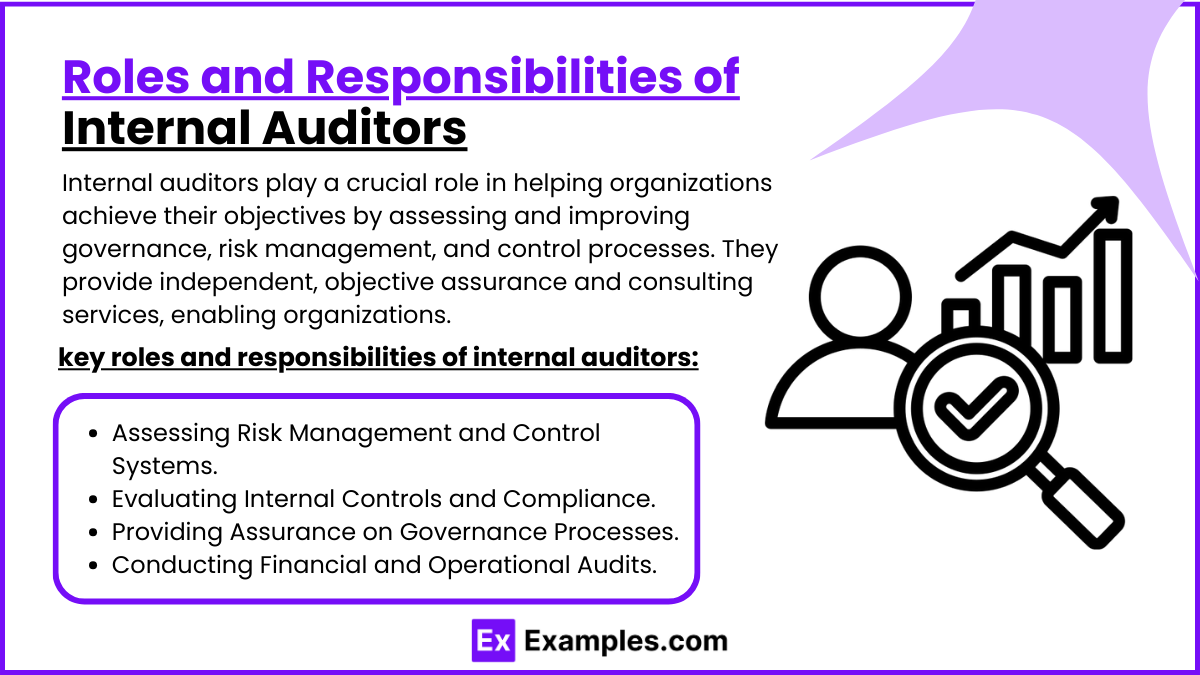

Roles and Responsibilities of Internal Auditors

Internal auditors play a crucial role in helping organizations achieve their objectives by assessing and improving governance, risk management, and control processes. They provide independent, objective assurance and consulting services, enabling organizations to operate efficiently, manage risks, and comply with regulations. Here’s an overview of the key roles and responsibilities of internal auditors:

1. Assessing Risk Management and Control Systems

Internal auditors evaluate the organization’s risk management processes to identify potential risks and determine whether adequate controls are in place to mitigate them.

- Responsibility: Review and test risk management practices, identifying gaps or weaknesses in risk controls.

- Purpose: To ensure that the organization can effectively identify, assess, and manage risks that may impact its objectives.

Example: An internal auditor conducts a risk assessment of the IT department, evaluating the effectiveness of cybersecurity controls to protect against data breaches.

2. Evaluating Internal Controls and Compliance

Internal auditors examine the effectiveness of internal controls to determine whether they are designed and implemented to achieve compliance with applicable laws, regulations, and internal policies.

- Responsibility: Test and validate that controls are working as intended to prevent errors, fraud, and regulatory violations.

- Purpose: To help the organization comply with regulatory requirements and reduce the risk of financial loss or reputational harm.

Example: An auditor tests controls around financial reporting to ensure compliance with the Sarbanes-Oxley Act and prevent material misstatements.

3. Providing Assurance on Governance Processes

Internal auditors provide assurance on the organization’s governance practices, ensuring that they align with ethical standards and support strategic objectives.

- Responsibility: Assess the effectiveness of governance structures, including board oversight, management accountability, and ethical practices.

- Purpose: To strengthen governance processes, promote accountability, and foster a culture of transparency.

Example: An internal audit team reviews the board’s oversight of executive compensation to ensure it aligns with the organization’s goals and ethical standards.

4. Conducting Financial and Operational Audits

Internal auditors examine financial and operational processes to assess their accuracy, efficiency, and alignment with organizational goals.

- Responsibility: Verify the accuracy of financial records, evaluate operational effectiveness, and identify opportunities for process improvement.

- Purpose: To support sound financial practices and optimize operational efficiency.

Example: An auditor reviews the procurement process to identify inefficiencies and recommend streamlined procedures that reduce costs.

Alignment of Internal Audit Activities with Organizational Objectives

Aligning internal audit activities with organizational objectives is essential to maximize the value internal audits bring to the organization. By focusing on areas that directly support strategic goals, internal auditors help organizations optimize resources, manage risks, and achieve key outcomes. Here’s how internal audit activities can align effectively with organizational objectives:

1. Understanding Organizational Goals and Strategies

To align with organizational objectives, internal auditors must first understand the organization’s vision, mission, and strategic goals.

- Approach: Internal auditors should review strategic plans, engage with senior management, and identify critical success factors.

- Outcome: This understanding enables auditors to prioritize audit activities that have a direct impact on achieving organizational goals.

Example: If an organization prioritizes expansion into new markets, the internal audit team may focus on risk assessments related to international operations, regulatory compliance, and supply chain management.

2. Conducting a Risk-Based Audit Planning Process

A risk-based audit approach aligns internal audit resources with areas of highest risk, ensuring that audit efforts focus on issues most likely to impact organizational objectives.

- Approach: Internal auditors conduct a risk assessment to identify high-risk areas aligned with strategic priorities, such as operational efficiency, compliance, and cybersecurity.

- Outcome: Audits are prioritized based on the potential impact on strategic goals, supporting effective resource allocation and risk mitigation.

Example: If cyber threats pose a high risk to a company’s strategic objective of protecting customer data, the internal audit team might prioritize cybersecurity audits and assess data protection controls.

3. Supporting Effective Governance and Accountability

Internal auditors assess the effectiveness of governance processes to ensure that oversight structures and decision-making mechanisms support the organization’s objectives.

- Approach: Auditors evaluate governance structures, board oversight, and management accountability practices.

- Outcome: Strong governance ensures that the organization remains on course to achieve its goals and upholds ethical standards.

Example: An internal audit of the board’s oversight on risk management practices ensures that governance aligns with organizational objectives and that strategic risks are properly monitored.

Examples

Example 1: Internal Control Frameworks

A fundamental aspect of internal auditing is the evaluation of internal control systems within an organization. For example, the COSO (Committee of Sponsoring Organizations of the Treadway Commission) framework is widely used by internal auditors to assess the effectiveness of an organization’s internal controls. By examining the control environment, risk assessment processes, control activities, information and communication systems, and monitoring activities, auditors can provide insights into areas that may require improvement or adjustment.

Example 2: Risk Assessment Processes

Internal auditors are tasked with identifying and assessing risks that could impede the achievement of an organization’s objectives. For instance, a manufacturing company may conduct a risk assessment to evaluate potential operational hazards, such as equipment failure or supply chain disruptions. The internal audit team can analyze these risks and prioritize them based on their potential impact, allowing the organization to allocate resources effectively to mitigate those risks.

Example 3: Governance Evaluations

Internal auditors play a crucial role in evaluating the governance structures of an organization. For example, they may assess the effectiveness of the board of directors in overseeing management and ensuring that the organization adheres to ethical standards. This evaluation can include examining governance policies, decision-making processes, and compliance with regulatory requirements, which helps ensure accountability and transparency within the organization.

Example 4: Compliance Audits

Another foundation of internal auditing involves conducting compliance audits to ensure that the organization adheres to applicable laws, regulations, and internal policies. For example, a healthcare organization may be audited to verify compliance with healthcare regulations and standards, such as HIPAA (Health Insurance Portability and Accountability Act). By assessing compliance, internal auditors help mitigate legal risks and protect the organization’s reputation.

Example 5: Performance Improvement Initiatives

Internal auditors are also involved in evaluating the efficiency and effectiveness of organizational processes. For instance, they may conduct audits of the procurement process to identify inefficiencies, such as excessive lead times or poor supplier performance. By analyzing these processes, internal auditors can provide recommendations for improvement, helping the organization optimize operations and achieve better performance outcomes. This role emphasizes the internal audit function’s value in contributing to overall organizational success.

Practice Questions

Question 1

What is the primary purpose of internal auditing within an organization?

A) To provide external stakeholders with financial statements.

B) To evaluate and improve the effectiveness of risk management, control, and governance processes.

C) To prepare tax returns and ensure compliance with tax laws.

D) To investigate employee misconduct and fraud.

Correct Answer: B) To evaluate and improve the effectiveness of risk management, control, and governance processes.

Explanation: The primary purpose of internal auditing is to provide independent assurance that an organization’s risk management, governance, and internal control processes are operating effectively. Internal auditors assess how well the organization is managing risks and whether the controls in place are sufficient to mitigate those risks. While options A and C relate to external auditing and tax compliance, respectively, they do not represent the core function of internal auditing. Option D, while relevant to internal auditing, is just one aspect of a broader role.

Question 2

Which of the following is a key attribute of effective internal auditors?

A) They should focus solely on compliance with regulations.

B) They must possess strong analytical and critical thinking skills.

C) They should prioritize their independence from the organization.

D) They need to have expertise only in financial accounting.

Correct Answer: B) They must possess strong analytical and critical thinking skills.

Explanation: Effective internal auditors need to have strong analytical and critical thinking skills to evaluate complex processes, identify risks, and suggest improvements. While independence is also crucial for maintaining objectivity in their evaluations, option B directly addresses the skills necessary to perform their roles effectively. Options A and D limit the role of internal auditors to compliance and financial expertise, which do not encompass the full range of skills needed for comprehensive internal auditing.

Question 3

In the context of internal auditing, what is the significance of the International Professional Practices Framework (IPPF)?

A) It provides a set of legal guidelines for auditing practices.

B) It serves as a framework for developing accounting standards.

C) It establishes a globally recognized set of standards and guidelines for internal auditing.

D) It is a certification program for internal auditors.

Correct Answer: C) It establishes a globally recognized set of standards and guidelines for internal auditing.

Explanation: The International Professional Practices Framework (IPPF) is significant because it provides a comprehensive set of standards and guidelines that govern the internal auditing profession globally. The IPPF helps ensure consistency and quality in internal auditing practices across different organizations and countries. It does not serve as legal guidelines or accounting standards, nor is it a certification program, making option C the correct choice.