Performing the Engagement

Preparing for the CIA Exam requires a thorough grasp of "Performing the Engagement," a critical aspect of auditing practice. This area emphasizes an auditor’s ability to execute audit engagements systematically, apply professional judgment, and maintain independence and objectivity. Mastering these skills ensures auditors can thoroughly assess controls, identify risks, and provide valuable insights for organizational improvement, which is essential for success on the CIA Exam.

Learning Objectives

In studying "Performing the Engagement" for the CIA exam, you should learn to understand the phases of the audit engagement process, including planning, executing, and reporting. Focus on defining objectives, scope, and approach through risk assessments and resource allocation. Understand techniques for evidence collection, such as interviewing, observation, and sampling, to substantiate findings effectively. Analyze internal controls, identify potential weaknesses, and assess their impact on organizational objectives. Evaluate communication strategies for reporting findings, ensuring clarity and relevance to stakeholders. Additionally, emphasize the importance of providing actionable recommendations that enhance governance, risk management, and control processes within the organization.

Core Elements of "Performing the Engagement"

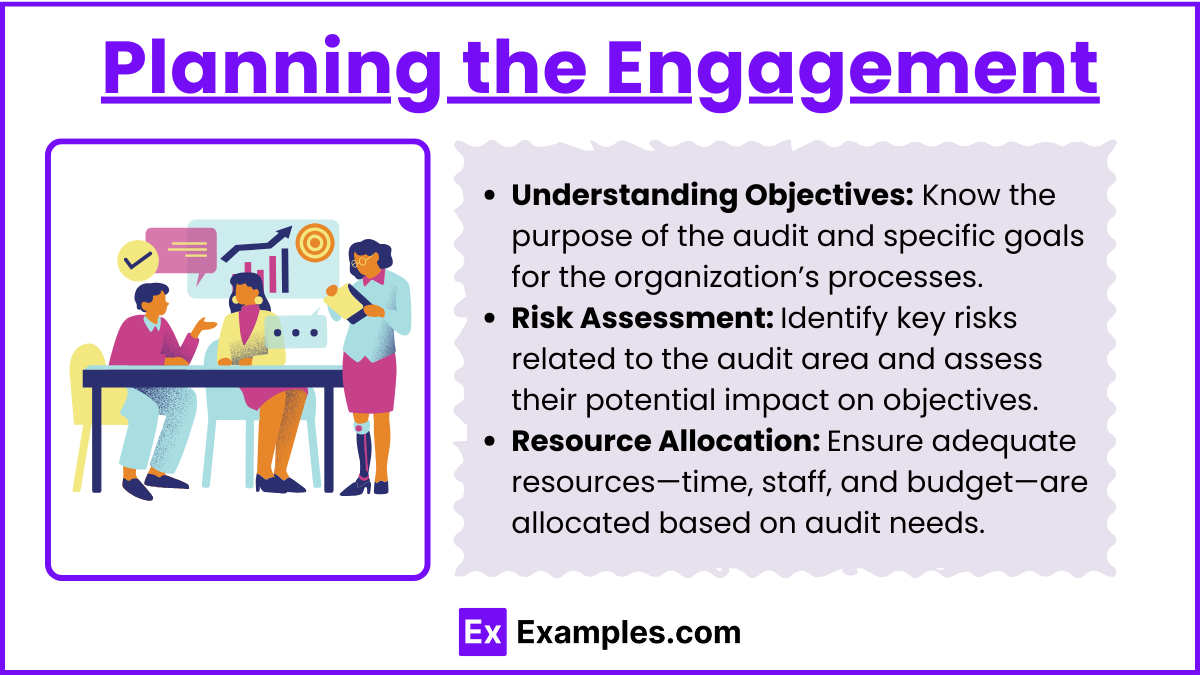

1. Planning the Engagement

Understanding Objectives: Know the purpose of the audit and specific goals for the organization’s processes.

Risk Assessment: Identify key risks related to the audit area and assess their potential impact on objectives.

Resource Allocation: Ensure adequate resources—time, staff, and budget—are allocated based on audit needs.

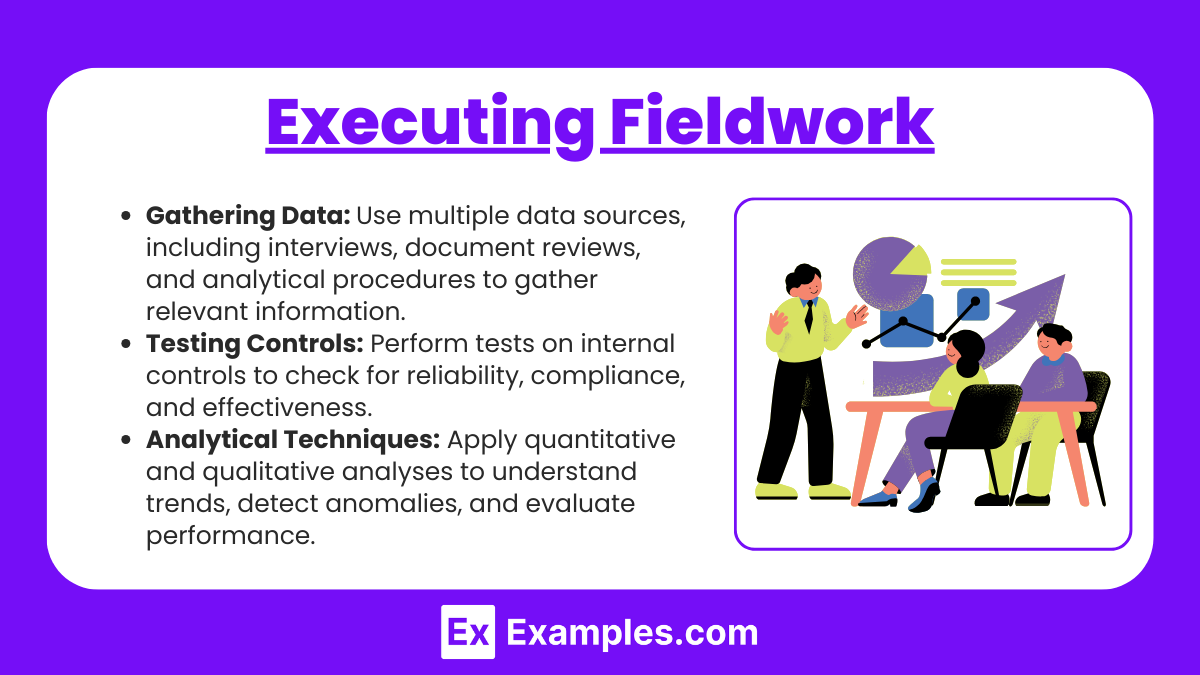

2. Executing Fieldwork

Gathering Data: Use multiple data sources, including interviews, document reviews, and analytical procedures to gather relevant information.

Testing Controls: Perform tests on internal controls to check for reliability, compliance, and effectiveness.

Analytical Techniques: Apply quantitative and qualitative analyses to understand trends, detect anomalies, and evaluate performance.

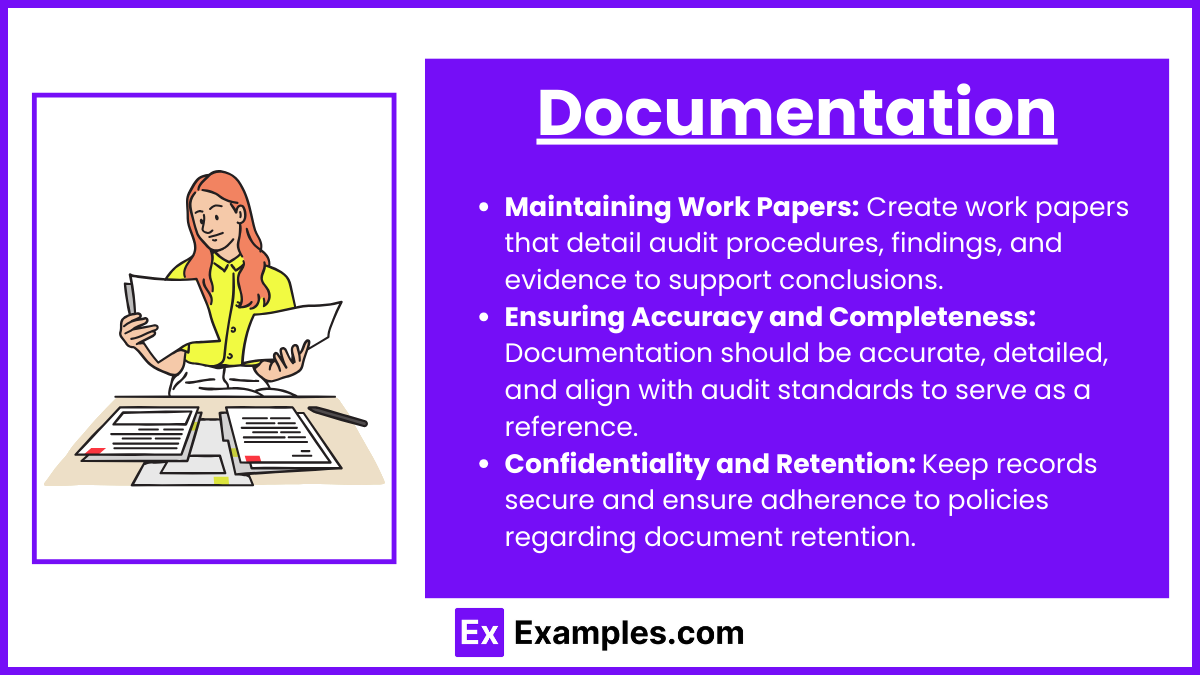

3. Documentation

Maintaining Work Papers: Create work papers that detail audit procedures, findings, and evidence to support conclusions.

Ensuring Accuracy and Completeness: Documentation should be accurate, detailed, and align with audit standards to serve as a reference.

Confidentiality and Retention: Keep records secure and ensure adherence to policies regarding document retention.

4. Communicating Findings

Drafting the Report: Prepare a report summarizing findings, recommendations, and action items for the organization.

Clear and Concise Language: Avoid jargon, make findings easily understandable, and highlight areas needing management’s attention.

Follow-Up Plans: Propose plans for periodic follow-ups to verify the implementation of recommended changes.

5. Quality Assurance and Improvement Program (QAIP)

Ongoing Improvement: Implement quality assurance practices to evaluate the audit’s effectiveness and identify areas for improvement.

Compliance with Standards: Ensure that the engagement complies with the International Standards for the Professional Practice of Internal Auditing.

Professional Development: Engage in continuous learning and skill enhancement to keep up-to-date with evolving audit practices.

Key Learning Objectives

1. Mastering Core Processes of Audit Execution

Understand the primary steps and methodologies involved in conducting an audit.

Focus on maintaining consistency in following established audit procedures.

Ensure adherence to the audit plan, addressing deviations effectively when they arise.

2. Implementing Audit Procedures with Precision

Learn the importance of executing audit tasks accurately to gather credible evidence.

Develop techniques to evaluate the reliability of data sources and information.

Practice assessing different audit techniques for their effectiveness in various audit scenarios.

3. Gathering Sufficient and Reliable Evidence

Recognize the characteristics of sufficient and appropriate evidence in an audit context.

Understand the types of evidence (documentary, testimonial, analytical) and how to obtain them.

Implement practices for validating information and ensuring its accuracy.

Importance of "Performing the Engagement"

Understanding the importance of "Performing the Engagement" is essential for CIA candidates, as it represents a core competency in the field of internal auditing. This section focuses on the actual execution phase of the audit, where auditors put their plans into action to gather evidence, assess risks, and ultimately provide objective insights to stakeholders. Here are some key reasons why "Performing the Engagement" is crucial:

1. Ensuring Reliable and Accurate Audit Results

The execution phase is where the audit truly takes shape. The methods and procedures used directly impact the reliability and accuracy of the audit's outcomes.

By following a structured approach, auditors can ensure that the evidence gathered is credible and supports valid conclusions, which is essential for building trust in the audit process.

2. Maintaining Objectivity and Ethical Standards

Objectivity is at the heart of the internal audit profession. During the engagement, auditors are responsible for maintaining an unbiased stance, ensuring that findings are based on evidence rather than personal or organizational biases.

Ethical standards are also upheld during this phase, as auditors follow frameworks that prioritize transparency, honesty, and integrity in all interactions and decisions.

3. Managing Resources Efficiently

Performing the engagement requires careful planning and resource allocation. Efficient resource management ensures that the audit is completed within budget and on time, which is critical in real-world settings.

Effective use of resources also allows auditors to maximize coverage and minimize disruptions, making the audit process smoother for both the auditing team and the organization.

4. Addressing Risks and Providing Assurance

One of the primary objectives of an internal audit is to identify and assess risks that could impact the organization. During the engagement phase, auditors can detect control weaknesses, operational inefficiencies, and compliance issues.

By addressing these risks proactively, auditors provide valuable assurance to stakeholders, helping the organization mitigate potential threats and improve resilience.

5. Enhancing Decision-Making through Evidence-Based Conclusions

The findings and conclusions drawn during the engagement phase form the foundation for decision-making. Clear, evidence-based conclusions allow stakeholders to take informed actions based on the audit's insights.

This can lead to improvements in internal controls, enhanced operational efficiency, and overall better alignment with the organization’s strategic goals.

Examples

Example 1. Assessing Internal Controls

During the engagement, auditors evaluate the effectiveness of internal controls within the organization. This step involves understanding control processes, testing them for reliability, and identifying areas where improvements can be made. Effective control assessment ensures that risks are managed, and operations align with the organization’s objectives.

Example 2 . Documenting Evidence

A crucial part of engagement is gathering and documenting audit evidence. Auditors meticulously collect data, verify records, and retain documentation that supports their findings. Detailed documentation not only substantiates conclusions but also serves as a reference for future engagements and reviews by supervisory bodies.

Example 3 . Communicating Findings

The engagement process includes communicating the findings to the organization's management. Auditors prepare detailed reports highlighting any discrepancies, compliance issues, or risk exposures discovered during the review. Clear communication helps management understand the findings and fosters proactive measures for risk mitigation.

Example 4 . Performing Risk Assessments

Risk assessment forms the basis of any engagement. Auditors analyze potential risks, evaluate their impact, and determine the likelihood of occurrence. By performing risk assessments, auditors can tailor the engagement to focus on areas that pose the greatest risk to the organization, ensuring a more efficient and focused approach.

Example 5 . Providing Recommendations

Engagements often culminate in providing actionable recommendations. Based on observations and findings, auditors suggest improvements or corrective actions to enhance operational efficiency and strengthen internal controls. Well-constructed recommendations guide management toward implementing changes that align with best practices and regulatory standards.

Practice Questions

Question 1

Which of the following best describes the purpose of engagement fieldwork in an internal audit?

A) To develop the annual audit plan

B) To establish and maintain independence and objectivity

C) To collect sufficient, relevant, and reliable information to support audit findings and recommendations

D) To review the entire organizational risk management process

Answer: C) To collect sufficient, relevant, and reliable information to support audit findings and recommendations

Explanation:

During the fieldwork phase of an engagement, auditors gather information to substantiate their conclusions and recommendations. This information must be sufficient, relevant, and reliable to ensure that findings are valid and can be used to make improvements. Developing the audit plan (A) and maintaining independence (B) are broader aspects of audit planning and professional conduct, not specific to fieldwork. Reviewing the risk management process (D) may be a part of the engagement if it aligns with the audit objectives, but it does not represent the primary purpose of fieldwork.

Question 2

What is the primary purpose of preparing and reviewing working papers during an engagement?

A) To ensure that the engagement is completed on schedule

B) To document evidence collected and support the audit findings and recommendations

C) To communicate audit findings directly to the management

D) To evaluate the effectiveness of the organization’s control environment

Answer: B) To document evidence collected and support the audit findings and recommendations

Explanation:

Working papers serve as a comprehensive record of the information collected, analyses conducted, and conclusions reached during an engagement. They help ensure that the evidence supports the audit's findings and recommendations, providing a basis for any conclusions made. Although timeliness (A) is important, it is not the primary reason for preparing working papers. Communicating findings (C) happens at the reporting stage, not in the working paper documentation. Evaluating the control environment (D) may occur in an audit but is not the primary purpose of working papers, which focus on recording and justifying the audit’s work.

Question 3

During an internal audit engagement, an auditor discovers a potential compliance violation. What is the auditor's most appropriate initial action?

A) Document the violation in the audit report without further action

B) Ignore the finding to avoid potential conflicts with management

C) Notify the appropriate management or compliance personnel while continuing the engagement

D) Conduct a full investigation independently before informing anyone

Answer: C) Notify the appropriate management or compliance personnel while continuing the engagement

Explanation:

An auditor should communicate potential violations promptly to the appropriate level of management or compliance staff to address the issue while continuing with the audit. This allows the organization to take timely action. Documenting the violation without notification (A) does not help in resolving the issue. Ignoring the finding (B) violates the auditor's responsibility to provide objective findings. Conducting an independent investigation (D) beyond the audit’s scope is typically unnecessary and may go beyond the auditor’s role, as further steps are usually coordinated with the compliance or legal teams.