Cost Management

Preparing for the CMA Exam requires a profound understanding of Cost Management principles, vital for mastering cost control and efficiency strategies. Grasping cost behavior, allocation techniques, and budgeting processes empowers you to make data-driven decisions that enhance profitability. With expertise in methods like Activity-Based Costing (ABC), variance analysis, and strategic budgeting, you gain crucial insights for reducing waste and optimizing resources. This knowledge is essential not only for excelling on the CMA exam but also for driving sustainable financial performance in real-world scenarios.

Learning Objective

In studying "Cost Management" for the CMA Exam, you should develop an understanding of the principles and techniques used in planning, controlling, and analyzing costs to enhance organizational efficiency. Explore the classifications of costs, cost behavior, and allocation methods such as Activity-Based Costing (ABC) and traditional costing. Understand the roles of budgeting, variance analysis, and performance metrics in optimizing resource use and improving profitability. Evaluate how these cost management tools enable informed decision-making, support financial control, and drive strategic cost savings. Apply this knowledge to analyze cost structures, assess cost drivers, and solve CMA practice questions on cost management challenges and efficiency improvements.

1. Introduction to Cost Management

Definition: Cost Management refers to the process of planning, controlling, and analyzing costs to ensure effective use of resources, leading to improved profitability and cost-efficiency.

Objective: Supports decision-making to enhance cost efficiency and maximize profitability while maintaining quality.

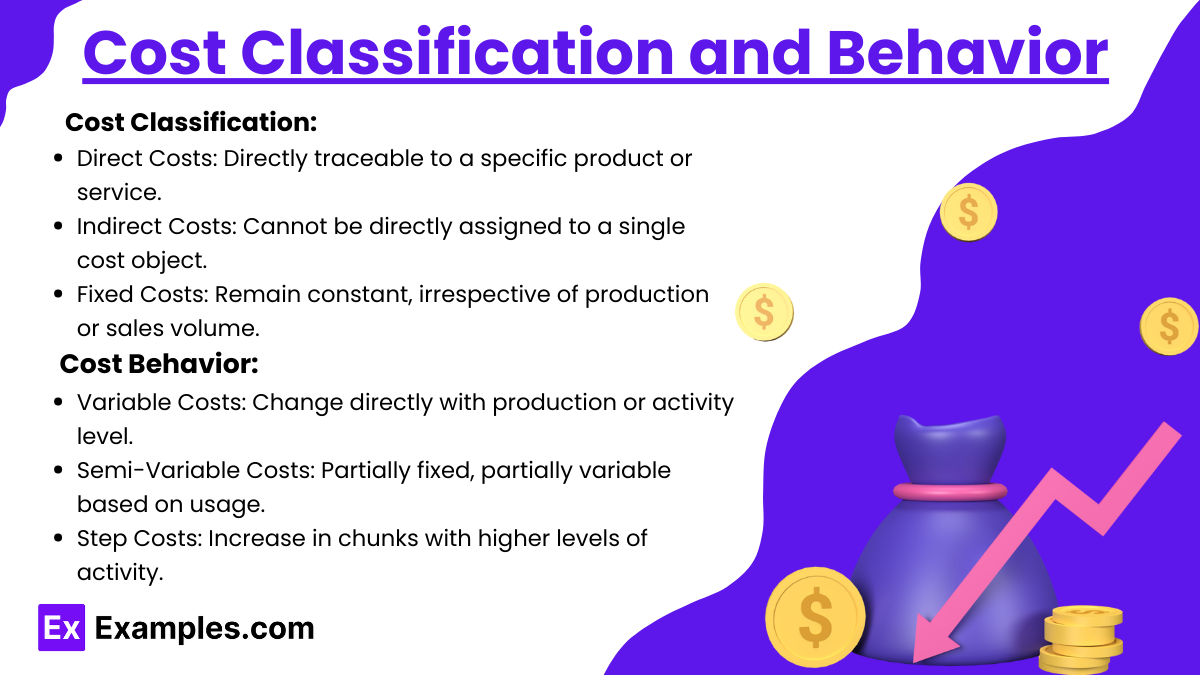

2. Cost Classification and Behavior

Types of Costs:

Fixed Costs: Remain constant irrespective of activity level (e.g., rent, salaries).

Variable Costs: Vary directly with production volume (e.g., raw materials).

Semi-Variable Costs: Partly fixed and partly variable, changing with production but not in direct proportion.

Behavioral Analysis:

Direct Costs: Attributable to a specific cost object (e.g., direct labor, materials).

Indirect Costs: Cannot be directly attributed to a single cost object (e.g., overheads).

Cost Drivers: Factors affecting the level of costs, such as labor hours or machine hours.

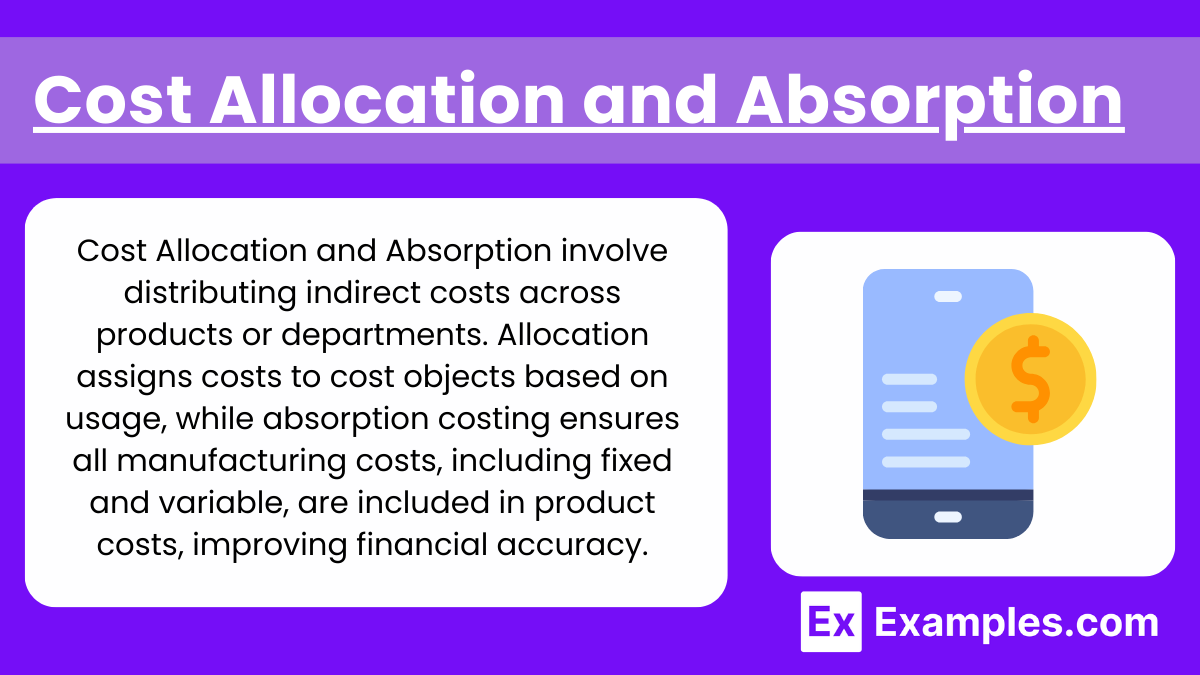

3. Cost Allocation and Absorption

Purpose: Assigns indirect costs to different products, services, or departments for more accurate cost tracking.

Methods:

Traditional Costing: Allocates overhead based on a single measure, such as labor hours, though it may lack accuracy in complex processes.

Activity-Based Costing (ABC): Allocates costs based on activities that drive costs, providing a more precise cost picture, especially for businesses with varied products.

Absorption Costing: Ensures that all manufacturing costs (both variable and fixed) are included in product costs, aligning with generally accepted accounting principles (GAAP).

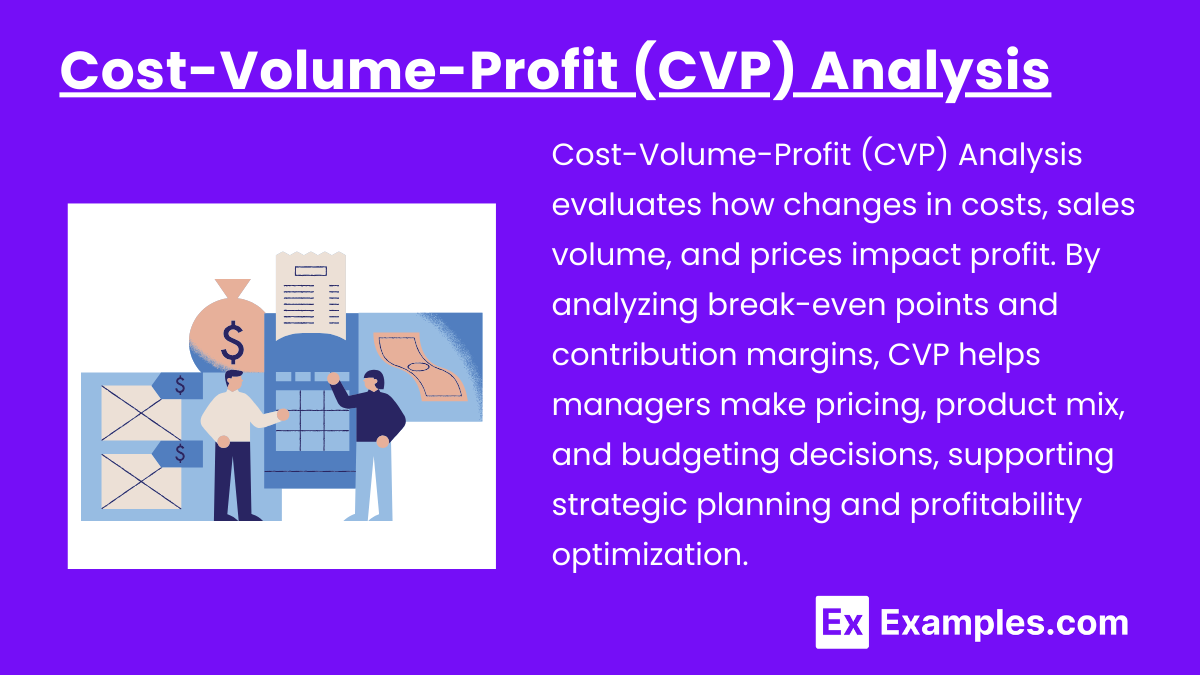

4. Cost-Volume-Profit (CVP) Analysis

Purpose: Assesses how cost and volume affect profit to inform pricing, product mix, and budgeting.

Key Components:

Break-Even Point: Level of sales where total revenue equals total costs, resulting in zero profit.

Contribution Margin: Sales revenue minus variable costs, providing insight into profitability per unit.

Margin of Safety: Difference between actual sales and break-even sales, indicating risk buffer.

Formulas:

Break-Even in Units = Fixed Costs ÷ Contribution Margin per Unit

Break-Even in Sales Dollars = Fixed Costs ÷ Contribution Margin Ratio

Examples

Example 1: Identifying Fixed and Variable Costs in Production

Cost Structure Analysis: Fixed costs (e.g., rent) remain constant regardless of production volume, while variable costs (e.g., raw materials) change with production levels.

Application: Understanding fixed and variable costs helps managers predict how changes in production affect total costs and profits, essential for budgeting and decision-making.

Example 2: Applying Activity-Based Costing (ABC) to Allocate Overhead

ABC Methodology: Costs are allocated based on activities that drive expenses, providing a more accurate view of product costs.

Benefit: ABC improves cost precision, especially in diverse product lines, enabling better pricing and resource allocation.

Example 3: Using Standard Costing for Budget Control

Setting Cost Standards: Predetermined costs (standards) are established for materials, labor, and overhead to compare against actual costs.

Variance Analysis: By identifying variances (differences between standard and actual costs), management can investigate inefficiencies and adjust processes.

Example 4: Implementing Lean Management to Reduce Waste

Lean Principles: Focus on minimizing non-value-added activities, such as excess inventory or unnecessary motion, to improve efficiency.

Outcome: Reducing waste leads to lower production costs, improved cash flow, and increased competitiveness.

Example 5: Using Break-Even Analysis for Pricing Decisions

Break-Even Point Calculation: Determines the sales level at which total revenue equals total costs, resulting in zero profit.

Application: Helps managers set prices or assess the viability of new products by understanding the volume needed to cover costs and achieve profitability.

Practice Questions

Question 1:

Which of the following techniques is most effective for identifying cost drivers and allocating overhead costs based on actual resource usage?

A) Job Order Costing

B) Standard Costing

C) Activity-Based Costing (ABC)

D) Absorption Costing

Answer: C) Activity-Based Costing (ABC)

Explanation: ABC allocates costs based on specific activities, providing detailed insights into how resources are consumed, making it effective for identifying cost drivers and improving cost allocation accuracy.

Question 2:

In a cost management context, what type of cost remains unchanged despite fluctuations in production levels?

A) Variable Cost

B) Fixed Cost

C) Direct Cost

D) Marginal Cost

Answer: B) Fixed Cost

Explanation: Fixed costs, such as rent or depreciation, do not vary with production levels, providing stability in budgeting but affecting overall cost per unit as production changes.

Question 3:

Which cost management technique focuses on continuous improvement by minimizing waste in production processes?

A) Standard Costing

B) Break-Even Analysis

C) Lean Management

D) Absorption Costing

Answer: C) Lean Management

Explanation: Lean Management emphasizes eliminating non-value-added activities, improving efficiency, and reducing costs by minimizing waste in all areas of production.