Performance Management

Preparing for the CMA Exam requires a deep understanding of Performance Management, crucial for excelling in organizational performance evaluation and improvement. Grasping the fundamentals of setting objectives, selecting Key Performance Indicators (KPIs), and applying benchmarking techniques equips you with the skills to assess and enhance business performance. Mastering performance evaluation tools like the Balanced Scorecard and techniques like variance analysis provides you with insights to drive operational efficiency and strategic alignment.

Learning Objective

In studying “Performance Management” for the CMA Exam, you should build a strong grasp of the principles guiding performance evaluation and enhancement. This includes understanding objective setting, selecting and measuring Key Performance Indicators (KPIs), and employing performance analysis tools like the Balanced Scorecard. Explore the importance of benchmarking, variance analysis, and responsibility accounting in creating accountability and driving continuous improvement. Evaluate how these tools and techniques help align individual and organizational goals, improve decision-making, and support operational efficiency. Additionally, recognize how effective performance management fosters a culture of accountability and strategic focus. Apply this knowledge to solving CMA practice questions on performance measurement, operational analysis, and organizational strategy alignment.

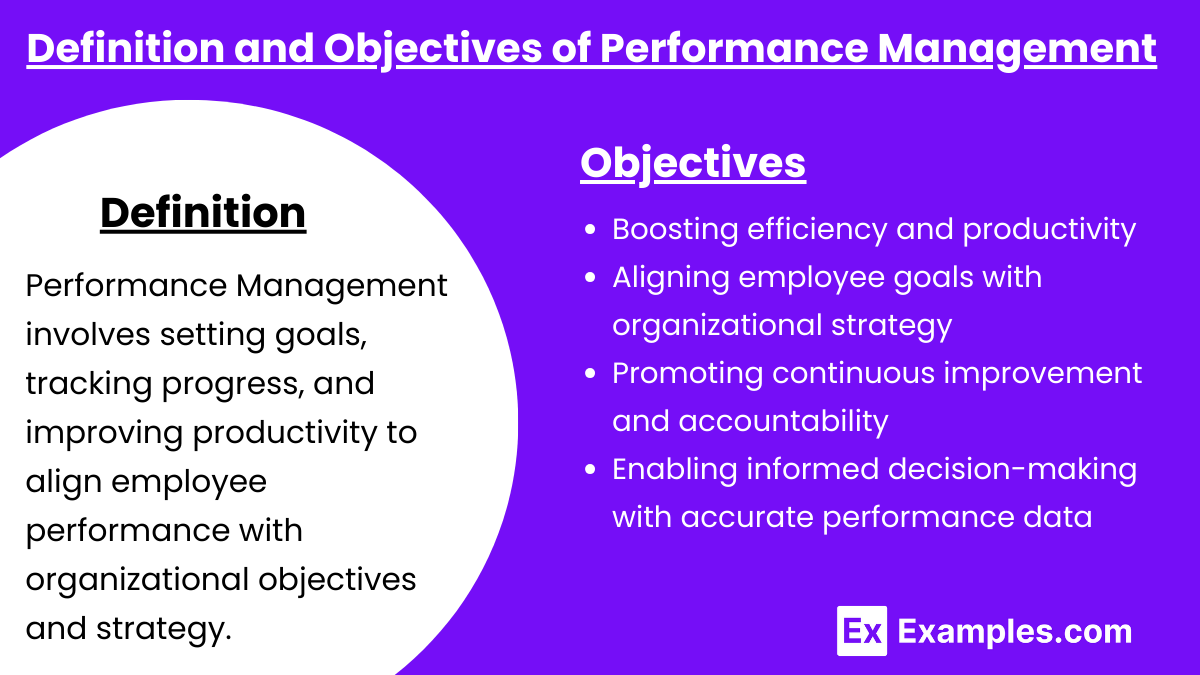

1. Definition and Objectives of Performance Management

Performance Management refers to the process of setting objectives, measuring results, and comparing actual outcomes with set targets to manage and improve organizational performance.

Objectives include:

- Enhancing efficiency and productivity

- Ensuring alignment of employee goals with organizational strategy

- Driving continuous improvement and fostering accountability

- Supporting better decision-making with accurate performance data

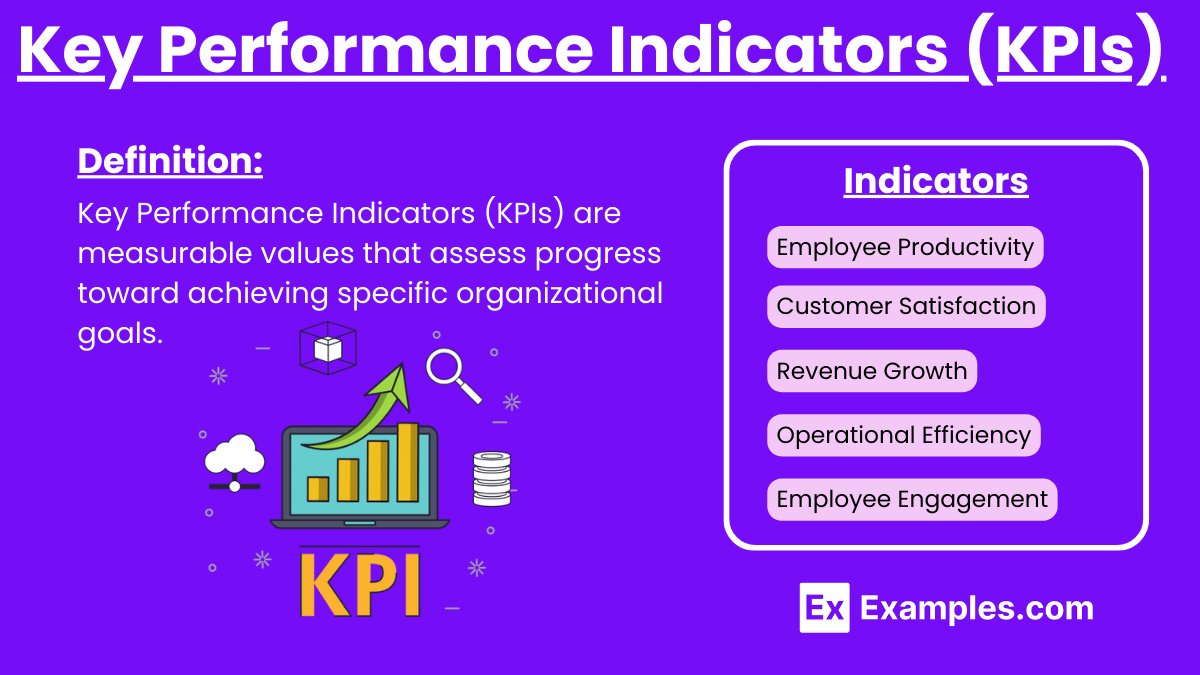

2. Key Performance Indicators (KPIs)

Definition: KPIs are measurable values that reflect the effectiveness of an organization in achieving key business objectives.

Types of KPIs:

- Financial KPIs (e.g., Revenue Growth Rate, Profit Margin)

- Customer KPIs (e.g., Customer Satisfaction, Retention Rate)

- Operational KPIs (e.g., Cycle Time, Process Efficiency)

- Employee KPIs (e.g., Employee Productivity, Turnover Rate)

Characteristics of Effective KPIs:

- Relevance to strategic objectives

- Measurability and clarity

- Attainability within resource constraints

3. Balanced Scorecard (BSC)

- Purpose: A strategic planning and management tool that balances four key perspectives to provide a comprehensive view of organizational performance.

- Perspectives:

- Financial: Measures profitability, cost management, and financial growth.

- Customer: Focuses on customer satisfaction, market share, and brand reputation.

- Internal Processes: Examines efficiency and quality in operational processes.

- Learning and Growth: Covers employee skills, innovation, and corporate culture.

- Implementation: Involves setting objectives, identifying KPIs, and linking them to strategic goals to monitor and improve performance.

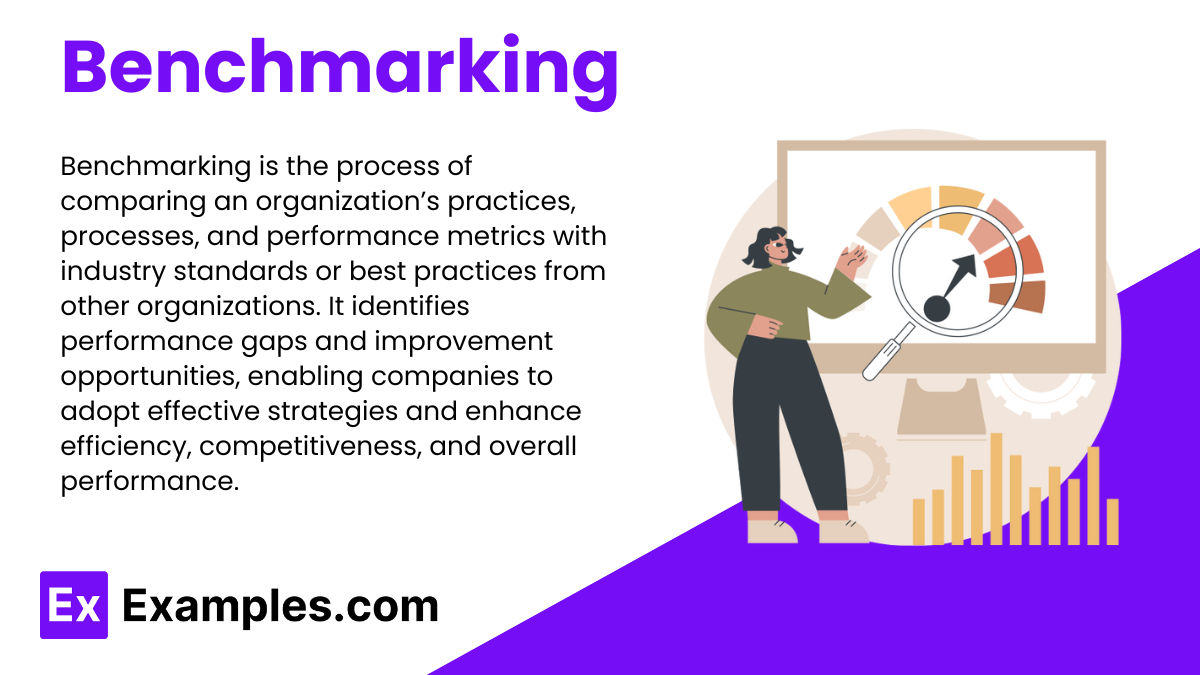

4. Benchmarking

- Definition: Comparing an organization’s processes and performance metrics to industry standards or best practices.

- Types of Benchmarking:

- Internal Benchmarking: Comparing similar processes within different departments.

- Competitive Benchmarking: Comparing with direct competitors.

- Functional Benchmarking: Comparing with businesses with similar processes.

- Generic Benchmarking: Focusing on processes unrelated to the industry.

- Steps in Benchmarking:

- Identify metrics and organizations for comparison

- Collect and analyze data

- Set improvement goals based on findings

- Implement and monitor improvements

Examples

Example 1: Setting Performance Objectives

- Objective Setting Process: Performance objectives are defined to align with organizational goals, guiding employees toward specific outcomes.

- SMART Goals: Performance objectives should be Specific, Measurable, Achievable, Relevant, and Time-bound to ensure clarity and focus.

Example 2: Role of Key Performance Indicators (KPIs)

- Defining KPIs: KPIs are selected to measure progress toward strategic goals, providing quantifiable metrics to track performance.

- Types of KPIs: Common categories include financial, customer satisfaction, operational efficiency, and employee engagement indicators.

Example 3: Application of the Balanced Scorecard (BSC)

- Using BSC for Performance Management: The Balanced Scorecard provides a comprehensive framework for assessing performance across financial, customer, internal process, and learning and growth perspectives.

- Implementing BSC: Objectives and KPIs are set for each perspective, aligning activities with organizational strategy and driving balanced growth.

Example 4: Conducting Benchmarking

- Benchmarking Process: Comparing internal processes and outcomes with industry standards or best practices to identify improvement areas.

- Types of Benchmarking: Includes internal, competitive, and functional benchmarking, allowing companies to learn from others and implement best practices.

Example 5: Analyzing Variances

- Variance Analysis: Comparing actual performance with budgeted or standard performance to identify variances, enabling proactive management.

- Types of Variances: Common areas include cost, revenue, and efficiency variances, each providing insights into specific performance aspects.

Practice Questions:

Question 1:

Which of the following best describes the purpose of Key Performance Indicators (KPIs) in performance management?

A) To document financial results in regulatory reports

B) To monitor progress toward achieving strategic goals

C) To establish employee reward systems

D) To simplify budgeting processes

Answer:

B) To monitor progress toward achieving strategic goals

Explanation:

KPIs are selected metrics that track an organization’s progress toward its goals, ensuring alignment with strategic objectives.

Question 2:

In the Balanced Scorecard framework, which perspective focuses on improving internal efficiency and effectiveness?

A) Financial

B) Customer

C) Internal Processes

D) Learning and Growth

Answer:

C) Internal Processes

Explanation:

The Internal Processes perspective in the Balanced Scorecard framework measures how efficiently and effectively internal operations meet organizational goals.

Question 3:

Which of the following techniques involves comparing an organization’s performance with industry best practices to identify improvement areas?

A) Variance Analysis

B) Responsibility Accounting

C) Benchmarking

D) Ratio Analysis

Answer:

C) Benchmarking

Explanation:

Benchmarking is the process of comparing a company’s performance and practices with industry leaders or best practices to identify areas for improvement.