Professional Ethics

In the Professional Ethics is foundational to maintaining integrity and trust in the management accounting profession. You’ll examine key ethical principles, including confidentiality, integrity, and objectivity. Understanding ethical standards and guidelines set by the IMA, as well as analyzing real-world ethical dilemmas, is crucial. These concepts are essential for mastering the ethical responsibilities that ensure accurate financial reporting, effective decision-making, and adherence to professional standards in various managerial accounting roles.

Learning Objectives

In studying "Professional Ethics" for the CMA, you should learn to recognize the principles of ethical behavior expected of management accountants, including integrity, objectivity, confidentiality, and professional competence. Understand how ethical standards apply to financial reporting, decision-making, and interactions with stakeholders. Analyze common ethical dilemmas and explore frameworks for resolving them while maintaining adherence to ethical guidelines. Evaluate the significance of ethical conduct in upholding public trust, fostering transparency, and enhancing organizational reputation. Additionally, familiarize yourself with the CMA’s Code of Ethics and how it guides accountants in maintaining high standards of professionalism and ethical responsibility.

Principles of Ethical Behavior for Management Accountants

Management accountants play a vital role in financial decision-making and reporting, influencing the integrity of financial information that supports business strategies. Ethical behavior is critical to maintaining trust, professionalism, and accountability in the field. Here are the key principles of ethical behavior for management accountants, which are typically guided by the Institute of Management Accountants (IMA) Statement of Ethical Professional Practice:

1. Honesty and Integrity

Management accountants must uphold honesty and integrity in all aspects of their professional responsibilities, avoiding actions that could harm the reputation of the organization or profession.

Truthfulness: Present financial information honestly, ensuring accuracy without omissions or misrepresentations.

Fair Dealing: Avoid conflicts of interest and ensure that personal interests do not influence business decisions.

Example: A management accountant should report errors or financial irregularities they discover, even if doing so may create discomfort or expose organizational issues.

2. Objectivity

Objectivity requires that management accountants maintain impartiality and fairness in their judgments, ensuring that their analysis and recommendations are free from bias.

Independent Judgment: Make decisions based solely on facts and evidence, not influenced by personal relationships or undue pressure.

Avoiding Conflicts of Interest: Refrain from engaging in activities or accepting gifts that could affect objectivity.

Example: An accountant assessing a capital investment should evaluate all potential risks and benefits without favoritism toward a particular department or executive.

3. Confidentiality

Management accountants have access to sensitive financial information and must protect its confidentiality unless legally required to disclose it.

Protecting Information: Safeguard all proprietary information and prevent unauthorized access.

Ethical Disclosure: Share sensitive information only with authorized parties, and avoid using confidential information for personal gain.

Example: An accountant working on a merger or acquisition should not share details with unauthorized colleagues or external parties, as doing so could lead to legal issues or compromise negotiations.

4. Professional Competence

Professional competence involves maintaining the knowledge and skills necessary to perform duties effectively and adhering to high standards of diligence.

Continuous Improvement: Stay updated with changes in accounting standards, regulations, and industry best practices.

Due Care: Perform tasks thoroughly and carefully, ensuring that all financial reports and analyses meet high-quality standards.

Example: An accountant should seek training on new regulatory requirements to ensure compliance and accuracy in financial reporting.

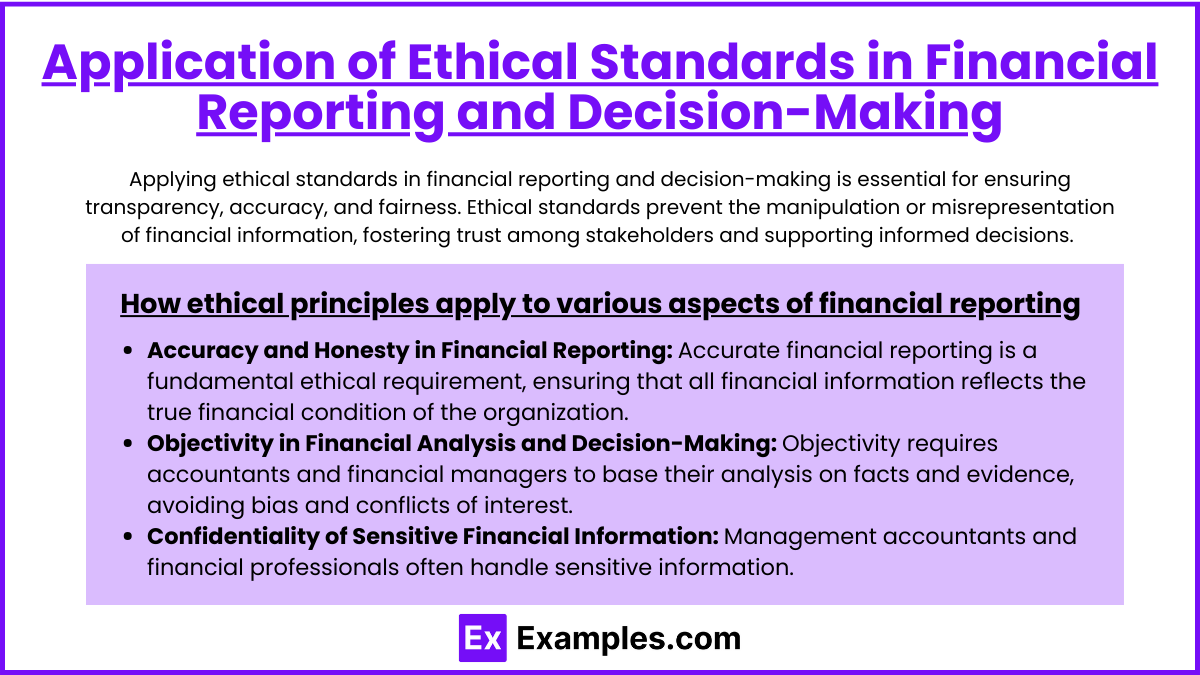

Application of Ethical Standards in Financial Reporting and Decision-Making

Applying ethical standards in financial reporting and decision-making is essential for ensuring transparency, accuracy, and fairness. Ethical standards prevent the manipulation or misrepresentation of financial information, fostering trust among stakeholders and supporting informed decisions. Here’s how ethical principles apply to various aspects of financial reporting and decision-making:

1. Accuracy and Honesty in Financial Reporting

Accurate financial reporting is a fundamental ethical requirement, ensuring that all financial information reflects the true financial condition of the organization.

Ethical Application: Accountants must record all transactions truthfully, without altering or omitting data to present a misleading picture. This includes avoiding overstatement or understatement of assets, liabilities, revenues, and expenses.

Example: An accountant who discovers an error in revenue reporting corrects it immediately, even if it reduces the perceived profitability for that period.

Impact: Honest reporting helps investors, creditors, and other stakeholders make informed decisions based on reliable data.

2. Objectivity in Financial Analysis and Decision-Making

Objectivity requires accountants and financial managers to base their analysis on facts and evidence, avoiding bias and conflicts of interest.

Ethical Application: Decisions should be made based on thorough analysis rather than personal interests or external pressures. Financial professionals should avoid situations where personal gains or relationships could influence their professional judgment.

Example: A financial manager evaluating investment options does so impartially, selecting the one that aligns best with organizational goals rather than favoring projects managed by close associates.

Impact: Objective analysis ensures fair and transparent decision-making, supporting the organization’s strategic goals without bias.

3. Confidentiality of Sensitive Financial Information

Management accountants and financial professionals often handle sensitive information, which must be kept confidential to maintain trust and comply with regulatory standards.

Ethical Application: Financial information should only be shared with authorized individuals and should not be disclosed for personal gain or to unauthorized parties.

Example: An accountant working on financial forecasts for a potential merger does not discuss these projections with family or friends to prevent potential insider trading issues.

Impact: Protecting confidentiality upholds trust within the organization and ensures compliance with legal standards, such as those related to insider trading and information security.

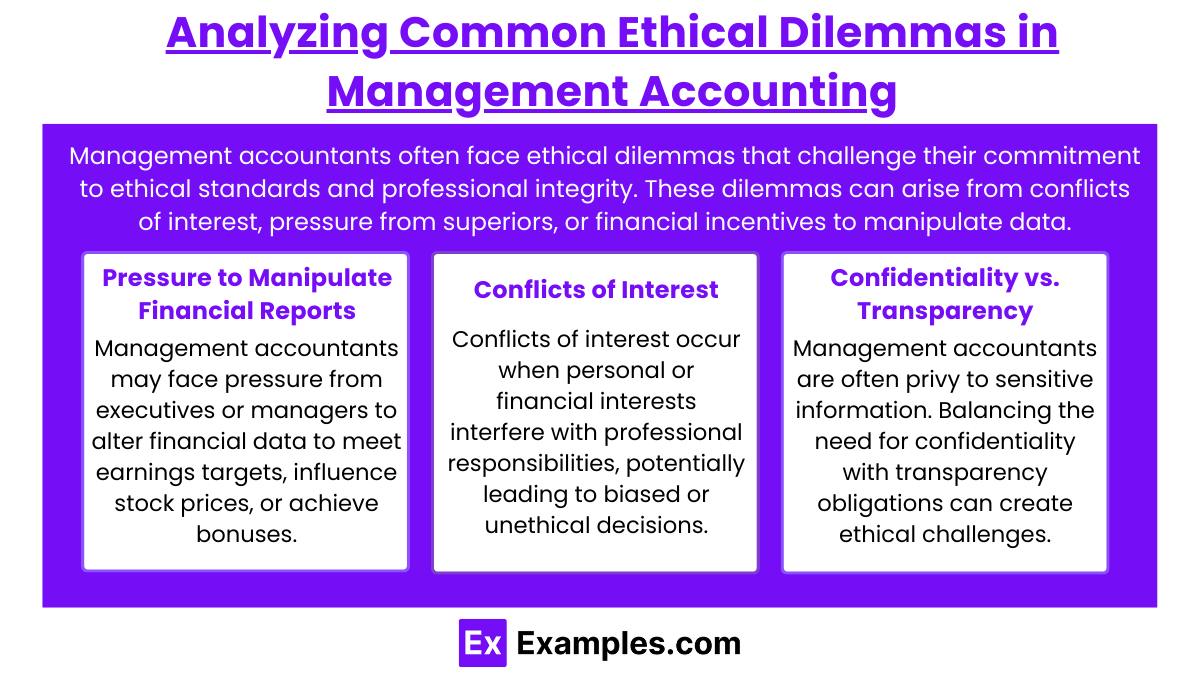

Analyzing Common Ethical Dilemmas in Management Accounting

Management accountants often face ethical dilemmas that challenge their commitment to ethical standards and professional integrity. These dilemmas can arise from conflicts of interest, pressure from superiors, or financial incentives to manipulate data. Understanding common ethical challenges helps accountants navigate complex situations with professionalism and uphold their ethical responsibilities.

1. Pressure to Manipulate Financial Reports

Management accountants may face pressure from executives or managers to alter financial data to meet earnings targets, influence stock prices, or achieve bonuses.

Dilemma: Should an accountant adjust figures to meet expectations, risking future financial stability and ethical integrity, or report honestly, possibly disappointing stakeholders?

Ethical Solution: The accountant should adhere to accuracy and integrity by presenting true financial results. Manipulating data misleads stakeholders and can have serious legal consequences.

Example: A manager pressures an accountant to defer expenses or accelerate revenue recognition to improve quarterly results. The accountant refuses, prioritizing honest reporting.

2. Conflicts of Interest

Conflicts of interest occur when personal or financial interests interfere with professional responsibilities, potentially leading to biased or unethical decisions.

Dilemma: Should an accountant participate in a decision where they have a personal stake, or should they disclose the conflict and recuse themselves?

Ethical Solution: Accountants should disclose any conflicts of interest and avoid participating in decisions where their impartiality may be compromised.

Example: An accountant with stock options in the company is asked to evaluate a project that could impact stock prices. The accountant discloses the conflict and steps back from the analysis to maintain objectivity.

3. Confidentiality vs. Transparency

Management accountants are often privy to sensitive information. Balancing the need for confidentiality with transparency obligations can create ethical challenges, especially when there is potential harm to stakeholders.

Dilemma: Should an accountant disclose confidential information to protect stakeholders from potential harm, or should they respect confidentiality and avoid unauthorized disclosures?

Ethical Solution: Accountants must respect confidentiality unless there is a clear legal or ethical obligation to disclose information for public safety or compliance purposes.

Example: An accountant discovers that the company is likely to experience a significant financial loss due to undisclosed liabilities. While respecting confidentiality, the accountant may need to advise management to make appropriate disclosures to stakeholders.

Significance of Ethical Conduct in Professional Accounting

Ethical conduct in professional accounting is vital to maintaining trust, integrity, and transparency in financial reporting and decision-making. Accountants are responsible for providing accurate, reliable financial information that supports informed decisions by management, investors, regulators, and other stakeholders. Here’s why ethical behavior is essential in the accounting profession:

1. Building and Maintaining Trust

Trust is the foundation of the accounting profession, and ethical conduct ensures that stakeholders have confidence in the financial information provided by accountants.

Importance of Trust: Investors, creditors, and regulatory bodies rely on accountants to present an honest and fair view of the organization’s financial health. Ethical behavior reinforces this trust, promoting credibility and professionalism.

Consequences of Lost Trust: When trust is compromised, it can lead to reputational damage, loss of business, and decreased market value.

Example: In cases like the Enron scandal, unethical behavior eroded public trust in financial reporting, leading to stringent regulations (like the Sarbanes-Oxley Act) to restore confidence in the profession.

2. Ensuring Transparency and Accuracy in Financial Reporting

Ethical conduct is essential for ensuring that financial statements are transparent, complete, and accurate. This honesty is crucial for stakeholders making economic decisions based on financial reports.

Clear Financial Insights: Transparent reporting allows investors and analysts to understand a company’s true financial position, supporting better investment decisions.

Preventing Misrepresentation: Ethical accountants avoid manipulations that could mislead stakeholders, helping to maintain the integrity of the market.

Example: A company that accurately reports all liabilities, even those that might negatively impact short-term results, demonstrates transparency, allowing investors to assess the real risks and rewards.

3. Upholding Regulatory Compliance and Legal Standards

Accountants must adhere to laws and regulations that govern financial reporting. Ethical behavior ensures that accountants remain compliant with these standards, reducing legal risks and penalties.

Regulatory Compliance: By following ethical guidelines, accountants help ensure compliance with regulatory frameworks such as GAAP, IFRS, and tax laws.

Legal Protection: Ethical conduct helps protect the organization from fines, lawsuits, and other penalties associated with non-compliance or fraudulent reporting.

Example: An ethical accountant would avoid practices like tax evasion, ensuring that tax filings are accurate and legally compliant, reducing potential penalties for the organization.

Examples

Example 1: Medical Ethics

In the healthcare field, medical professionals are guided by ethical principles such as beneficence, non-maleficence, autonomy, and justice. For instance, a physician must respect a patient's autonomy by obtaining informed consent before any treatment. This commitment to ethical practice ensures that patients are treated with dignity and that their rights and preferences are prioritized in medical decision-making.

Example 2: Legal Ethics

Lawyers adhere to a strict code of ethics, which includes the duty of confidentiality, loyalty to clients, and the obligation to represent clients zealously within the bounds of the law. For example, a lawyer must not disclose any information about a client’s case without their consent. This framework ensures that clients can trust their legal representatives and that the legal profession maintains its integrity and fairness.

Example 3: Business Ethics

In the corporate world, professionals are expected to uphold ethical standards that promote transparency, fairness, and accountability. For example, a company may have a code of ethics that prohibits insider trading and conflicts of interest, requiring employees to act honestly and with integrity in all business dealings. Adhering to these principles helps build a positive corporate culture and fosters trust with customers and stakeholders.

Example 4: Engineering Ethics

Engineers are responsible for ensuring public safety and welfare in their designs and projects. For instance, an engineer must disclose any potential hazards associated with a construction project and ensure compliance with safety regulations. Ethical guidelines in engineering emphasize the importance of protecting the environment and the community, requiring professionals to consider the broader implications of their work.

Example 5: Journalistic Ethics

Journalists are bound by ethical principles that promote accuracy, fairness, and independence in reporting. For example, a journalist must fact-check information before publishing a story and strive to present multiple perspectives on an issue. Ethical journalism is crucial for maintaining public trust and ensuring that the media serves as a reliable source of information for society.

Practice Questions

Question 1

Which of the following best describes the principle of confidentiality in professional ethics?

A) Sharing client information with anyone interested

B) Maintaining privacy regarding client information unless consent is given

C) Discussing client cases with colleagues for advice

D) Reporting any information to authorities without exception

Correct Answer: B) Maintaining privacy regarding client information unless consent is given.

Explanation: Confidentiality is a fundamental principle in many professions, particularly in healthcare, law, and counseling. It involves keeping client information private and not disclosing it to unauthorized parties without the client's consent. This principle helps build trust between professionals and their clients, ensuring that sensitive information is protected. Options A and D violate confidentiality, while C could be acceptable under specific circumstances but does not capture the essence of confidentiality.

Question 2

In the context of professional ethics, what does the term "conflict of interest" refer to?

A) A situation where personal interests may interfere with professional duties

B) A disagreement between professionals on ethical matters

C) A scenario where a professional is penalized for unethical behavior

D) A legal obligation to disclose financial interests

Correct Answer: A) A situation where personal interests may interfere with professional duties.

Explanation: A conflict of interest occurs when an individual's personal interests, such as financial gain or relationships, could potentially compromise their professional judgment or actions. This situation can lead to biased decision-making and unethical behavior, making it essential for professionals to disclose such conflicts and act in the best interest of their clients or employers. Options B, C, and D do not accurately describe the concept of a conflict of interest.

Question 3

Why is it important for professionals to adhere to ethical guidelines in their field?

A) To avoid legal repercussions only

B) To enhance their professional reputation and trustworthiness

C) To satisfy regulatory requirements without concern for ethical principles

D) To ensure compliance with industry trends

Correct Answer: B) To enhance their professional reputation and trustworthiness.

Explanation: Adhering to ethical guidelines is crucial for professionals to build and maintain trust with clients, colleagues, and the public. Ethical conduct fosters a positive reputation and credibility within the profession, leading to long-term success and relationships. While avoiding legal repercussions is important, ethical guidelines are about more than just compliance; they reflect a commitment to integrity and responsibility. Options C and D underestimate the significance of ethics as fundamental to professional identity and practice.