Noise Traders and the Law of One Price

Preparing for the CMT Exam involves grasping the concept of noise traders and the Law of One Price, essential in understanding market anomalies and pricing efficiency. Recognizing how irrational traders, or “noise traders,” impact asset prices and deviate from fundamental values is critical for analyzing price discrepancies and market behavior.

Learning Objective

In studying “Noise Traders and the Law of One Price” for the CMT Exam, you should understand the role of noise traders and how their irrational actions affect market prices and liquidity. Analyze the Law of One Price, which asserts that identical assets should trade at the same price in efficient markets, and evaluate how noise trading can create temporary mispricings and price discrepancies. Explore how these deviations impact arbitrage opportunities and market stability, and examine the limitations that prevent arbitrage from fully correcting prices. Apply your understanding to assess price inefficiencies and evaluate market behavior in CMT practice scenarios.

Understanding Noise Traders

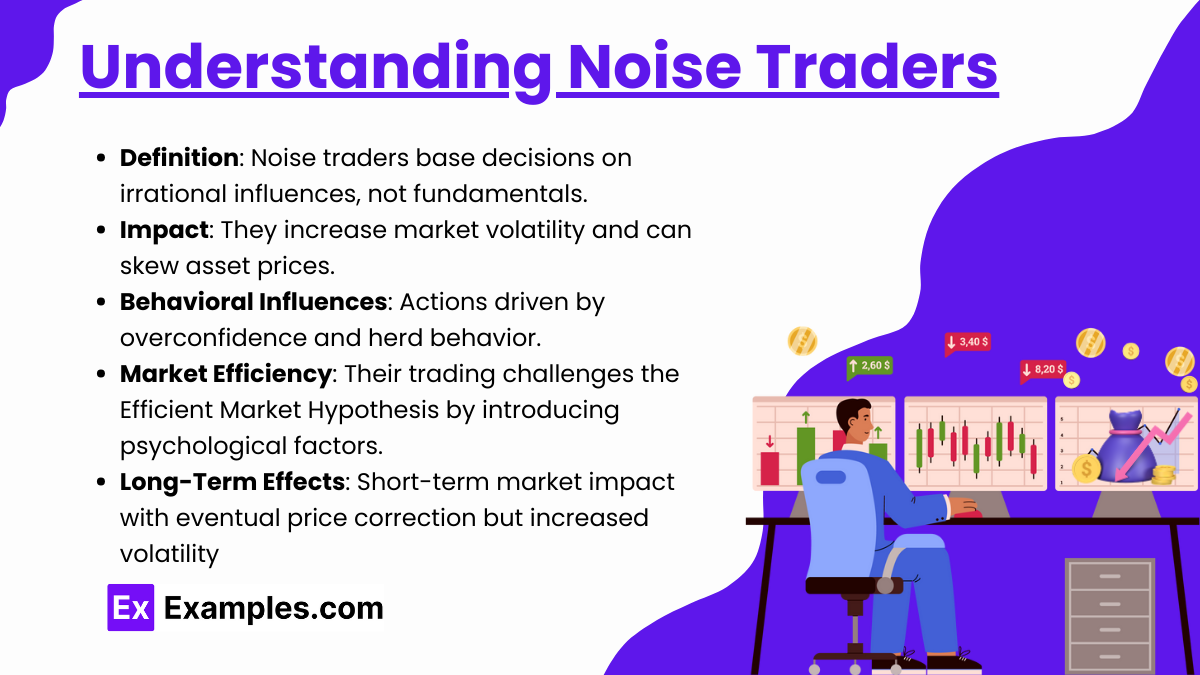

Definition and Characteristics Noise traders are individuals or entities in the financial markets who make buy and sell decisions not based on fundamental value assessments of securities but rather on irrational influences or speculative impulses. These traders often react to news, rumors, or psychological biases, which can lead to erratic market movements. Unlike traditional investors who analyze financial statements and market trends to make informed decisions, noise traders base their actions on less rational, often emotional factors.

Impact on Market Dynamics Noise traders add a significant level of unpredictability and volatility to the markets. They can influence stock prices away from their intrinsic values temporarily, creating opportunities and risks for other traders. For instance, a surge in buying activity from noise traders can inflate a stock’s price well above its fundamental value, leading to bubbles. Conversely, panic selling can unduly depress prices, leading to sharp market downturns.

Behavioral Influences The actions of noise traders are often driven by behavioral finance principles, such as overconfidence, herd behavior, and loss aversion. For example, noise traders might follow a trending stock without understanding its fundamentals due to the herd instinct, leading to increased demand and a subsequent rise in its price. Alternatively, during market downturns, fear and loss aversion can prompt noise traders to sell off holdings irrationally, exacerbating market declines.

Implications for Market Efficiency According to the Efficient Market Hypothesis (EMH), prices in an efficient market reflect all available information. However, noise traders challenge this notion as their trades are not information-driven. Their presence suggests that markets can deviate from efficiency, allowing prices to be influenced by psychological and speculative factors rather than solely by information. This deviation from EMH suggests that other market participants can potentially exploit the inefficiencies caused by noise trading for arbitrage opportunities.

Long-Term Effects While noise traders can significantly impact market prices in the short term, their influence is generally considered to diminish over the long term as prices eventually revert to reflect fundamental values. However, the presence of noise traders can lead to increased trading volume, which might enhance liquidity in the market but also contribute to price volatility, complicating the investment strategies of fundamental and technical analysts alike.

The Law of One Price (LOOP)

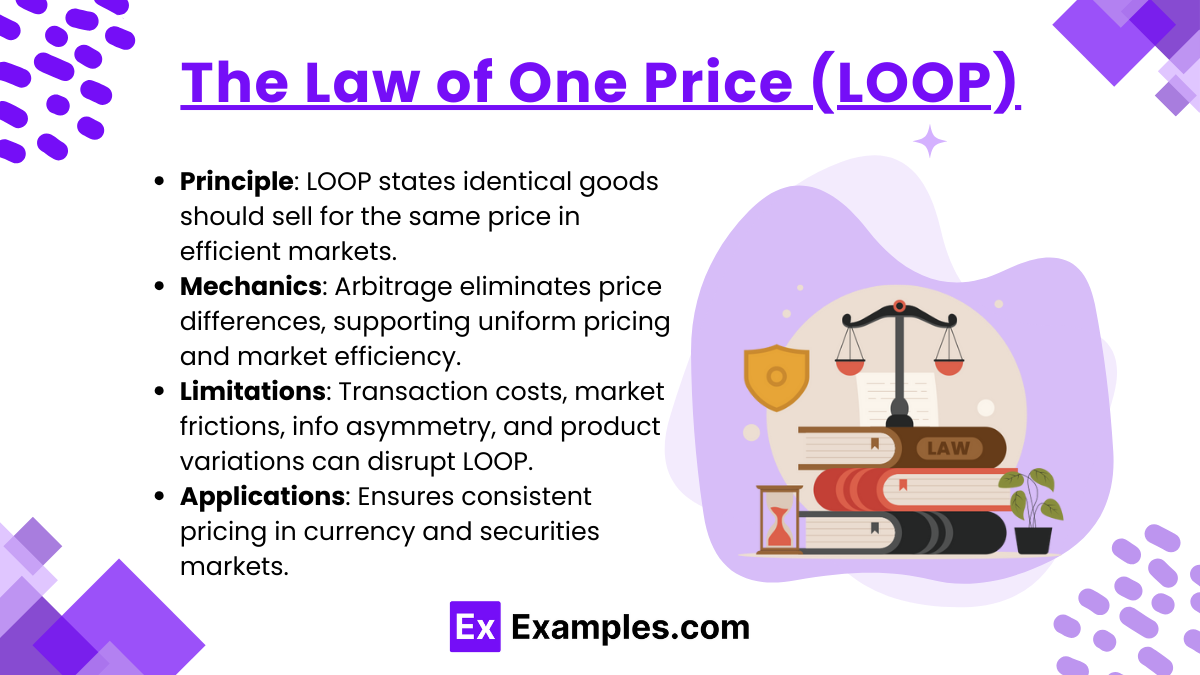

Basic Principle The Law of One Price (LOOP) is a fundamental concept in economics and finance that states that identical goods or financial instruments should sell for the same price in different markets when there are no transportation costs and no differential taxes between the two markets. In essence, LOOP asserts that if markets are efficient, arbitrage opportunities will ensure that the prices of identical assets will equalize across different markets.

Mechanics and Implications LOOP operates on the premise that if two identical items are selling at different prices in different markets, traders will buy the item in the cheaper market and sell it in the more expensive one, thus profiting from the price difference. This process, known as arbitrage, continues until the price discrepancy is eliminated and the items sell for a uniform price across all markets.

This principle is crucial for maintaining consistency in pricing and forms the basis for many financial strategies and economic theories. It also supports the notion of market efficiency, suggesting that markets are capable of self-correcting any pricing anomalies through the actions of profit-seeking individuals.

Challenges and Limitations While the Law of One Price provides a straightforward theoretical framework, several practical barriers can prevent it from holding true in real-world markets:

- Transaction Costs: Costs associated with buying and selling goods, such as fees, taxes, or transport expenses, can inhibit arbitrage, allowing price discrepancies to persist.

- Market Frictions: Various market frictions, including legal restrictions, tariffs, and quotas, can also prevent arbitrage from equalizing prices.

- Information Asymmetry: Differences in access to information can lead to situations where all traders do not perceive products as identical or are not aware of the price differences across markets.

- Non-Identical Goods: In practice, goods and financial instruments may not be perfectly identical across markets due to differences in quality, service levels, or brand perception, complicating the application of LOOP.

Applications in Financial Markets In financial markets, LOOP is closely linked with the concept of purchasing power parity in currency exchange. It suggests that exchange rates should adjust so that identical products cost the same in different countries when prices are expressed in the same currency. Similarly, in the securities market, LOOP is applied to ensure that the same security does not trade at different prices at the same time in different exchanges.

Arbitrage and Market Inefficiencies

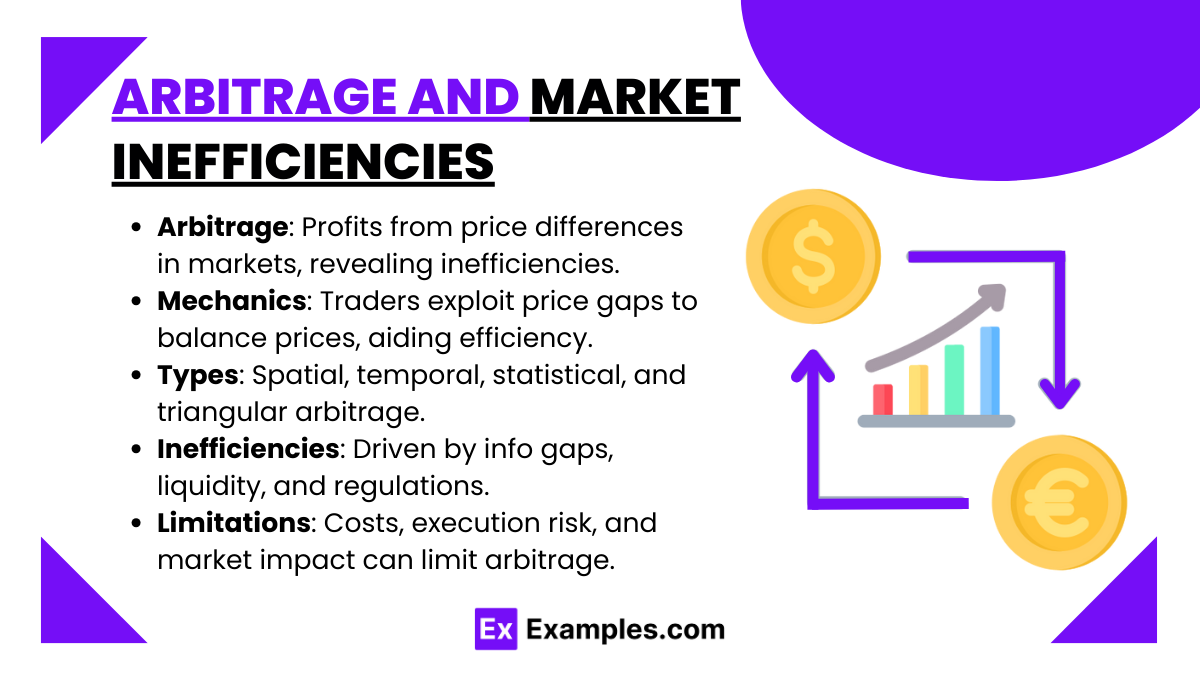

Definition and Overview Arbitrage refers to the simultaneous purchase and sale of an asset in different markets to profit from a difference in the price. It is a financial strategy that exploits price discrepancies between markets or similar assets without taking significant risk. The existence of arbitrage opportunities is often indicative of market inefficiencies, where the prices of identical or similar financial instruments vary across different markets or platforms.

Mechanics of Arbitrage Arbitrageurs, the traders who engage in arbitrage, play a crucial role in the financial markets by helping to ensure that prices do not diverge significantly from their fair value for long. They do this by:

- Identifying Price Discrepancies: Using sophisticated technology and algorithms to monitor and compare prices across various markets in real-time.

- Executing Simultaneous Trades: Quickly buying the undervalued asset in one market while selling the overvalued asset in another, locking in risk-free profits before the prices converge.

Types of Arbitrage

- Spatial Arbitrage: Exploiting price differences between geographic locations.

- Temporal Arbitrage: Taking advantage of price differences occurring at different times.

- Statistical Arbitrage: Using mathematical models to identify price inefficiencies over a longer time frame.

- Triangular Arbitrage: Involving three currencies in the foreign exchange market, where mispricings between currency pairs are exploited.

Market Inefficiencies Market inefficiencies occur when information is not reflected accurately in asset prices, often due to:

- Information Asymmetry: When all participants do not have access to the same information.

- Liquidity Issues: Thinly traded markets may show larger spreads and more pronounced inefficiencies.

- Regulatory and Structural Barriers: Such as capital controls or trading restrictions that can prevent free movement of capital across borders.

Limitations and Barriers to Arbitrage While theoretically sound, arbitrage is limited in practice due to several factors:

- Transaction Costs: High fees, taxes, or other costs can eat into the profits from arbitrage.

- Market Impact: Large orders necessary for arbitrage can themselves shift market prices, eroding potential profits.

- Execution Risk: Delays in trade execution can lead to missed opportunities as markets adjust prices in the interim.

- Counterparty Risk: The risk that the other party in a transaction will not fulfill their obligation.

Implications for Market Behavior Arbitrage contributes significantly to the liquidity and efficiency of financial markets. By quickly acting on price disparities, arbitrageurs help align prices with their theoretical values, correcting anomalies and ensuring that markets function smoothly. Their activities are vital for the integration of global financial markets, helping maintain price parity across different trading venues and reducing the cost of capital.

Examples

Example 1

In the stock market, a celebrity tweets positively about a company they enjoy, leading to a surge in that company’s stock price due to noise traders buying shares based on the tweet rather than the company’s economic fundamentals. This sudden demand drives the stock price above its intrinsic value, temporarily violating the Law of One Price as similar companies in the sector do not experience such increases.

Example 2

A rumor spreads about a potential merger involving a small tech firm, causing noise traders to rapidly buy shares, inflating the stock price. Despite no confirmation of the merger, the price disparity between this stock and comparable stocks in the industry illustrates a breach of the Law of One Price, fueled by speculative trading rather than genuine valuation.

Example 3

During a market downturn, noise traders panic and sell shares of a blue-chip company en masse, driving its price significantly below its fair market value based on its financials. This price is inconsistent with similar companies that have not been sold off as aggressively, showing how noise traders can disrupt the equilibrium predicted by the Law of One Price.

Example 4

Currency markets often see noise traders engaging in trades based on political news or economic forecasts that may not be accurate. For instance, traders might sell off a currency due to a predicted political upheaval, leading to a deviation in its value compared to other currencies with similar economic indicators, thus distorting the Law of One Price in the forex market.

Example 5

In the commodities market, news of a potential shortage of a metal might lead noise traders to buy up futures contracts for that metal, driving prices up based on speculation rather than actual supply constraints. This speculative price does not reflect the metal’s price in physically different markets or its substitutes, thereby distorting the Law of One Price until the actual supply situation becomes clear

Practice Questions

Question 1

What is the primary impact of noise traders on financial markets?

A) They decrease market liquidity.

B) They improve market efficiency by increasing the volume of trades.

C) They contribute to market volatility by trading based on non-fundamental information.

D) They eliminate arbitrage opportunities entirely.

Answer: C) They contribute to market volatility by trading based on non-fundamental information.

Explanation:

Noise traders often make decisions based on speculative, non-fundamental information such as rumors or news headlines, which can lead to irrational trading behaviors. These behaviors contribute to market volatility by creating price movements that do not align with underlying economic or financial conditions.

Question 2

How does the Law of One Price (LOOP) relate to market arbitrage?

A) LOOP states that arbitrage is not possible in efficient markets.

B) LOOP encourages arbitrage by highlighting price discrepancies.

C) LOOP eliminates the need for arbitrage by ensuring identical asset prices.

D) LOOP predicts that arbitrage increases market inefficiencies.

Answer: B) LOOP encourages arbitrage by highlighting price discrepancies.

Explanation:

The Law of One Price asserts that identical assets should sell for the same price in different markets. When this does not hold, it creates arbitrage opportunities where traders can profit from the price differences, thus encouraging arbitrage practices to bring prices into alignment across markets.

Question 3

Which scenario best illustrates a violation of the Law of One Price due to noise trading?

A) A stock is traded at the same price on all exchanges.

B) A stock’s price increases sharply due to a fabricated news article, while its fundamentals remain unchanged.

C) Currency values fluctuate slightly due to differing market opening times.

D) Bonds from the same issuer have identical yields in different countries.

Answer: B) A stock’s price increases sharply due to a fabricated news article, while its fundamentals remain unchanged.

Explanation:

This scenario describes a situation where noise trading based on false or misleading information leads to a significant price increase in a stock, independent of its economic fundamentals. This creates a temporary mispricing and violates the Law of One Price, as the stock becomes overvalued compared to other similar assets whose prices are still aligned with their fundamental values.